![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

58 Cards in this Set

- Front

- Back

|

two goods are substitutes if an increase in the price of one... |

leads to an increase in the quantity demanded of the other |

|

|

two goods are complements if an increase in the price of one leads to... |

a decrease in the quantity demanded of the other

|

|

|

a competitive market is economically efficient because it |

maximizes aggregate consumer and producer surplus |

|

|

production functions describe technical efficiency |

as being achieved when a firm uses each combination of inputs as effectively as possible |

|

|

exchange economy |

market in which two or more consumers trade two goods among themselves |

|

|

pareto efficient allocation |

allocation of goods in which no one can be made better off unless someone else is made worse off |

|

|

edgeworth box |

diagram showing all possible allocations of either two goods between two people or of two inputs between two production processes |

|

|

how do you know if a new allocation is efficient in edgeworth box? |

|

|

|

competitive equilibrium |

set of prices at which the quantity demanded quals the quantity supplied in every market |

|

|

Adam Smith's invisible hand |

the economy will automatically allocate resources in a Pareto efficient manner without the need for regulatory control |

|

|

welfare economics |

normative evaluation of markets and economic policy: if everyone trades in the competitive marketplace, all mutually beneficial trades will be completed and the resulting equilibrium allocation of resources will be Pareto efficient |

|

|

Four views of equity |

1. egalitarian - all members of society receive equal amounts of goods 2. rawlsian - maximize the utility of the least-well-off person 3. utilitarian - maximize the total utility of all members of society 4. market-oriented - market outcome is the most equitable |

|

|

technical efficiency |

condition under which firms combine inputs to produce a given output as inexpensively as possible |

|

|

production possibilities frontier |

curve showing all efficient combinations of outputs PPF is concave because its slope (the marginal rate of transformation - MRT) increases as the level of production of food increases |

|

|

when output markets are perfectly competitive, all consumers allocate budgets so MRS = |

price ratio: MRS = Pf / Pc so Pf = MCf and Pc = MCc |

|

|

country 1 has a comparative advantage over country 2 in producing a good if: |

the cost of producing that good, relative to the cost of producing other goods in 1, is lower than the cost of producing eh good in 2, relative to the cost of producing other goods in 2 **when each of two countries has comparative advantage, they are better off producing what they are best at and purchasing the rest |

|

|

country has an absolute advantage in producing a good if: |

its cost is lower than the cost in other country |

|

|

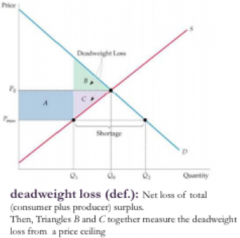

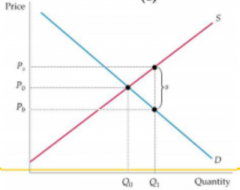

deadweight loss |

|

|

|

economic efficiency |

When the allocation of resources is such that the sum of aggregate consumer and producer surplus is maximized |

|

|

price ceiling |

|

|

|

market failure |

Situation in which an unregulated market is inefficientbecause prices fail to provide proper signals to consumers andproducers. There are three important instances in which market failurecan occur:

|

|

|

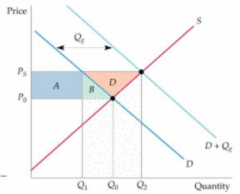

price supports |

Governments set prices above free-marketlevel and maintain them high through purchases of excess supply ∆CS + ∆PS − Cost to Govt. = D −(Q2 − Q1)Ps |

|

|

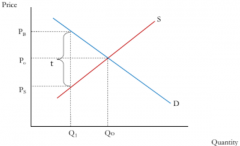

No matter on what side the tax is imposed on, define PB (the price paid bybuyers) and Ps (the price that sellers receive) |

Then, PB- PS=t If on consumers: PB=PS+t If on producers: PS = PB- t |

|

|

If demand is very inelastic relative to supply,the burden of the tax falls mostly on buyers. |

|

|

|

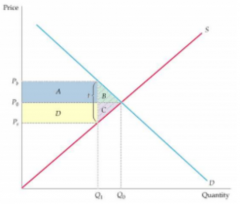

social burden of a tax |

Buyers lose A + B. Sellers lose D + C. The gov earns A + D inrevenue. The deadweight loss is B + C. |

|

|

subsidy |

Payment reducing the buyer’s price below the seller’s price |

|

|

pareto efficiency |

in an efficient allocation of goods,no one can be made better off without makingsomeone else worse off |

|

|

1st Theorem of Welfare Economics |

“If all economic agents are price takers, themarket equilibrium allocation will be Paretoefficient”. All mutually beneficial trades will be completed. |

|

|

2nd Theorem of Welfare Economics |

“Every efficient allocation (every point on the contractcurve) is a competitive equilibrium for some initialallocation of goods”. |

|

|

definition of externality |

Externalities are effects of production andconsumption activities on other production orconsumption activities, not directly reflected inmarket prices. |

|

|

negative externality |

when the action of one party imposes costson other parties (pollution or, more generally, torts) negative externalities imply excessproduction and unnecessary social cost. |

|

|

positive externality |

when the action of one party producesbenefits for other parties (voluntaries cleaning publicparks, a beekeeper who benefits from neighboringgardens) Positive externalities imply insteadunderproduction and too low social benefits. |

|

|

Inefficiency of Externalities |

When there are externalities, the price of a gooddoes not reflect its social value. Firms may then produce too much or too little,so the quantity traded in the market mightnot be the efficient one. The efficient level of production is where MSC=MC+MECequals price, at q*. |

|

|

Correcting Externalities |

Standards set thequantity of emissionsat E*. Firms which donot comply areheavily fined. Fees charges firmsfor each unit ofpollutant emitted. |

|

|

Tradeable Emission Permits |

System of marketable permits specifying the maximum level of emissionsthat can be generated, initially allocated among firms and then traded. |

|

|

Coase Theorem |

“When parties can bargain without cost and to their mutual advantage, the resultingoutcome will be efficient regardless of how property rights are specified” |

|

|

Public goods |

Non-rival good: Good for which the marginal cost of offering it to an additional consumer is zero. Non-exclusive good: people can't be excluded fromconsuming the good, so that it is difficult or impossible tocharge for its use. |

|

|

the main problem of public goods |

The main issue in the private provision of public goods isthe presence of Free Riders Since there is no way to provide these goods andservices without effectively benefiting everybody,families would have no incentive to pay what the goodis in fact worth to them. In other terms, they exhibit afree rider attitude, underscoring the value of the good orservice in order to enjoy it without suffering its cost. |

|

|

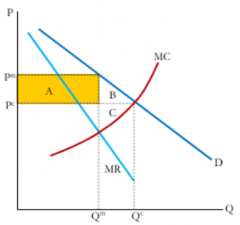

monopoly |

a single firm is the sole producer of thegood: It is a price maker. It can change price and quantity without having toworry about the (strategic) reaction of competitors. i.e. Its demand curve is the entire market demandand is negatively sloped. The ability to make profits are limited by demandconditions. TR(Q)=P(Q)Q |

|

|

in a monopoly, the rule for profit maximization is |

the rule for profit maximization isMR = MC |

|

|

definition of price-elasticity of demand: |

|

|

|

DWL in Monopoly |

|

|

|

Regulation through price ceilings («marginal costpricing») by Governments can limit market power.However, it is not always effective: |

|

|

|

Antitrust Laws in the US |

Antitrust Laws act with the aim of promoting competitiveeconomies by prohibiting actions that restrain or might restraincompetition. Sherman Act (1890): Section 1 prohibits contracts, combinations or conspiracies inrestraint of trade (both explicit and implict, as in “ParallelConduct” ). Section 2 makes it illegal to monopolize or attempting tomonopolize a market and prohibits conspiracies that result inmonopolization (i.e., with exclusive dealing or predatorypricing). |

|

|

Conditions for Price Discrimination |

1. The firm must be a price maker.

|

|

|

First-degree (perfect) price discrimination: |

the firmis able to sell each unit of output at a price just equal tothe buyer’s maximal willingness to pay for that unit |

|

|

Second-degree price discrimination: |

the firm charges different prices according to the quantity (bulk discounts) or the type of service (fast, accurate, etc.) a customer purchases. The firm is not able to observe the type of the customer but it is the customer itself that“self-selects” on the basis of the offers made by the firm. |

|

|

Third-degree price discrimination: |

The firm observes some characteristics of the buyers that indicate their willingness to pay. It then charges different prices to different types. |

|

|

Efficiency of Monopolistic Competition |

|

|

|

Oligopoly |

|

|

|

NASH Equilibrium |

a firm is in equilibrium when itchooses the course of action that is the bestresponse to what its competitors are doing |

|

|

Cournot Competition |

|

|

|

Profit Maximization in the Cournot Model |

|

|

|

Collusion |

|

|

|

Bertrand Model |

|

|

|

Prisoner’s Dilemma |

|

|

|

How is the price elasticity of demand related to the optimal price set by a monopolist accordingto the rule of thumb of monopoly pricing? |

|

|

|

Explain why goods will not be distributed efficiently among consumersif the MRT is not equal to the consumers’ marginal rate of substitution. |

If the marginal rate of transformation, MRT, is not equal to the marginal rate ofsubstitution, MRS, we could reallocate inputs in producing output to leave the consumersand producers better off. If the MRS is greater than the MRT then consumers are willing topay more for another unit of good x (in terms of good y) than it will cost the producers toproduce it (again in terms of good y). Both consumers and producers can therefore be madebetter off by arranging a trade somewhere between what consumers are willing to pay andwhat the producers have to pay to produce the extra units of x. This also means that thecurrent output combinations is not optimal, and more units of x and less of y will beproduced until MRS=MRT. Note also that when MRT ≠ MRS, the ratio of marginal costswill not be equal to the ratio of prices. This means that one good is being sold at a pricebelow marginal cost and one good is being sold at a price above marginal cost. We shouldincrease the output of the good whose price is above marginal cost and reduce the outputof the other good whose price is below marginal cost. |