![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

96 Cards in this Set

- Front

- Back

|

Law of demand |

A goods price falls with more demand |

|

|

Extension of demand/supply Contraction of demand/supply |

An adjustment it movement down/ up the curve Up/down curve |

|

|

Rational behaviour |

Acting with a pursuit of self interest, consumers maximise welfare |

|

|

Utility |

The satisfaction or economic welfare an individual gains from consuming a good or service |

|

|

Marginal utility |

The additional welfare, satisfaction or pleasure gained from consuming one extra unit of a good |

|

|

Hypothesis of diminishing marginal utility |

For the a single consumer the marginal utility derived from a good or served diminishes for each additional unit consumed |

|

|

Asymmetric information |

When one party yo a market transaction possesses less information relevant to the exchange than the other |

|

|

Behavioural economics |

A method of economic analysis that applies psychological insights into human behaviour to explain how individuals make choices and decisions |

|

|

Rule of thumb |

A rough and practical method that can easily be applied when making decisions |

|

|

Bounded rationality |

When making decisions an individuals rationality is limited bu the information they have the limitations their mind and the finite amount of time available to make a decision |

|

|

Bounded self control |

Limited self control which individuals lack the self control to act in what they see as their self interest |

|

|

Cognitive bias |

A mistake in reasoning or in some other mental process occurring as a result of for example rules of thim or holding preferences regardless of contrary information |

|

|

Availability bias |

Occurs when individuals make judgements about the likelihood of future events according to how easy it is to recall examples of similar events |

|

|

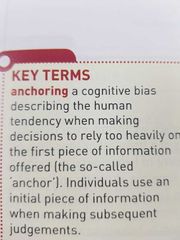

Anchoring |

|

|

|

Social norms |

Forms of patterns of behaviour considered acceptable bu a society or group within society |

|

|

Economic sanctions |

Restrictions imposed by regulations and or laws that restrict an individuals freedom to behave in certain ways. Breaking a sanction can lead to a punishment |

|

|

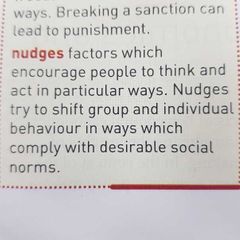

Nudges |

|

|

|

Altruism |

Concern for the welfare if others |

|

|

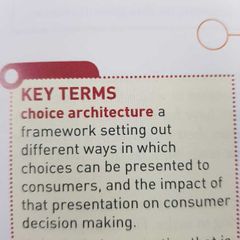

Choice architecture |

|

|

|

Default choice |

An option that is selected automatically unless an alternative is specified |

|

|

Framing |

How something is presented influences the choices people make |

|

|

Mandated choice |

People are required bu law to make a decision |

|

|

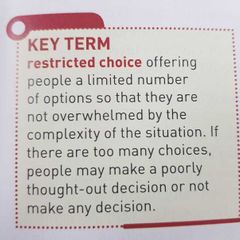

Restricted choice |

|

|

|

Marginal returns of labour |

|

|

|

Law of diminishing returns |

|

|

|

Average returns of labour |

Total output divided by the toqk number if workers employed |

|

|

Total returns of labour |

Total output produced by all the workers employed by a firm |

|

|

Productivity |

Output per unit if input |

|

|

Labour productivity |

Output per worker |

|

|

Returns to scale |

The rate by which output changes if the scale of all favors of production is changed |

|

|

Increasing/ constant/ decreasing returns to scale |

When the scale if all the factors of production employed increases, out put increases at a faster rate/ same rate/ slower rate. |

|

|

(Dis)Economy of scale |

As output increases long run average cost falls(rises) |

|

|

Long run average cost |

Cost per unit of output incurred when all factors of production or inputs can be varied |

|

|

Optimum firm size |

The size of a firm capable of producing at the lowest average cost and this being productively efficient |

|

|

Minimum efficiency scale |

The lowest output at which the firm is able to produce at the minimum achievable LRAC |

|

|

Minimum efficiency scale |

The lowest output at which the firm is able to produce at the minimum achievable LRAC |

|

|

(External) Internal economies and diseconomies of scale |

Changes in long run average costs of production resulting from increases in the size or scale of a firm or plant (vs growth of market or industry of which the firm is part of) |

|

|

Marginal cost |

Addition to total cost resulting from producing one additional unit of output |

|

|

Average fixed cost |

Total cost of employing the fixed factors of production to produce a particular level of output, divided by the size of output AFC=TFC÷Q |

|

|

Average variable cost |

|

|

|

Average total cost |

Total cost of producing a particular level of output divided by the size of output ATC=AFC+AVC aka average cost |

|

|

Long run marginal cost |

|

|

|

Long run average cost |

|

|

|

Total revenue |

All the money received by a firm from selling its total output |

|

|

Average revenue |

Total revenue divided by output |

|

|

Marginal revenue |

Addition to total revenue resulting from the sale of one more unit of product |

|

|

Price taker |

A firm which is so small that it has to accept the ruling market price. If the firm raises its price it loses all its sales if it cuts its price it gains jo advantages |

|

|

Price maker |

When a firm faces a downward sloping demand curve for its product, it possesses the market power to set the price at which it sells the product |

|

|

Quantity setter |

When a firm faces a downward sloping demand curve for its product it possesses the market power to set the quantity of the good it wishes to sell |

|

|

Profit maximization |

Occurs at the level of output at which total profit is greatest |

|

|

Normal profit |

The minimum profit a firm must make to stage in business however insufficient to attract new firms into the market |

|

|

Abnormal profit |

Profit over and above normal profits. Aka supernormal profit |

|

|

Productive efficiency |

The level of output at which average costs of production are minimised |

|

|

Dynamic efficiency |

Occurs in the log run leading to the development of new products and more efficient processes that improve productive efficiency |

|

|

Monopolistic completion |

A market structure in which firms have many competitors bit each sell slightly dif products |

|

|

Duopoly |

Two firms only in the market |

|

|

Creative destruction |

Capitalism evolving and renewing itself over time through new technology and innovations replacing older technologies and innovations |

|

|

Entry barriers |

Obstacles that make it difficult for a new firm to enter a market |

|

|

Natural barriers |

Barriers that result from inherent features of the industry such as economies of scale or high research and development costs |

|

|

Sunk costs |

Costs that have already been incurred and cannot be recovered |

|

|

Artificial barriers |

Bstrieres erected by the firms themselves such as high levels of advertising expenditure ot predatory pricing |

|

|

Limit prices |

Prices set low enough to make it unprofitable for others firms to enter market |

|

|

Predatory pricing |

Prices set below average cost or very cheaply with the aim of forcing rival firms out of business |

|

|

Product differentiation |

The marketing of generally similar products with minton variations or the marketing of a range of different products |

|

|

Divorce of ownership from control |

The owners those who manage the firm are different groups with different objectives |

|

|

Satisficing |

Achieving a satisfactory outcome father than the best possible outcome |

|

|

Monopoly |

One firm in the market |

|

|

Static efficiency |

Efficient at a particular point in time |

|

|

Allocatuve efficency |

Occurs when it is impossible go improve overall economic welfare bu reallocaging resources between markets Price equals marginal cost in every market P=MC |

|

|

Private costs and benefits |

|

|

|

Social costs and benefits |

|

|

|

Monopoly power |

|

|

|

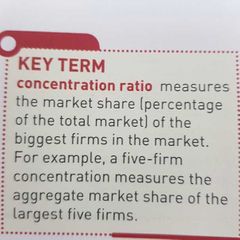

Concentration ratio |

|

|

|

Cartel |

|

|

|

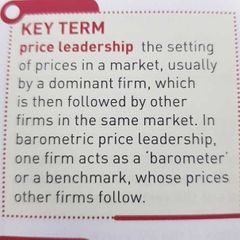

Price leadership |

|

|

|

Price agreement |

An agreement between a firm and similar firms suppliers or customers regarding the pricing of a good or service |

|

|

Price War |

Occurs when rival firms continuously lower prices to undercut each other |

|

|

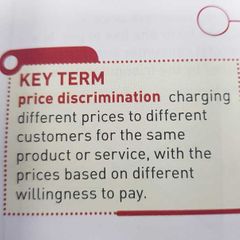

Price discrimination |

|

|

|

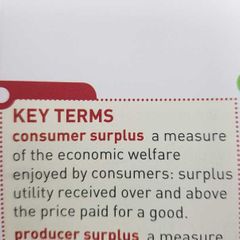

Consumer surplus |

|

|

|

Producer surplus |

|

|

|

Contestabel market |

|

|

|

Hit and run competition |

|

|

|

Dead weight loss |

|

|

|

Derived demand |

|

|

|

Marginal physical product of labour |

The addition to a forms total output brought about by employing one more worker |

|

|

Marginal revenue product of labour |

The money value of the addition to a firms total output brought about nu employ one more worker |

|

|

Elastxify of demand for labour |

Proportionate change in demand for labour following a change in the wage rate |

|

|

Substitution effect |

A higher hourly wage rate makes work more attractive than leisure so workers substitute labour for leisure |

|

|

Income effect |

An increase in the hourly wage rate means higher real income and if pleasure is a normal good the quantity of leisure demanded goes up which means a reduction in the quantity of labour supplied |

|

|

Net advantage |

The sum of the monetary and non monetary benefits of working |

|

|

Eleastcity of supply of labour |

|

|

|

Average cost of labour |

Total wage costs divided by the number of workers employed |

|

|

Marginal cost of labour |

The addition to films total cost of prediction resulting from employing one more worker |

|

|

Monopsony |

There is only one buyer in the market |

|

|

Monopsont power |

The market power exercised in a market bu the buyer of a good or the service of a factor of production such as labour even thought the firm is not a pure monopsonist |

|

|

Occupational immobility of labour |

When workers are unwilling or unable to move from one type of jobs to another eg other skill are needed |