![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

32 Cards in this Set

- Front

- Back

|

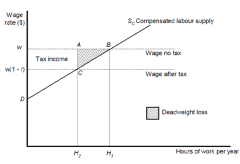

DWL - labour income - burden on worker |

Supply curve that shows how quantity of labour supplied varies with wage rate - Utility = constant Gross wage doesn't change, Net wage changes |

|

|

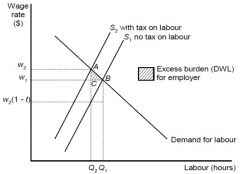

DWL - labour income - burden on employer (payroll tax) |

|

|

|

Compensated Labour Supply - details |

- nets out income effects

- only shows substitution effect of a change in wage rate (between work-leisure trade-off) - wage rate is assumed to be a given (equal to Marginal Product) - demand is steady |

|

|

Pareto Efficiency |

When it is impossible to make one individual better off without worsening the situation for another |

|

|

Optimal Income Taxes |

What is the least distortionary method of gaining a given revenue?

Equal Absolute Sacrifice Equal Proportional Sacrifice Equal Marginal Sacrifice |

|

|

Optimal Income Taxes - Equal Absolute Sacrifice |

Each person should sacrifice the same utility (not income) - Not sensible |

|

|

Optimal Income Taxes -Equal Proportional Sacrifice |

Each person should sacrifice an equal proportion of their utility (%) - Not sensible |

|

|

Optimal Income Taxes -Equal Marginal Sacrifice |

if A has less marginal utility of income than B (cares about money less) A should be taxed more until the utility is level/equated. Marginal Income Utility: change in utility for +$1 in income |

|

|

Optimal Income Taxes -Optimal Design |

is complicated - broad aim is to choose tax rates and levels of spending subject to labour supply constraints and feasibility that maximises social welfare |

|

|

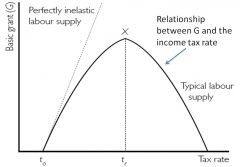

Optimal Income Taxes - Optimal Design graph |

Optimal Tax or labour income is actually along the left side somewhere |

|

|

Optimal Income Taxes -Linear Tax Structure |

a tax with constant marginal tax rate: CAN BE: - Proportional - Progressive |

|

|

Optimal Income Taxes -Linear Tax Structure: Proportional |

Tax paid is proportional to income (MTR=ATR at all levels of income) |

|

|

Optimal Income Taxes -Linear Tax Structure: |

MTR is constant but ATR increases with income - achieved by awarding a given grant (G) to all, along with a proportional tax rate |

|

|

Optimal Income Taxes - Non-Linear Tax System |

Marginal Tax Rate varies with income (typically MTR>ATR) Australia and most other countries |

|

|

Optimal Income Taxes -KEY ISSUES |

Economic Efficiency: function of MTR Economic Equity: function of ATR Optimal Tax system attempts to have low MTR to minimize efficiency costs while increasing ATR for equity - Non-Linear System is prefered ---- NLS has high admin/compliance costs (are they worth the cost?) |

|

|

Optimal Commodity Taxes |

DWL ^ with elasticity of D&S Aim is to minimize DWL from taxes on goods needed to meet revenue target MUST DETERMINE: - Quantity changes that result in lowest DLW - Tax rates that produce these Q changes |

|

|

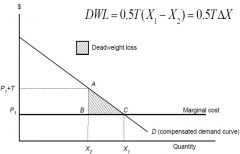

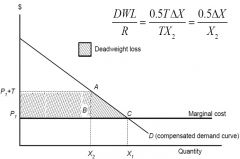

Optimal Commodity Taxes - DWL from Unit Tax on Good X |

|

|

|

Optimal Commodity Taxes - ratio of DWL to revenue raised |

|

|

|

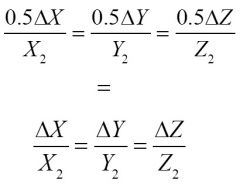

Optimal Commodity Taxes - Analysis for 3 goods |

Equate marginal DWL as required for commodity tax to be efficient. - suggests that % reduction should be the same for all, only works for small changes in consumption (when X is close to Y) |

|

|

Optimal Commodity Taxes - Ramsey Rule |

Inverse Elasticity Rule: determines tax rates consistent with equal proportionate rule (which has general application ) - Tax rate lessens as elasticity rises ---Goods with lower elasticities should be taxed higher Theory was developed to show how to raise given revenue from a limited set of commodity taxes --- in practice this has limited application (we tax goods broadly using one rate for simplicity) |

|

|

Optimal Commodity Taxes - Uniform Commodity Tax arguments |

- Under certain conditions, it's efficient - Relatively low distortion - Simple therefore low compliance costs *Economists recommend uniform tax except when dealing with G&S that provide positive externalities (education...) |

|

|

Taxes on Intermediate Goods and Trade |

Governments often tax producer goods and internationally traded goods (intermediate goods tax is bad in AUS) - Diamond and Mirrlees (1971) Gov's can't improve welfare by taxing intermediate goods - incredibly distortionary *Economists prefer taxes on income & consumption |

|

|

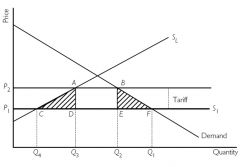

Taxes on Intermediate Goods and Trade - DWL of tariff |

Loss of tax on imports

|

|

|

Optimal Tax System - options |

Head Taxes - equitable but not feasible Income Taxes Consumption Taxes Wealth Tax - used on land/natural resources but taxes on income works too... |

|

|

Optimal Tax System - General Income Tax |

would tax all sources of income at the same rate - could be non/linear (most are hybrid) |

|

|

Optimal Tax System - General Commodity Tax |

Expenditure Tax --- never implemented (politics) VAT/GST --- high compliance costs General Retail Sales Tax --- Difficult to differentiate customer and producer (USA has this at state level 6% VA) |

|

|

Optimal Tax System - KEY PRINCIPLES |

1) All taxes should be viewed as part of the same system - direct income taxs can be used to meet distributional goals, others should focus on efficiency 2) Tax should be comprehensive and neutral - Broad base rate reduces rates&distortions, Similar things should be taxed similarly 3) Tax rates should be higher for factors or goods in inelastic Supply/Demand 4) Fixed resources (land) can be taxed efficiently (high) allowing labour to be taxed lightly [avoid work-leisure tradeoff] 5) Producer goods should not be taxed 6) Taxes should be targeted at externalities 7) Tax should be as simple as possible to avoid distortions - have fewest departures from general uniform tax |

|

|

Mirrlees Review (2011) UK Principles |

1) Should be progressive and neutral 2) Income tax should be clear, progressive rate schedule with single grant to low income people (no more than 3 increasing MTR) 3) Income from all sources of labour and capital should be taxed using same rate schedule to maintain relative prices between the two 4) All costs of generating income should be deductible 5) Commodity taxes have a role - captures income that avoids tax, affects labour surplus less 6) Uniform Commodity tax should be charged on final consumption with broad base and low rates 7) Pure economic rents should be taxes (land/natural resources) - hard though |

|

|

TAX REFORM Challenges |

- Choice between imperfect systems. Second Best Theorum: Fixing one distortion will affect another - always produces a winner/loser. Should generate net aggregate gain to compensate losers - doesn't - Multilevel gov systems can make tax reform more complex |

|

|

TAX REFORM - should be evaluated on system basis |

- preferably based on social welfare function - most tax systems evolved haphazardly and are ineffficient |

|

|

TAX REFORM proposals are based on |

- Base Broadening - More uniform (lower) tax rates [fewer exemptions] - Reducing discrimination against savings [double taxation] - Tax simplification - Re-writing statues to reduce tax evasion |

|

|

Henry Review |

Australia has too many taxes and they're way too complex --- the tax systems are subject to demands for increasing amounts of things! - the capacity of the legislative/operating platforms to manage the complexity has been reached (they can't handle it) - 90% of Australia's tax revenue is raised from 10 out of the 125 taxes |