Reading...

![]()

Play button

![]()

Play button

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

15 Cards in this Set

- Front

- Back

|

Define and give examples of, a social science

|

A study of people in society and how they interact with each other. e.g. psychology, sociology, political science etc

|

|

|

Define and give examples of, and distinguish between, goods and services; needs and wants; economic goods and free goods

|

Goods - physical objects that are capable of being touched (tangible goods) e.g. cars, meat, vegetables

Services - intangible things that cannot be touched e.g. motorbike repairs, haircuts etc. Needs - things that we must have to survive e.g. food shelter Wants - things that we would like to have but which are not necessary for our survival Economic good - any good or service that has a price, and is thus being rationed (has opportunity cost) Free good - goods which do not have a price and therefore are not relatively scarce |

|

|

Define opportunity cost and understand its link to relative scarcity and choice

|

Opportunity cost - the next best alternative foregone when an economic decision is made

People have to decide how to allocate their limited financial resources and so always need to choose between alternatives |

|

|

Explain the basic economic questions: "What to produce?", "How to produce?", and "Who to produce for?"

|

What is required to be produced and in what quantities? Is there high demand for a particular product?

There are multiple ways to produce a product e.g. organically, by an automated production line etc. Should the product be available to those who can afford it or be shared in some "fair" manner? |

|

|

Describe the factors of production

|

Land - all natural resources

Labour - the human workforce; the physical and mental contribution of the existing workforce to production Capital - investment in physical capital and human capital. Physical capital - machinery, roads, tools. Human capital - skills of workers which can be improved through education Management (entrepreneurship) - the organising and risk-taking factor of production. Entrepreneurs organise the other factors of production to produce goods and services |

|

|

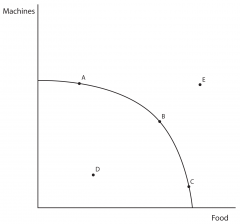

Explain, illustrate, and analyse production possibility curves

|

A PPC shows the maximum combinations of goods and services that can be produced by an economy in a given time period, if all resources in the economy are being used fully and efficiently and the state of technology is fixed

In this case, the economy can only produce machines or food. At point D, it is producing within its PPC and therefore resources are not being used efficiently. At point B it produces on its PPC which means the resources are being used efficiently. Point E is unattainable unless the economy itself expands, i.e, there is an increase in the quality or quantity of the economy's aggregate supply |

|

|

Distinguish between microeconomics and macroeconomics; positive economics and normative economics; private sector and public sector

|

Microeconomics deals with smaller, discrete economic agents and their reactions to changing events e.g. individuals and individual firms

Macroeconomics takes a wider view and considers such things as measuring all the economic activity in the economy such as inflation, unemployment etc. Positive economics deals with areas of the subject that are capable of being proved to be correct or not Normative economics deals with areas of the subject that are open to personal opinion and belief. Private sector - The part of the economy that is not state controlled, and is run by individuals and companies for profit Public sector - The part of national economy providing basic goods or services that are either not, or cannot be, provided by the private sector and is controlled by the government |

|

|

Define and explain ways of measuring utility

|

Utility is a measure of usefulness and pleasure.

Total utility - the total satisfaction gained from consuming a certain quantity of a product. Marginal utility- the extra utility gained from consuming one more unit of a product. |

|

|

Explain that economists are model builders and that they employ the assumption of "ceteris parabus"

|

Economists build theoretical models in order to test and illustrate their theories. The models may then be manipulated in order to see what the outcome will be if there is a change in one of the variables.

This method is known as "ceteris barabus" (all other things being equal). |

|

|

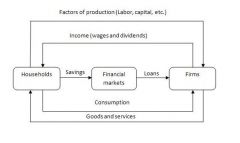

Explain and illustrate a basic model of an economy

|

In this model, households represent the group of individuals in the economy who perform two functions. They are the owners and providers of the factors of production that are used to make goods and services. Firms represent the productive units in the economy that utilise the FoP to make goods and services

|

|

|

Distinguish between different rationing systems

|

Planned economy - Decisions about the answers to the basic economic questions are made by the government. All resources are collectively owned, and government bodies arrange all production, and set prices through central planning.

Free market economy - Prices are used to ration goods and services. All production is in private hands and demand and supply are left free to set wages and prices in the economy. |

|

|

Give the disadvantages of a planned economy

|

1. Total production, investment, trade etc are too complicated to plan efficiently and there will be a misallocation of resources

2. Because there is no price system in operation, resources will not be used efficiently. Arbitrary decisions will not be able to make the best use of resources 3. Incentives tend to be distorted 4. The dominance of the government may lead to a loss of personal liberty and freedom of choice 5. Governments may not share the same aims as the majority of the population |

|

|

Give the disadvantages of a free market economy

|

1. Demerit goods will be over-provided driven by high prices

2. Merit goods will be underprovided 3. Resources may be used too quickly and the environment may be damaged by pollution, as firms seek to make high profits to minimize cost 4. Some members of society will not be able to look after themselves and will not survive 5. Large firms may grow and dominate industries, leading to high prices, a loss of efficiency, and excessive power |

|

|

Distinguish between economic growth and economic development

|

Economic growth is an increase in actual output, a movement from a point inside the PPC to a point nearer to the curve.

Economic development is a measure of welfare, a measure of well-being. It is used to measure economic development not just in monetary terms. |

|

|

Define sustainable development

|

Sustainable development - development that meets the needs of the present without compromising the ability of future generations to meet their own needs

|