![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

8 Cards in this Set

- Front

- Back

|

What is a budget ? |

A budget is a formal statement, in financial terms of management's plans for the future. Budgets are prepared for all parts of operations and for all types of assets. The keys to successful budgeting are 1) to make accurate forecasts of the future and 2) to compare actual results with those that were forecasted. |

|

|

What is a master budget? |

The master budget is the comprehensive set of all budgetary schedules and the pro forma (before the formal; an estimate of) financial statements of an organization. It sets then target sales, production, distribution and financing activities. It generally culminates on a cash budget, a budgeted income statement and balance sheet. |

|

|

Sales Budget |

This is the most difficult budget to prepare as it is not easy to estimate consumer's future demands, especially when a new product is being introduced. It is, however, the starting point in preparing the master budget.

It is possibly the most important subsidiary budget because if the sales figure is incorrect, the practically all the other budgets will be affected, especially the master budget.

It is derived from the sales forecast and ot should represent management's best estimate of sales revenue for the year. An inaccurate sales budget may adversely affect net income. Usually, the sales and production manager is responsible for producing this budget. |

|

|

What is the layout for a sales budget? |

Sales {units} x selling price = sales {$} |

|

|

Production Budget |

This budget shows the units that may be produced to meet anticipated sales.

The production budget is based upon the sales budget, production capacity and the budgeted finished goods stock requirement.

|

|

|

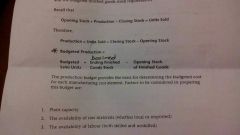

What is the layout for the production budget? |

Budgeted sales (units) Add: closing stock = Total amount required Less: Opening Stock = Required production |

|

|

Direct Material Budget |

This budget contains both the quantity and cost of direct materials to be purchased. It is based upon the production budget and the budgeted material stock. |

|

|

Layout of Direct Materials budget |

Units to be produced x # of pounds/kgs/ tonnes per unit = Direct material required ( unit of measure) Add: Desired closing stock = Total amount required - Opening stock = Total material for production x *cost per unit of measure* = Cost of material

|