![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

19 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

Long-run Costs |

Period long enough for all inputs to become variable. |

|

|

|

Calculation for Total Cost (TC) |

TC = TVC |

Long-run |

|

|

Decisions Business Must Make |

• What must the scale of production be: decide how many units to produce to minimise cist of production.

• Where should the business be located: Factors that influence: nature of product; infrastructure required; target market. • Which production technique should be used: Direct impact of long-run cost of production. Eventually influence profitability. |

|

|

|

Economies of scale |

When inputs are increased and production increase by more than the % increase in inputs. |

|

|

|

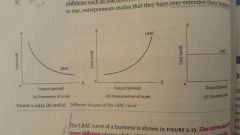

Long-run Average Cost (LRAC) |

• Vary based on economies of scale that a business experiences.• Economies of Scale: LRAC decreases as Q increases• Constant Costs: LRAC remains constant as Q increases• Diseconomies of Scale: LRAC increases as Q increases |

|

|

|

Law of Diminishing Marginal Utility |

As Q consumed increases, satisfaction attained decreases. |

|

|

|

Reasons for Economies of Scale |

• Specialisation of resources. • Technology advanced equipment. • Improvement in organisation eg. assembly-line production. |

|

|

|

Total Revenue (TR) |

Total value of sales of business or producer. |

|

|

|

Calculation for TR |

TR = Price × Q sold |

|

|

|

Average Revenue (AR) |

If AR = Market price, then the product is homogeneous. |

|

|

|

Calculation for AR |

AR = TR/Q sold |

|

|

|

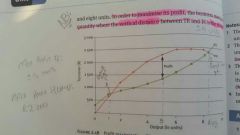

Marginal Revenue (MR) |

Change in TR if one additional unit of a product is sold. |

|

|

|

Calculation for MR |

MR = (Change in TR)/(Change on Q sold) |

|

|

|

Accounting Profit (or total profit) |

The difference between TR from sales and total explicit costs. |

|

|

|

Explicit Costs |

Payments of money that have been made for the factors of production and other inputs that are used in the production process. |

|

|

|

Normal Profit |

• Minimum return that is required by the owners of a business in order for them to continue with the business. • This profit should be large enough to justify the continuation of the business. • Normal profit is the remuneration for entrepreneurship. • It included in the TC of production. |

|

|

|

Economic Profit |

Extra profit (additional to the money that is allocated to the entrepreneurship as a factor of production) that a business makes on a specific transaction. |

|

|

|

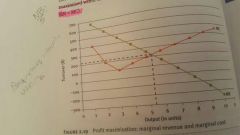

Draw MR/MC Graph |

|

|

|

|

Draw MR/MC Graph |

|

|