Reading...

![]()

Play button

![]()

Play button

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

61 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

List the Economic issues that are of pressing concern

|

1. Productivity Growth

2. Population Aging 3. Climate Change 4. Global Financial Stability 5. Rising Government Debt 6. Globalization Many of the challenges we face in Canada and around the world are primarily economic. |

|

|

|

What is Economics?

|

Economics is the study of the use of scarce resources to satisfy unlimited human wants.

|

|

|

|

What are resources?

|

A society's resources are usually divided into land, labour, and capital.Economists refer to resources as factors of production. Outputs are goods (tangibles) or services (intangibles).

|

|

|

|

Explain the concept of scarcity and choice leading to opportunity cost...

|

Resources can produce only a fraction of the goods and services desired by people.Scarcity implies the need for choice. Every choice has an associated cost—opportunity cost. Opportunity cost is defined as the benefit given up by not using resources in the best alternative way. The opportunity cost of any alternative is defined as the cost of not selecting the "next-best" alternative.

|

|

|

|

Describe the economic resources

|

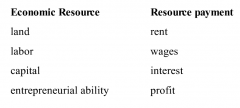

*Land-natural resources, the “free gifts of nature”

*Labor-the contribution(skills and knowledge) of human beings(Human capital) *Capital-plant and equipment(machines used in producing goods and services) this differs from “financial capital”(or money) *Entrepreneurial ability: An entrepreneur (i)Implements new ideas (ii)Brings(organizes) all the other resources together (iii)makes the basic decisions, and (iv)takes the risks to earn profits (or suffer losses) |

|

|

|

Explain trade offs

|

The existence of opportunity cost involve trade-offs in the use of resources and the choices we make in the production of goods and services. We have to decide what we will have and what we must forego(sacrifice). Economists call these sacrifices (or trade-off) as opportunity costs, which also means `there is no free lunch`

|

|

|

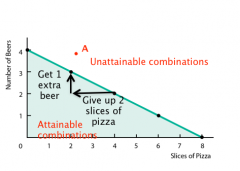

Describe this diagram...

|

All points that lie on or

inside the line would be attainable combinations.

The negatively sloped line provides a boundary between attainable and unattainable combinations. The opportunity cost of getting 1 extra slice of pizza is half of a beer that must be given up. |

|

|

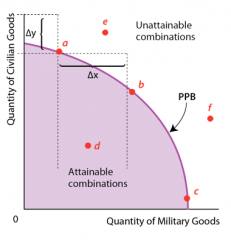

A Production Possibilities Boundary (PPF)

|

The PPF illustrates:

1. scarcity 2. choice 3. opportunity cost Points e and f show scarcity; they are unattainable with current resources. Points a, b, c, d show choice. They are all attainable, but which one will be chosen? The negative slope illustrates opportunity cost. |

|

|

|

Production possibilities curve Assumptions..

|

1. A fixed quantity and quality of available resources

2. A fixed level of technology 3. Efficient production (i.e., no unemployment and no underemployment) |

|

|

|

The Production possibility curve/frontier shows

|

The Production possibility curve/frontier shows the maximum quantity of one good that can be produced given the quantity of the other good produced, with the full employment of the available resources(land, labour, capital and entrepreneurial supply and fixed technology).

|

|

|

|

the Law of Increasing Costs...

|

The Production Possibilities Model also demonstrates the Law of Increasing Costs. As you increase production of one product , INCREASING amount of another product must be given up.

Law of diminishing returns- in a production system with fixed and variable inputs (say capital equipments and labor), beyond some point, each additional unit of variable input yields less and less additional output . This explains the bowed-out(concave) shape of the production possibilities frontier |

|

|

|

Law of diminishing returns and Increasing Marginal Cost

|

Law of diminishing returns: output will ultimately increase by progressively smaller amounts when the use of a variable input increases while other inputs are held constant. When we shift resources from one use (say x) to another use(y), the fixed capital resources required in the latter use(that is, Y) have to be substituted by variable resources in the short run

|

|

|

Four Key Economic Problems

|

1. What Is Produced? How should it be produced?

2.What is t consumer, For whom-Who will get the goods 3. Why Are Resources Sometimes Idle? 4. Is production capacity growing? |

|

|

|

Consumer sovereignty?

|

In a market system, consumers(as demanders) and producers(as suppliers) communicate through prices. Prices act as signals that guide the allocation of resources in a market economy.

|

|

|

|

How should you go about producing goods in a market economy?

|

1. profit maximization requires least-cost production (holding quantity and quality constant).

2. new technology is introduced only if it lowers total cost. 3. sellers of a resource have an incentive to supply the resource to its most highly valued use. |

|

|

|

How do you decide who should the goods be produced for?

|

In a market economy, both output and resource (factor) markets determine who receives which goods.

Distribution of income (wages, interest, rent, and profit) is determined in the resource market. Individuals who own more highly valued resources receive higher incomes. The allocation of goods and services is determined in the output market (given the distribution of income). |

|

|

|

How to decide what to produce?

|

Different economic system solve this problem in different ways. In a market based economies, the economy or a firm will produce that combination of goods and services which is valued the most by the people. This solution is obtained by allocating resources through using market prices as the guide.

|

|

|

|

Government intervention in the what should be produced, how it should be produced and for whom it should be produced...

|

Government influences the responses to each of the three fundamental questions. Examples:

What? -government spending -product safety and consumer protection laws How? -Factor endowments -safety regulations -minimum wage laws -environmental protection For whom? -tax structure -welfare programs |

|

|

|

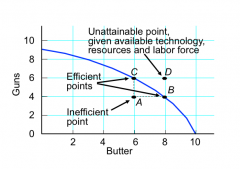

Why are resources sometimes idle?

|

An economy is operating inside its production possibilities boundary if some resources are idle.

Under what circumstances are workers seeking jobs unable to find them? Should governments worry about idle resources? Is there anything governments can do about it? |

|

|

|

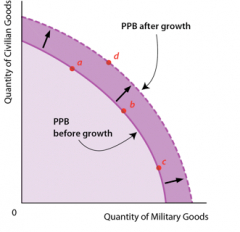

Is productive capacity growing?

|

Growth in productive capacity is shown by an outward shift of the PPB.

Point d was initially unattainable. But after sufficient growth, it becomes attainable. |

|

|

|

Define Macroeconomics

|

Macroeconomics is the study of determination of economic aggregates. E.g. GDP is an economic aggregate as it is a collaboration of all markets and individuals into a measure of total output. Focus on the price level, inflation, overall performance of the economy

|

|

|

|

Economics and Government Policy

|

The design and effectiveness of government policy is relevant to discussing all four problems.

1. It can alter the allocation of the economy's resources to make society as a whole better off. 2, It can be used to improve the distribution of consumption across individuals. 3. It is also part of the discussion of why economic resources are sometimes idle (e.g., unemployment). 4. It can affect the overall output and income. |

|

|

|

The Nature of Market Economies

|

Self-OrganizingWho or what provides the goods and services individuals desire?

Early economists noticed that the interaction of self-interested people creates a spontaneous social order—the economy is self-organizing. Self-interest, not benevolence, is the foundation of economic order. |

"It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest. ---Adam Smith

|

|

|

Self-organization is a process

|

(i)which is spontaneous: it is not directed or controlled by any agent or subsystem inside or outside of the system; and

(ii) where there is an invisible coordination mechanism that creates order (equilibrium) in the system. In economics, a market economy is sometimes said to be self-organizing. |

|

|

|

The invisible hand...

|

In economics, the invisible hand of the market is a metaphor conceived by Adam Smith to describe the self-regulating behavior of the marketplace.

n a market economy, the decisions about what goods and services to produce, how much to produce, and who gets to consume them are made by millions of firms and households. Firms and households, guided by self-interest, interact in the marketplace where prices and quantities are determined. Adam Smith made the famous observation in the Wealth of Nations in 1776 that self-interested households and firms interact in markets and generate desirable social outcomes as if guided by an "invisible hand."These optimal social outcomes were not their original intent. The prices generated by their, competitive activity signal the value of costs and benefits to producers and consumers, whose activities usually maximize the well-being of society. |

|

|

|

What is Rational self-interest?

|

A rational decision Maker only takes action if the marginal benefit exceeds the marginal cost. Individuals select the choices that make them happiest, given the information available at the time of a decision.

|

|

|

|

Self-interest vs. selfishness..

|

self interest is different from selfishness. Selfishness is acting in your benefit without regard, and often harming, other individuals. Self-interest, on the other hand, is linked to fulfilling one’s own goals, which may also include philanthropic goals or altruistic (unselfish concern for others) attitude.

|

|

|

|

Types of goods...

|

Economic goods( scarcity), meaning the price of the good is at a 0 price as many people want it. Free goods is when the quantity supplied exceeds the demand of the good when the price is 0. Economic bads are goods that people are willing to pay to avoid like illnesses, pollution etc.

|

|

|

|

Labour is

|

the contribution of human beings to the production process

|

|

|

|

Capital

|

Defined to consist as plants and equipment, when economists refer to the term capital we are talking about the physical (capital) things used to produce outputs. This defers from financial capital as we do not use bonds or stocks to build houses, we use wood (physical capital)

|

|

|

|

Entrepreneurial Ability is a type of

|

labour resource ,

entrepreneurs receive a residual payment-whatever is left over after all costs have been taken care of to produce goods. |

|

|

|

Examples of Economic resources and resource payments

|

|

|

|

|

Positive Economics

|

Positive economics is an attempt to describe how the economy functions/works and relies on testable hypothesis (educated guess)

|

|

|

|

Normative economics

|

Normative economics relies on values judgements to evaluate a term or policy, you are describing how you believe the economy should be functioning (perception)

|

|

|

|

Scientific method...

|

1. Observe a phenomena you'd like to explain

2. Come up with simplified assumptions that you use to formulate a hypothesis (a tentative explanation about this relation that you would like to observe) 3. generate predictions 4. test the hypothesis You can reject the hypothesis or fail to reject the hypothesis, they are only tentative explanations of a situation- if it is not rejected you should test it to see how well it upholds the situations |

|

|

|

ceteris paribus

|

holding everything else constant

|

|

|

|

abstraction in economics

|

when you gage in abstraction you are trying to take a complex economy and simplify it in the most fundamental way that you understand , relatively simple

|

|

|

|

Fallacies of composition

|

the fallacy of composition, this occurs when we incorrectly assume that what is true for each and every individual in isolation is true for an entire group. e.g, if individuals save more the wealth of the population will increase

|

|

|

|

post hoc, ergo propter hoc fallacy (association of causation)

|

occurs when one incorrectly assumes that one event is the cause of another because it precedes the other.

|

|

|

|

Micro economics

|

is defined to be the study of individual economic agents and individual markets- individual consumers, individual firms and the behaviour of individual markets. Focuses on the pieces of the economy and the behaviour of the individual behaviour and individual firms. Focus of the price of individual commodities

|

|

|

|

Direct relationship

|

the relationship of two variables where the increase of one variable leads to the increase of the other variable. the graph of this relationship will b upward sloping as when x increases y increases

|

|

|

|

Inverse relationships

|

When x increases y decreases, this will have a downward slope

|

|

|

|

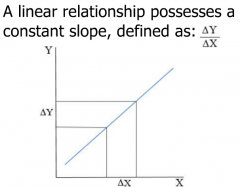

Linear relationships

|

Have a constant slope, which is defined by the change in y to the change in x.... delta y/delta x

|

|

|

|

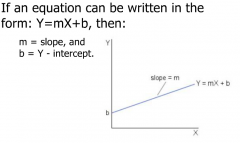

y=Mx+B

|

you can calculate the slope by saying

y=Mx+B M and B are constants, M is the slope of the relationship and B is the Y intercept. If we have a direct relationship m will be positive, if we have a inverse relationship m will be negative |

|

|

|

efficiency

|

The term efficiency

refers to organizing available resources to produce the goods and services that people most value, when they most want them, and using the fewest possible resources to do so. An economic system is said to be more efficient than another (in relative terms) if it can provide more goods and services for society without using more resources. |

|

|

|

Incentives and Self-Interest

|

Self-interest guides individuals.

Individuals respond to incentives. Prices and quantities are set in (relatively) free markets in which individuals trade voluntarily. Institutions, created by the state, protect private property and enforce contractual obligations. |

|

|

|

The Decision Makers and Their Choices

|

Three broad groups of decision makers:

1. Consumers 2. Producers 3. Government In order to achieve their objectives, maximizing consumers and producers make marginal decisions. they decide whether they will be made better off by buying or selling a little less of any given product. |

|

|

|

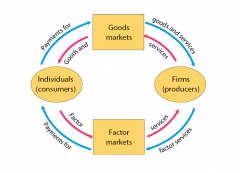

The Circular Flow of Income and Expenditure

|

|

|

|

|

The Flow of Income and Expenditure

|

Individuals own factors of production. They sell the services of

these factors to producers in factor markets and receive payment

in return.

These are the (factor) incomes of individuals. Producers transform factor services into goods and services, which they then sell to individuals in goods markets, receiving payment in return. These are the incomes of producers. |

|

|

|

The Complexity of Production

|

Production usually displays two characteristics noted long ago by Adam Smith: specialization and the division of labour. Division of labour extends the idea of specialization for the production of a single good or service.

Rather than being self-sufficient, people can specialize in producing one good or service and exchange it for another |

|

|

|

Define specialization

|

Specialization is the allocation of different jobs to different people. It is more efficient than self-sufficiency because you have a comparative advantage and you learn by doing.

Specialization must be accompanied by trade. Money eliminates the cumbersome system of barter by separating the transactions involved in the exchange of products, thereby facilitating specialization and trade. |

|

|

|

You have a comparative advantage when...

|

Individual abilities differ

|

|

|

|

learning by doing means

|

Focusing on one activity leads to improvements

|

|

|

|

Free trade?

|

If each country specializes in the production of those goods in which it possesses a comparative advantage and trades with other countries, global output and consumption in increased.

|

|

|

|

Globalization

|

Underlying modern globalization is the rapid reduction of transportation and communication costs in the last half of

the 20th century.

Today, no country can take an isolationist economic stance and hope to take part in the global economy. |

|

|

|

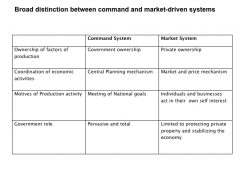

Types of Economic Systems

|

There are three pure types of economic systems:

1. Traditional 2. Command 3. Free-Market In practice, every economy is a mixed economy, in the sense that it combines significant elements of all three systems. |

|

|

|

The Great debate says..

|

A century after Adam Smith, Karl Marx (1818–1883) argued that

free-market economies could not be relied upon to generate a

"just" distribution of output.

He argued the benefits of a centrally planned system. Beginning with the Soviet Union in the 1920s, many countries inspired by Marx adopted socialist/communist systems. By the last few decades of the 20th century, most of these countries were unable to provide their citizens the rising living standards that existed in the more free-market economies. In the last two decades of the 20th century, most governments replaced their systems of central planning with much freer markets. |

|

|

|

The Failure of Central Planning

|

The failure of the centrally planned economies does not demonstrate the superiority of completely free-market economies.

Instead, it shows the superiority of mixed economies, with large elements of free markets. |

|

|

|

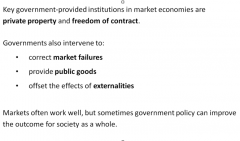

Government in the Modern Mixed Economy

|

|

|

|

|

Markets are crucial as devices for organizing complex and interdependent economies.

-Scarcity of resources, consumers’ choices, and opportunity cost are fundamental concepts of economics -The importance of marginal decisions, and Opportunity cost principle -The modern economy/economic system functions on the principal of production specialization, market exchange mechanism, and global spread of economic activities -All actual economies are mixtures(mixed economies), containing elements of all three pure systems- traditional, command, and free-market systems. |

Important Terms: Market system is a Self organizing system, Efficiency, Opportunity cost, Marginal decisions, specialization

|

|

|

|

Main characteristics of market economies

|

1. self interested

2. Incentives 3. Market price and competition 4. Institution and Govts intervention |

|