![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

74 Cards in this Set

- Front

- Back

|

The law of demand |

When Price falls, consumers will buy more of a good; when price rises consumers will buy less |

|

|

Economic Agents |

The main agents (participants in the economy are individuals such as consumers or workers, the firm's who produce and the government. All these agents have decisions to make regarding the allocation of resources. |

|

|

Scarcity/ fundamental economic problem |

We have unlimited human wants and needs but finite resources Therefore we have to make choices |

|

|

Positive statement |

A statement of fact that can be scientifically tested to see if it is correct or incorrect |

|

|

Normative statement |

A statement that includes a value judgement and cannot be refuted by just looking at the evidence

Often contain "ought, should, better, worst" |

|

|

A value judgement |

Based on an individuals opinion |

|

|

Need |

Something that is necessary for human survival, such as food, clothing, warmth, shelter |

|

|

Want |

Something that is desirable, such as fashionable clothing, but not necessary for survival |

|

|

Economic Welfare |

The economic well-being of an individual or a group within society or an economy. |

|

|

Production |

A process or set of processes that converts inputs into outputs of goods Converts input to output |

|

|

Capital goods |

A good which is used in production of other goods and services. Also known as a Producer Good. |

|

|

Consumer good |

A good which is consumed by individuals or households to satisfy their needs or wants |

|

|

Renewable resources |

A resource such as timber that with careful management can be renewed as it is used |

|

|

Land |

The natural resources on the planet, some natural resources are renewable and others are non renewable. The environment is a scarce resource: soil, water, forest, fisheries, minerals, gases like hydrogen and oxygen |

|

|

Finite resources |

A resource such as oil, which is scarce and runs out as it is used. Also known as non-renewable resource |

|

|

Labour |

Work completed by the individuals/ workers |

|

|

Capital |

Tools or equipment used by labour to produce goods and services |

|

|

Enterprise |

The individual or group of individuals prepared to take a risk and combine these factors of production |

|

|

Fundamental Economic problem |

How best to make decisions about the allocation of scarce resources among competing uses so as to improve and maximise human happiness and welfare |

|

|

Scarcity |

Results from the fact that people have unlimited want a bug resources to meet these want are limited. In essence pale would like to consume more goods and services than the economy is able to produce with its limited resources |

|

|

Economic activity |

The production of goods and services to satisfy people's needs and wants |

|

|

Economic activity |

The production of goods and services to satisfy people's needs and wants |

|

|

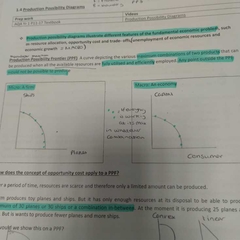

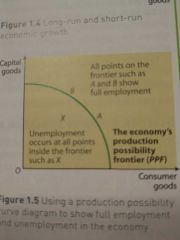

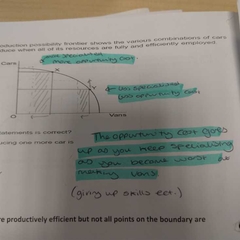

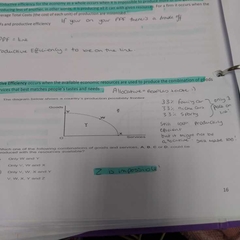

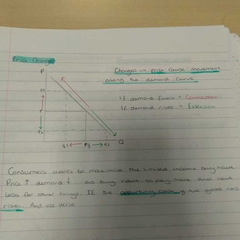

PPF ( Production Possibility Frontier) |

A curve depicting the various combinations of two products that can be produced when all the available resources are efficiently employed. Resources fully utilised (land, capital, labour) PPF = Line Productive Efficiency = to be on the line |

|

|

Opportunity cost |

The cost of giving up the next best alternative |

|

|

Traditional economist |

Expects consumers to act rationally in only a self interested way to maximise income and private benefit |

|

|

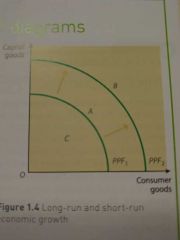

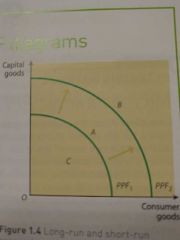

Economic Growth |

The increased in the potential level of real output the economy can produce over a period of time. |

|

|

Short run vs long run economic growth |

Short term= C to A Long term= A to B |

|

|

Full employment vs unemployment |

Full = When all who are able and willing to work are employed Un = opposite ^ |

|

|

Trade off |

Giving something up to get more of something |

|

|

Production Possibility curve |

|

|

|

PPF and opportunity cost / specialisation |

This happens because your mote specialised as you move across and so opportunity cost increases as you move across as you assume they get better at making or doing whatever.

The opportunity cost goes up as you keep specialising as you become worst at making or doing whatever, giving up skills |

|

|

Allocative Efficiency |

Occurs when the available resources are used to produce the combination of goods and services best maybe a people's tastes and needs Z is impossible |

|

|

Productive Efficiency |

For the economy as a whole occurs when it is impossible to produce more of one good without producing less of another good. For a firm it occurs when the average got cost of production is minimised Being on the PPF line

Maximising output and minimising waste |

|

|

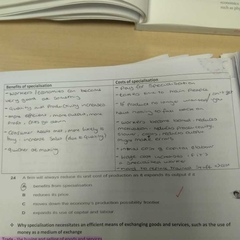

Specialisation |

A worker only performing one task or a narrow range of tasks. Also different firms specialising in producing different goods and services Individual- 1 degree Firm - 1 type of product car Economy - Uk financial services, education etc |

|

|

Division of labour |

Different workers perform different tasks in the course of producing a good or service |

|

|

Productivity |

Output per hour per displeasure how well you use your factors of production |

|

|

Labour productivity |

Output per worker |

|

|

Capital productivity |

Output per unit of capital |

|

|

Production |

Is a measure of the value of the out out of goods and services An increase in production means there's been an increase in productivity |

|

|

Benefits and costs of specialisation |

It also becomes cost effective to provide workers with specialist equipment |

|

|

Trade |

The buying and selling of goods and services |

|

|

Exchange |

To give something in return for something else received, money is a medium of exchange Specialisation needs a medium of exchange |

|

|

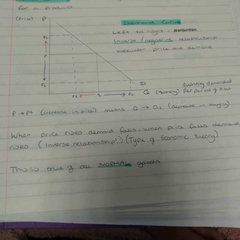

Price mechanism |

Refers to system where the force of demand and supply determine the price of commodities and changes therein. The buyers and sellers determine (market mechanism) |

|

|

Planning/command mechanism |

Refers to where the government rather than the free market determine what goods ago produce how many how much. Communist ideas |

|

|

Pure market economy |

Relies exclusively on markets to allocate resources and to answer all three questions of allocation. Theoretically no government involved No real economy is completely |

|

|

Complete command economy |

All decisions what how how much when where and whom for are taken by central planning authority. Only a very rigid totalitarian political frame. No real economy is completely |

|

|

UK economy |

Is a mixed economy Has large non market and market sector But the non market sector is much smaller than 40 years ago due to privatisation, marketisation and deregulation Economic liberalisation |

|

|

Competitive market |

A market in which the large number of buyers and sellers possess good market information and can easily enter or leave the market |

|

|

Market |

Buyers and sellers willing to meet |

|

|

Equilibrium price |

The price at which demand for a good or service exactly equals planned supply |

|

|

Supply |

The quantity of a good or service that firms are willing and able to sell at given prices in a given period of time |

|

|

Demand |

The quantity of a good or service that consumers are willing and able to buy at a given time. For Economists demand is always effective demand |

|

|

Effective demand |

The desire for a good or service backed by the ability to pay |

|

|

Intended demand |

Planned desired but not able/ actual/ realised back by the ability to pay |

|

|

Individual demand |

Eve ty individual has their own demand curve for every product which can be difficult |

|

|

Market demand |

The quantity of a good or service that all the consumers in a market are willing and able to buy at different market prices (Total of all the individual demand curves for a product) |

|

|

Demand curve |

A demand curve shows the relationship between programs demand, this inverse or negative relationship headaches under ceteris parabus the consumer is inclined to buy less of the price goes up as they want to maximise return on their income |

|

|

Ceteris Paribus |

"All other things remain equal"

This means we are only considering price sensibility and not looking at anything else. Climate, travel, terrorism, security, exchange rate, advertisement |

|

|

Normal goods |

A good for who h demand increases as income rises and demand decreases as income falls |

|

|

Inferior good |

A good which demand decreases as income rises and demand increases as income falls |

|

|

Speculative demand |

People believe price will rise in the future, petrol, shares |

|

|

Price = Quantity |

Believing higher price means higher quality New care, private education |

|

|

Veblen goods |

Snob value, exclusive appeal, RRolex Ferrari |

|

|

Price changes |

|

|

|

Determinants/ conditions of demand Factors causing shifts |

-Change in price of substitutes, competing, joint demand, complementary products -personal income -tastes and preferences -population size

-advertisement and publicity -seasonal products -change in law |

|

|

Law of supply |

Higher prices imply higher profits and that this will provide the incentive to expand production Opportunity cost of not supplying the product is higher than supplying it which means not to supply is less attractive |

|

|

Individual supply |

Every firm apartheid own supply curve for every product |

|

|

Market supply |

The total of all individual supply curves from all forms for a product |

|

|

Firm / producer and consumers |

Main objective us to maximise profit, supply curve must consider costs as these drive the price charged

Consumers want to maximise return on their income |

|

|

Profit = |

= Total revenue - Total costs

Revenue: sale only Profit: surplus |

|

|

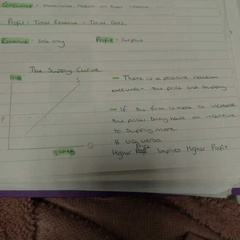

Supply curve |

A supply curve shows the relationship between price and quantity of supply, this is a positive relationship - as price goes up supply goes up and vice versa, this is because if the price of the product goes up then firms have more of an incentive to make more / new firms join the market, because they can make more profit, increased opportunity costs |

|

|

Conditions of supply |

-costs of production ^wage cost ^raw materials ^energy cost ^costs of borrowing ^technical progress ^taxes and subsidies |

|

|

Market Equilibrium |

A market is in equilibrium when planned demand equals planned supply and the demand curve crosses the supply curve. |

|

|

Market disequilibrium |

Exists at any price other bbs. The equilibrium price. When the market is in disequilibrium either excess demand of excess supply exists in the market. Excess demand causes the price to rise until a new equilibrium is established. Excess supply causes the market price to call until equilibrium is achieved |