![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

119 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

American Put Early exercise is optimal if |

PV (Interest on the strike K) > PV (Dividends) + Implicit Call By exercising a put option early - Get cash earlier, so you earn interest on K - Give up implicit call opt - Give up dividends |

|

|

|

American Call - non dividend paying stock Early exercise is optimal if |

Early exercise is never optimal. C amer = C eur Lose protection against the price of the stock going below K. Lose interest on K. |

|

|

|

American Call - dividend paying stock Early exercise is optimal if |

PV (Dividends) > PV (Interest on the strike K) + Implicit Put if early exercise is rational, exercise should be right before a div. is paid, in order to maximize the interest. |

|

|

|

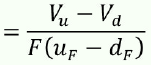

Put-Call Parity (PCP) Prepaid Forward & Forward |

|

|

|

|

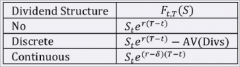

Put-Call Parity Prepaid Forward - Dividend Structure |

|

|

|

|

Put-Call Parity Forward - Dividend Structure |

|

|

|

|

PCP for Stock C - P = |

|

|

|

|

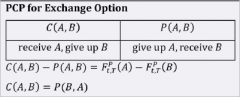

PCP for Exchange Option C(A, B) |

|

|

|

|

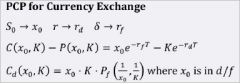

PCP for Currency Exchange S --> ? r --> ? δ --> ? |

|

|

|

|

PCP for Bonds C - P = Bt = |

|

|

|

|

Comparing Options - Different Strike Prices For K1 < K2 < K3: CALL C(K1) ? C(K2) ? C(K3) C(K1) - C(K2) ? K2 - K1 European: C(K1) - C(K2) ? PV(K2 - K1) [C(K1)-C(K2)]/[K2 - K1] ? [C(K2)-C(K3)]/[K3-K2] |

|

|

|

|

Comparing Options - Different Strike Prices For K1 < K2 < K3: Put P(K1) ? P(K2) ? P(K3) P(K1) - P(K2) ? K2 - K1 European: P(K2) - P(K1) ? PV(K2 - K1) [C(K2)-C(K1)]/[K2 - K1] ? [C(K3)-C(K2)]/[K3-K2] |

|

|

|

|

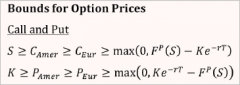

Comparing Options - Bounds for Option Prices Call and Put |

|

|

|

|

Comparing Options - Bounds for Option Prices European vs. American Call |

|

|

|

|

Comparing Options - Bounds for Option Prices European vs. American Put |

|

|

|

|

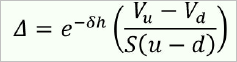

Binomial Model Replicating Portfolio |

An option can be replicated by buying delta shares of the underlying stock and lending B at the risk-free rate. |

|

|

|

Binomial Model Replicating Portfolio Delta = |

Delta - shares of underlying stock |

|

|

|

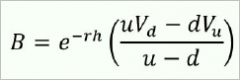

Binomial Model Replicating Portfolio B = |

Lending B @ risk-free rate. If - then borrow to purchase stock.

|

|

|

|

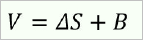

Binomial Model Replicating Portfolio V = option premium = |

|

|

|

|

Binomial Model Replicating Portfolio Table |

|

|

|

|

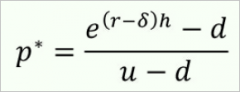

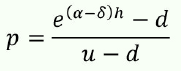

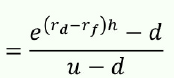

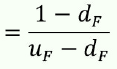

Risk-neutral Probability Pricing p* = |

|

Probability stock will increase in value. |

|

|

Risk-neutral Probability Pricing V = |

|

|

|

|

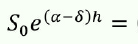

Risk-neutral Probability Pricing Se^[(r-δ)h] = |

|

|

|

|

Realistic Probability Pricing p = |

|

|

|

|

Realistic Probability Pricing V = |

|

|

|

Realistic Probability Pricing |

|

|

|

Realistic Probability Pricing |

|

|

|

|

Standard Binomial Tree (Forward Tree) u = d = |

|

|

|

|

Binomial Model - Option on Currencies S --> ? r --> ? δ --> ? u = d = |

S --> x0 r --> rd δ --> rf |

|

|

|

Standard Binomial Tree (Forward Tree) p* = ... = ... |

Interestingly, r and δ don't affect p*. |

Risk neutral probability will be close to 0.5 |

|

|

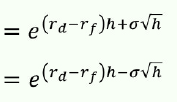

Cox-Ross-Rubinstein Tree u = d = |

Centered on 1 |

If e^(r-δ) > e^σ sqrt h, violates arbitrage-free since both u & d are < e^(r-δ). With h small enough this won't happen. |

|

|

Lognormal Tree (Jarrow-Rudd Tree) u = d = |

Centered on e^(r-δ-.5σ^2)h |

|

|

|

No Arbitrage Condition |

Arbitrage is possible if the following inequality is not satisfied: d < e^[(r-δ)h] < u Means the upper node must be higher than the result of a risk-free investment and the lower node must be lower. |

|

|

|

Binomial Model - Option on Currencies S --> ? r --> ? δ --> ? p* = |

S --> x0 r --> rd δ --> rf |

|

|

Binomial Model - Option on Futures Contracts |

|

|

|

|

Binomial Model - Option on Futures Contracts T = TF = T=< St --> δ --> |

T = Expiration date of the option T = Expiration date of the futures contract T =< TF St --> Ft,TF δ --> r |

|

|

|

Binomial Model - Option on Futures Contracts p* = |

= 1/(1+u) if tree is based on forward prices

|

|

|

|

Binomial Model - Option on Futures Contracts Δ = # of forwards in replicating portfolio |

F = Futures contract price

|

|

|

|

Binomial Model - Option on Futures Contracts B = Option premium since there's no initial cost for futures |

|

|

|

|

Binomial Model - Utility Values and State Prices Options on Futures (not stocks) Uu: Ud: |

Uu: Utility value per dollar in the up state Ud: Utility value per dollar in the down state |

|

|

|

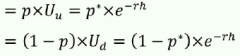

Binomial Model - Utility Values and State Prices Qu = ... = ... Qd = ... = ... |

|

|

|

|

Binomial Model - Utility Values and State Prices e^(-rh) |

= Qu + Qd |

|

|

|

Binomial Model - Utility Values and State Prices S = |

|

|

|

|

Binomial Model - Utility Values and State Prices V = |

= QuVu + QdVd |

Vd = cash flow of the stock at the EOY 1. |

|

|

Binomial Model - Utility Values and State Prices p* = |

= Qu / (Qu + Qd) |

Qi = current value of $1 paid @ EOY 1. |

|

|

ɣ |

discounting rate for option must be the same as the discounting rate for the replicating portfolio |

|

|

Binomial Model |

|

|

|

|

Futures vs. Forward Definition |

A Forward agreement is a customized contract. Futures contract is standardized / marked to market daily. Exchange traded fwd contract. |

|

|

|

The one who sells the call option is called the ... |

writer. |

|

|

|

Buy x, we are... x |

long x |

|

|

|

Sell x, we are ... x |

short x |

|

|

|

How to create a Bull Spread with Puts & Calls |

Buy K1 & sell K2. K2 > K1 |

|

|

|

How to create a Bear Spread with Puts & Calls |

Buy K2 & sell K1. K2 > K1 |

|

|

|

A Bull Spread from the perspective of the purchaser is a ... |

bear spread from the perspective of the writer. |

|

|

|

Ratio Spread |

Buy n of one option, and Sell m of another option of the same type m does not equal n |

|

|

|

Box Spread |

Agreement to buy stock @ K1 and sell it for K2. So profit = K2 - K1 (should be no gain/loss). |

|

|

|

Box Spread is a ... option strategy |

4: Bull Spread Calls & Bear Spread Puts K Bull Spread Bear Spread K1 buy call sell put K2 sell call buy put |

|

|

|

Butterfly spreads is a ... option strategy. |

3: all same type. |

|

|

|

Option prices as a function of K must be ... |

convex. |

|

|

|

Collars |

buying one option & selling an option of the othre kind. No risk. No profit or loss. |

|

|

|

Straddle |

buying 2 options of different kinds. It's a bet on volatility. (Strangle is a special subset.) |

|

|

|

Conversion |

Creating a synthetic Treasury |

|

|

|

Reverse Conversion |

Shorting stock, buy call, sell put |

|

|

|

Asset sold |

Underlying asset, St |

|

|

|

Asset want / buy |

Strike asset, Qt |

|

|

|

Foreign risk-free rate |

role of a stock to be purchased for a call option or sold for a put option. S and δ |

|

|

|

Domestic risk-free rate |

role of a cash in stock. Owner pays in a call or one which owner receives in put. The one in which the price is expressed. K |

|

|

|

Foreign Currency |

underlying asset of option |

|

|

|

TRUE / FALSE If settlement is through cash (not in currency exchange) then put options may not have the same payoff as the call option. One in f while call in domestic. Exchange rate X may be different at time t. |

TRUE |

|

|

|

A Call option cannot be worth more than ... |

underlying stock. |

|

|

|

A Euro Call cannot be worth more than ... |

prepaid forward price of the stock. If cont divs then upper bound is Se^(-δt). |

|

|

|

A Put cannot be worth more than ... |

K. |

|

|

|

A Euro Put cannot be worth more than ... |

Ke^(-rt) |

|

|

|

TRUE / FALSE An option must be worth at least zero since no negative payoff. |

TRUE |

|

|

|

A Euro option is worth at least as much as implied by ... |

Put-Call parity. |

|

|

|

For both Calls and Puts, list in order of greatest to least: S or K American option European option Max(0, Fp - Ke^(-rt)) or Max(0, Ke^(-rt) - Fp) |

S >= C amer >= C eur >= Max(0, Fp - Ke^(-rt)) K >= P amer >= P eur >= Max(0, Ke^(-rt) - Fp) |

|

|

|

TRUE / FALSE Every call option has an implicit put option built into it. Similarly, every put option has an implicit call option built into it. |

TRUE |

|

|

|

For a Euro Put option, longer time to expiry may make the PV of cash received... |

lower. |

|

|

|

A longer-lived American Call option with K increasing at the risk-free rate must be worth at least as much as a ... |

shorter-lived option. |

|

|

|

TRUE / FALSE

Longer lived American Put option is at least as valuable as the shorter-lived one, dividends or not; an increase in K is a perk. |

TRUE |

|

|

|

TRUE / FALSE An American option with expiry T and K must cast at least as much as the one with expiry t and K. |

TRUE Also true for a Euro Call option. |

|

|

|

TRUE / FALSE

A Euro Option on a nondiv paying stock with expiry T and Ke^r(T-t) must cost at least as much as one with expiry t and k. |

TRUE This statement is stronger than the previous statement & includes it. Since it applies to both calls & puts, and increases in K make calls worth less. |

|

|

|

The higher K Call |

then lower premium. The premium for a call decreases more slowly than K increases. |

|

|

|

The higher K Put |

then higher premium. The premium for a put option increases more slowly than K increases. |

|

|

|

Three inequalities - if don't hold then arbitrage |

Direction, Slope, Convexity |

|

|

|

Convexity |

Option premiums are convex. Convexity involves 3 options. |

|

|

|

Arbitrage mispricing |

If there's a mispricing, the option in the middle will be overpriced relative to other two options. So sell the middle option and buy the ones at the 2 extremes. |

|

|

|

TRUE / FALSE If a put with K1 is optimal to exercise, then so is an otherwise similar put with K=K2 > K1. |

TRUE |

|

|

|

Two ways to price options |

1. Binomial tress 2. Black Scholes |

|

|

|

Risk-Neutral assumption |

Satisfied to earn the risk-free rate on a risky asset. An option can be priced using risk-neutral prob. discounted at the risk-free rate. |

|

|

|

Law of one price |

If two portfolios lead to the same outcomes in all scenarios, they must have the same price. |

|

|

|

Risk-neutral pricing is equivalent to pricing with ... |

pricing with a replicating portfolio. |

|

|

|

B (bond) |

Amount we lend when positive. Lend @ risk-free rate. |

|

|

|

Intercept |

The intercept (the maturity value of the amt to lend) is the balancing item. |

|

|

|

Run = |

uS - dS = (u-d)S |

|

|

|

Volatility |

square root of variance

|

|

|

|

Volatility sigma_h = |

= sigma \sqrt{h} Default is annual volatility. |

|

|

|

Standard Binomial Tree Forward Tree |

Tree is based on forward prices and "the usual method in McDonald" |

|

|

|

Δ decreases to ? as the put gets further into the money. |

-1 |

|

|

|

For a call, Δ increases to ? as the call gets further into the money. |

+1 |

|

|

|

Futures contract - Early exercise |

Exercising the option enters one into a futures contract, allowing one to earn interest on the mark-to-market $. |

|

|

|

Pricing Options on Futures |

Assume Futures have the same price as Forwards. |

|

|

|

TRUE / FALSE An option may have the same expiry as the futures contract, or the futures contract may expire later. |

TRUE |

|

|

|

Futures Contract |

Pays no dividends. Almost all options on Futures are American style. |

|

|

|

Futures Contract # of shares in replicating portfolio = |

e^ (-rh) * Δ |

|

|

|

For a bond, the coupon rate serves the purpose of the ... |

dividend yield. |

|

|

|

TRUE / FALSE Bond values must converge to their maturity value, or possibly their call value if they're callable. |

TRUE |

|

|

|

Bonds are MORE/LESS volatile as period to maturity decreases. So cannot project values using fixed volatility rate. |

LESS |

|

|

|

The best way to project bond values is to project |

interest rates. |

|

|

|

Underling asset - Dividend Yield Stock/Stock Index Currency Futures Contract Bond |

Dividend Yield Dividend Yield Foreign risk free rate Risk free rate b (r) Coupon yield |

|

|

|

The discounting rate for a put option is negative since... |

you invest money at the risk-free rate & sell an asset on which you must pay a higher discounting rate. |

|

|

|

Even though the return on the underlying asset is constant, the return on the option ... |

varies by period. |

|

|

|

Price of an option computed using risk-neutral prob & discounting with r equals... |

the price using true prob. & discounting the stock with α and the option with ɣ |

|

|

|

Early exercise optimal? Higher volatility |

Less likely early exercise is optimal because of the increased value of the implicit call |

|

|

|

Random Walk |

Binomial variable in each unit of time, and as the # of periods go to infinity, the position converges to a normal dist. by CLT. |

Central Limit Theorem |

|

|

Since we're multiplying rather than adding moves to model stock prices .. |

the stock price converges to the exponential of a normal dist. or a lognormal dist. |

|

|

|

Lognormal Model for Stock prices Assumptions |

1. Volatility is constant 2. Stock returns for diff. time periods are indep. 3. Large stock movements do not occur; stock prices do not jump. |

All of these assumptions appear to be violated in practice. |

|

|

Cox-Ross-Rubinstein tree & Lognormal tree |

Do not guarantee arbitrage-free. Upper node > forward price Lower node < forward price |

|

|

|

Binomial model For an infinitely lived Call option on a stock with σ = 0, |

exercise is optimal if Sδ > Kr |

|