![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

54 Cards in this Set

- Front

- Back

|

Market microstructure |

The market structures and processes that affect how the manager's interest in buying or selling an asset is translated into executed trades |

|

|

Principal trade |

A trade with a broker in which the broker commits capital to facilitate the prompt execution of the trader's order |

|

|

Markets should provide |

- liquidity - transparency - assurity of completion |

|

|

Quote-driven markets |

Rely on dealers to establish firm prices at which securities can be bought or sold. |

|

|

Inside bid / market bid |

Highest and best bid |

|

|

Inside ask / market ask |

Lowest ask |

|

|

Inside quote / market quote |

Using the inside bid and inside ask |

|

|

Effective spread (buy order formula) |

= 2 × (execution price - midquote) |

|

|

Electronic crossing network |

Orders are batched together and crossed (matched) at fixed points in time during the day at avg bid and ask quotes |

|

|

Auction markets |

Trader orders compete for execution |

|

|

Automated auctions |

Computerized auction markets Provide price discovery |

|

|

Use Brokered markets when: |

Investors use brokers to locate counterparty to a trade. When: 1. Large block to sell 2. Want to remain anonymous 3. Market for the security is small or illiquid |

|

|

Hybrid market |

Combination of quote-driven, order-driven, and brokered markets |

|

|

Relationship between trader and broker |

Principal and agent Broker acts as trader's agent, locates necessary liquidity and best price. Broker may also provide record keeping, financing, cash management, and other services |

|

|

Relationship between trader and dealer |

Opposing interests Dealers want to maximize trade spreads while traders want to minimize Trader profits at dealer's expense when have extra info (adverse selection risk) |

|

|

Market liquidity |

small bid-ask spread mkt Dept resilience = stay close to intrinsic value |

|

|

Transparent market |

Can without significant expense or delay obtain both pre-trade info and post-trade info. If not = lose faith, decreasing trading activity |

|

|

Market's assurity of completion |

Can be confident that counterparty will uphold their side of trade agreement |

|

|

Explicit costs |

Readily discernible and include commissions, taxes, etc |

|

|

Implicit costs |

Bid-ask spread, market or price impact costs Opportunity costs Delay costs (eg. Shipping) |

|

|

Implementation shortfall |

Difference between actual portfolio return and paper portfolio return. For purchase: - increase in price = cost - decrease in price is account benefit (a negative cost) |

|

|

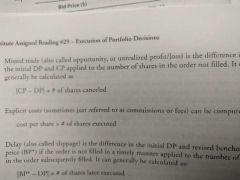

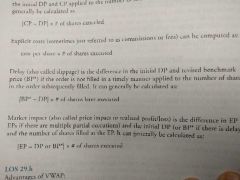

Decision price (DP) |

Mkt price when order is initiated |

|

|

Revised benchmark price (BP*) |

Mkt price of security if order not completed in timely manner as defined by user |

|

|

Missed trade equation |

|

|

|

Explicit costs |

Commission or fees. = Cost per share × # shares executed |

|

|

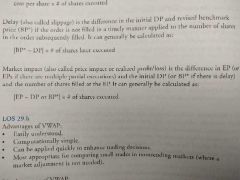

Delay |

|

|

|

Market impact |

|

|

|

Advantages of VWAP |

1. Easily understood 2. Computationally simple 3. Can be applied quickly to enhance trading decisions 4. Most appropriate for comparing small trades in nontrending mkts |

|

|

Disadvantages of VWAP |

1. Not informative for trades that dominate trading volume 2. Can be gamed by traders 3. Doesn't evaluate delayed or unfilled orders 4. Doesn't account for mkt movements or trade volume |

|

|

Advantages of Implementation Shortfall |

1. PM can see the cost of implementing their ideas 2. Demonstrates the trade-off b/w quick execution and mkt impact 3. Decomposes and identifies costs 4. Can be used in an optimizer to minimize trading costs and max performance 5. Not subject to gaming |

|

|

Disadvantages of Implementation Shortfall |

1. May be unfamiliar to traders 2. Requires considerable data and analysis |

|

|

Use of Econometric models |

Used to forecast transaction costs |

|

|

Mkt microstructure theory has shown that trading costs are nonlinearly related to: |

1. Security liquidity: trading volume, mkt cap, spread, price 2. Size of the trade relative to liquidity 3. Trading style: more aggressive = higher costs 4. Momentum : trades that require liquidy 5. Risk |

|

|

Usefulness of econometric models |

1. Trading effectiveness can be assessed by comparing actual trading costs to forecasted trading costs from the model. 2. Can assist PM in determining the size of the trade |

|

|

Information-motivated traders |

Trade based on time-sensitive info. Prefer mkt orders bc trades must take place quickly Trades demand liquidity, willing to beat higher trading costs |

|

|

Value-motivated traders |

Use investment research to uncover misvalued securities. Will use limit orders. Main objective = price, not speed |

|

|

Liquidity-motivated traders |

Transact to convert securities to cash or reallocate portfolio from cash. Utilize mkt orders and trades on crossing networks and electronic communication networks (ECNs) Prefer to execute orders within the day |

|

|

Passive traders |

Trade for index funds and other passive investors Favor limit orders and trade on crossing networks. Allows for low commissions, low mkt impact, price certainty, possible elimination of bid-ask spread. |

|

|

Liquidity-at-any-cost trading focus |

Must transact large block of shares quickly. Must be ready to pay higher price for trading in the form of mkt impact, commissions, or both |

|

|

Costs-are-not-important trading focus |

Believe exchange mkts will operate fairly and efficiently such that execution price they transact is at best execution. Must use market orders |

|

|

Need-trustworthy-agent trading focus |

Employ broker to skillfully execute large trade in a security, which may be thinly traded. Weakness: commissions may be high and trader may reveal his trade intentions to the broker. |

|

|

Advertise-to-draw-liquidity trading focus |

Trade is publicized in advance to draw counterparties to the trade. Weakness: another trader may front run the trade, buying in advance of a buy order |

|

|

Low-cost-whatever-the-liquidity trading focus |

Place limit order outside current bid-ask quotes in order to minimize trading costs. Passive and value-motivated traders will offer pursue this strategy. |

|

|

Algorithmic trading |

The use of automated, quantitative systems that utilize trading rules, benchmarks, and contraintes to execute orders with minimal risk and costs. Strategies classified into logical participation strategies, opportunities strategies and specialized strategies |

|

|

Types of algorithmic trading strategies |

1. Logical participation strategies (simple logical and implementation shortfall strategies) 2. Opportunistic strategies 3. Specialized strategies |

|

|

Simple logical participation strategies |

Seek to trade with mkt flow so as to not become overly noticeable to the mkt and to minimize mkt impact. |

|

|

Implementation shortfall strategies |

(or arrival price strategies) Minimize trading costs as defined by the implementation shortfall measure or total execution costs. |

|

|

Opportunistic participation strategies |

Trade passively over time but increase trading when liquidity is present |

|

|

Specialized strategies |

Include passive strategies and other miscellaneous strategies |

|

|

VWAP strategy |

Seek to match or do better than day's VWAP |

|

|

Time-weighted average price strategy (TWAP) |

Spreads the trade out evenly over the whole day as to equal a TWAP benchmark. Used for thinly traded stock with volatile, unpredictable intraday trading volune |

|

|

Best execution vs prudence |

Prudence = selecting security most appropriate for an investor Best execution = best means to buy/sell those securities Both attempt to improve portfolio performance and meet fiduciary responsibilities |

|

|

Characteristics of best execution |

1. Depends on VA of trade vs cost 2. Best execution and VA cannot be known ex ante 3. Best execution and cost can only be calculated ex post. 4. Relationships and practices = integral to best execution. Best execution is ongoing and requires diligence and dedication to the process. |

|

|

Trade management guidelines |

1. Processes (have policies, procedures that have intent of maximizing portfolio value using best execution) 2. Disclosures (firm should provide disclosure to their clients &potential clients regarding (a) general info on trading techniques, mkts, brokers (b) conflict of interest related to trading) 3. Record keeping (firm should maintain documentation supporting (a) firm's compliance (b) disclosures made to its clients |