![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

51 Cards in this Set

- Front

- Back

|

Incidence: |

the analysis of the effect of a particular tax on the distribution of economic welfare. Tax incidence is said to "fall" upon the group that ultimately bears the burden of, or ultimately has to pay, the tax. |

|

|

Basic Elements of Tax System |

Tax Base Tax Rate Tax Unit |

|

|

Tax Base |

Economic activity on which tax is levied. Simplest form is head/lump sum/poll tax Lump Sum; Income; Expenditure; Wealth. |

|

|

Lump Sum Tax |

Levied on individual, regardless of income and spending. - Inequitable as everyone pays the same regardless of capacity to pay - Non distorting = efficient! Second Welfare Theorum depends on lumpsum - Often used in research/models where tax is not the focus - Thatcher tried to introduce - was thrown out |

|

|

Income Tax |

Conceptually the same as Expenditure tax Y = Y(L) + Y(C) = C+S Y(L): Labour income ... Y(C): Capital Income aka. Direct Taxes; borne by entity that pays it. Progressive but distortionary |

|

|

Consumption Tax |

Indirect tax; may be legally borne by one and paid by another - payroll taxes, commodity tax... C + S (Consumption + Savings) Regressive - less distortionary |

|

|

Wealth Tax |

Tax on stock of assest rather than flow of income spawned from those assets. Tax value of assets held by individual/corporation eg. Land tax |

|

|

General / Partial |

General: Levied Uniformly on all components of a tax base with no exceptions eg. based on total income recieved Partial: Selective Tax levied on only park of tax base. AUSTRALIA: Income Tax makes up 65% total tax revenue - Not general as it allows some exeptions (imputed rent, bequests... savings & retirement incomes taxed at concessional rates) |

|

|

Most Common Consumption Tax |

Expenditure Tax - Tax on total income - Savings -- avoids double taxation! ---Currently: income earned on savings is tax and again when spent! Economists have been pushing for just an Expenditure tax to avoid extra taxation - never implemented due to politics |

|

|

Value Added tax

|

aka GST in AUS (General Consumption Tax) - % tax on value added at each stage of production - Mostly borne by consumer (end of the line!) - Rarely applied generally; most OECD gov except health, education, some food... equaling about 40% of consumption! (= distortion) ----EXCLUDING NZ, VAT is quite general. |

|

|

TAX RATE |

Tax Collected / Tax Base Average Tax Rate ATR = Total Tax paid/Value of Tax Base Marginal Tax Rate MTR = Change in Tax Paid / Change of Tax Base |

|

|

Tax Rate Structure (3) |

Progressive Tax System Proportional Tax System Regressive Tax System |

|

|

Progressive Tax System |

ATR rises as tax base value changes (MTR is changing) eg. Income Tax |

|

|

Proportional Tax System |

ATR is constant as tax base value changes (MTR does nothing) |

|

|

Regressive Tax System |

ATR falls as the base rate changes |

|

|

Tax Unit |

Entity on which tax is levied Individuals or House Holds (irrelevant if MTR is constant - flat rate tax) Choice can have significant effect on tax liability - may have efficiency and equity implications |

|

|

Tax Unit - Individuals |

Most common for AUS and most OECD countries - Treat individuals as income tax unit. -- but they use households as unit for welfare/redistribution! |

|

|

Tax Unit - Household |

Some countries (France, Germany, Switzerland) treat FAMILIES as a unit - raises opportunity for income shifting within the household |

|

|

EXEMPTIONS |

Tax concessions; some are complete exemptions, others partial AUS has: - Superannuation income - Capital gains on owner-occupied housing -----there is tax on investment housing - Bequests/Inheritance ------ no death duties - NFP organisations - no income tax - Certain Goods and Services (health etc...) |

|

|

Tax Hypothecation |

Links expenditure to the source of funds - Common. 25% state rev in USA is from it Funds are used to compensate a group in society that has lost an entitlement or suffered exceptional damanges - Social Security Contributions, Super, Flood Damage Levy, Roads... Bush Fires... Treasure HATES it as it reduces their autonomy |

|

|

Tax Hypothecation ADVANTAGES |

- Politically easier to raise revenue (can see benefit) - Facilitates economic tests of public benefit of taxes |

|

|

Tax Hypothecation DISADVANTAGES |

- If hypothecated revenue < expenditure it effectively just contributes to consolidated revenue - If revenue > expenditure resource allocation may be distorted. |

|

|

What is Tax Avoidance |

Any behaviour that legally reduces tax liability; organising business affairs to avoid taxation ** Salary sacrifice; **Shifting Income to retirement fund at lower rate; **Shifting assets to low tax family member |

|

|

What is Tax Evasion |

Not paying tax that is legally due - Under reporting income; over-reporting expenses - Offshore earnings hidden in havens |

|

|

Evasion VS Avoidance |

Hard to distinguishin Aus: if tax avoidance is the main driver behind an activity it's considered tax evasion and is not allowed- Apple, BHP...

|

|

|

Tax Avoidance facts |

- Distorts economic behaviour - Ties up professional resources - May be inequitable (those that can pay can be better at avoiding) - Means tax rates must be increase - compared to if there was no avoidance |

|

|

Tax Evasion facts

|

- Creates an informal economy (cash) - Distorts economic behavior - Is inconsistent with equity |

|

|

Evaluating Tax Systems: How should tax revenues be raised to meet expenditure requirements and distributional objectives while creating minimum efficiency cost |

Good tax system: 1) Equitable 2) Efficient (minimize DWL) 3) Administratively Simple (4) Politically responsible ) |

|

|

Key Concepts - Equity |

Ability to pay principle

ADAM SMITH: "individuals should contribute according to their respective abilities" ----Ability to pay is difficult to measure, money income used as a proxy but that causes issues----- |

|

|

Key Concepts - Equity: Main principles

|

Horizontal: Individuals in like circumstances should be treated similarly (AUS) Vertical: Individuals with more capacity to pay should pay more |

|

|

Key Concepts - Equity: Other principles |

Benefit Principle: Individuals should pay for the benefits they recieve - can't work due to public goods etc etc. These are hypothecated taxes. Intergenerational Equity: Fairness between generations Principle of "Fair Desserts": Individuals deserve to keep what they work for/earn |

|

|

Key Concepts - Efficiency |

All taxes (excluding lump sum) distort prices. Price distortions = price wedges ---- occur between: - Wages received & Marginal product (labour tax) - the Gross & Net Return of Capital (capital tax) - Product Prices & Marginal Costs (commodity tax) |

|

|

Key Concepts - Efficiency: Other issues |

- Administration & Compliance costs ----- ~1% of revenue collected in Aus (0.3% GDP) ----- Cost of designing, operating & changing system - Compliance costs: Cost of dealing w/tax system ----- agents/advisors estimated 2-4% GDP - Political Responsibility: Transparency and Certainty |

|

|

Statutory Incidence |

Determines who is responsible for paying tax Legalities, less important - focus on economics |

|

|

Economic Incidence |

Change in any real income of any economic agent as a result of taxation. Reliant on D&S elasticity |

|

|

Economic Incidence details |

- Analysis of incidence helps explain how taxes change price of commodities and factors of production which affects distributional income - Shifting of tax burden occurs mainly with indirect taxes - Distribution of tax burden is independent of statutory incidence (who pays) |

|

|

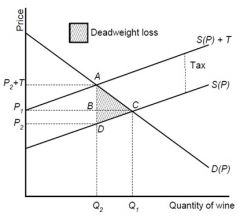

Commodity Taxes |

Unit Tax: Given dollar amount for each unit perchased - shifts marginal cost up Ad Valorem Tax: a percentage tax rate on value/quantity of commodity/service |

|

|

Commodity Tax - on producers |

|

|

|

Commodity Tax - on Consumers |

|

|

|

Economic Incidence |

Depends on elasticity of demand & supply - If Demand = Perfectly inelastic // Supply = elastic ------ Consumers pay tax - If Demand = elastic // Supply = perfectly inelastic ------ Producers pay tax - For cases in between, tax is shared Agent with the most elastic response bears the least amount of the burden. |

|

|

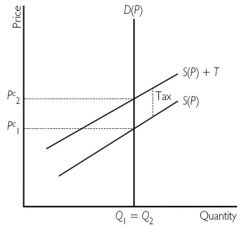

Incidence with perfectly inelastic demand |

consumers bear burden |

|

|

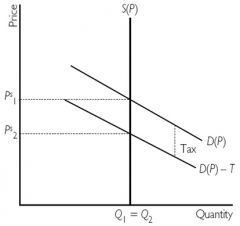

Incidence with perfectly inelastic supply |

producers bear burden |

|

|

Ad Valorem Tax |

Levied as a proportion of the price of the good - if tax revenue raised is the same as with unit tax the real incidence is the same -- Ad valorum taxes are more fair and becoming more popular |

|

|

Imperfect Competition |

incidences depends on many factors. Monopolists (or a firm with market power) can pass on tax burden to consumers |

|

|

Imperfect competition - how market power can shift burden |

- Price discrimination - Marginal Revenue curve is non-linear - Supply curve is elastic (same with perf comp) - Tax is ad valorum (rather than unit tax) |

|

|

Factors of Production |

Most factor taxes (land, labour (payroll), capital) are ad valorum. Incidence depends on: - Market D&S elasticities - Nature of the market (im/perf comp) - less elastic side of market bears tax |

|

|

Factors of Production - Tax on Labour

|

1) Personal Income Tax (PayAsYouEarn) - incidence on YOU 2) Payroll taxes - incidence on employer |

|

|

Factors of Production - Tax on Labour - Payroll Tax who bears |

Relatively inelastic labour Supply curve = labourer bears most of the tax Elastic labour supply at Union determined wage = employer bears tax |

|

|

Factors of Production - Capital Income |

Closed Economy: if inelastic supply, burden borne by domestic capital owners Open Economy: if perfectly elastic, domestic capital owners still bear cost -> lower foreign capital supply Open or Closed economy changes supply of foreign capital, not the burden. |

|

|

Factors of Production - Land |

Total supply of land is perfectly inelastic - General land tax borne by land owner; reduces market price of the land -- hard to pass burden on. Many land taxes are selective. |

|

|

General Equilibrium Analysis - CGE modelling |

examining the big picture, all effects (flow on affects of taxation) |