![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

215 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

Explain how accounting makes it possible to use scarce resources more efficiently. |

Accounting provides reliable, relevant, and timely information to managers, investors and creditors so that resources are allocated to the most efficient enterprises. |

Resources, efficient, timely |

|

|

Who are stakeholders in financial reporting? |

Investors, creditors, management, securities commissions, stock exchanges, analysts, credit rating agencies, auditors and standard setters |

|

|

|

What is the objective of financial reporting? |

To communicate information that is useful to key decision makers such as investors and creditors in making resource allocation decisions about the resources and claims to resources of an entity and how these are changing |

Communication, resources |

|

|

How do information asymmetry and bias interfere with the objective of financial reporting? |

Information asymmetry exists because of management bias whereby management acts in its own self-interest such as maximizing bonuses (moral hazard). Information asymmetry causes markets to be less efficient and may cause stock prices to be discounted or costs of capital to increase and may restrict good companies from raising capital in the particular market where relevant information is not available (adverse selection) |

Management, bonuses, markets, capital |

|

|

What is the need for accounting standards? |

Without standards, each enterprise would have to develop their own standards and readers of financial statements would have to become familiar with every company's particular accounting and reporting practices. |

|

|

|

What is the meaning of GAAP and the significance of professional judgement in applying GAAP? |

GAAP are either principles that have substantial authoritative support, such as the CPA Canada handbook or those arrived at through the use of professional judgement and conceptual framework. Professional judgement plays an important role in ASPE and IFRS since much of GAAP is based on general principles that need to be interpreted. |

|

|

|

What are some of the challenges in accounting? |

Oversight in the capital markets, centrality of ethics, standard setting in a political environment, principles vs rules based standard setting, the impact of technology and integrated reporting |

|

|

|

What are the main components of a conceptual framework for financial reporting? |

1st level: the objective of financial reporting 2nd level: qualitative characteristics of useful information and the elements of financial statements 3rd level: foundational principles and conventions |

|

|

|

What is the usefulness of a conceptual framework? |

-create standards that build on an established body of concepts and objectives -provide a framework for solving new and emerging practical problems -increase financial statement users' understanding of and confidence in financial reporting -enhance comparability among different companies' financial statements |

4 points |

|

|

Identify the qualitative characteristics of accounting information |

Fundamental characteristics: relevance and faithful representation Enhancing characteristics: comparability, verifiability, timeliness, understandability |

|

|

|

Basic elements of financial statements |

Assets Liabilities Equity Revenue Expenses Gains Losses |

|

|

|

Describe the foundational principles of accounting |

Economic entity Control Revenue recognition/realization Matching Periodicity Monetary unit Going concern Fair value Historical cost Full disclosure principle |

10 items |

|

|

Double entry accounting rules |

Debit side increases: assets, expenses, dividends Credit side increases: liabilities, revenues, shareholders equity, common stock, retained earnings |

|

|

|

Steps in the accounting cycle |

1. Identification and measurement of transactions and other events 2. Journalizing 3. Posting 4. Unadjusted trial balance 5. Adjustments 6. Adjusted trial balance 7. Statement preparation 8. Closing |

8 items |

|

|

How does the type of ownership structure affect the financial statements? |

The types of accounts that are in the equity section differ Corporation: under shareholders equity - share capital (preferred and common shares), retained earnings, contributed surplus, accumulated other comprehensive income Proprietor or partnership: under owners equity - owners capital, owners drawings |

|

|

|

What happens during the closing process? |

Revenue and expenses are closed to Income Summary Net income/loss in Income Summary transferred to Retained Earnings Any items posted to OCI closed to AOCI Dividends closed to retained earnings |

|

|

|

Use IFRS 13 to measure fair value |

The following must be considered : -attributes of the asset being measured -how would or could it be used -the marketplace -valuation technique/model (market model or income model) -is it an observable market or not? -level 1 (reflects market prices) - level 3 (unobservable inputs) -select the model that provides best quality fair value measure -section draws on professional judgement, an evaluation of the assets characteristics and the available information |

|

|

|

Identify differences between IFRS and ASPE |

-main difference is that IFRS contains specific guidance in IFRS 13 regarding fair value measurements -Under ASPE, guidance is spread throughout the body of knowledge and less detailed |

|

|

|

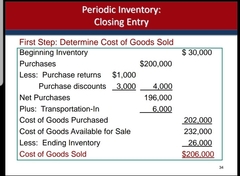

Closing entries for periodic inventory system |

|

|

|

|

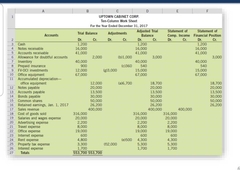

Using a worksheet |

|

|

|

|

What are the three activities in the basic business model? |

Financing Investing Operating |

|

|

|

Limitations of Income Statement |

-Items are excluded if cannot be measured reliably -Amounts reported are affected by accounting method used -Use of estimates in measuring income -Financial reporting bias -GAAP shortcomings |

|

|

|

Use of Income Statement |

Helps users: -evaluate past performance and profitability -provide a basis for predicting future performance -help assess the risk of not achieving future net cash inflows |

|

|

|

Quality of Earnings |

Refers to how solid earnings numbers are, main aspects being content and presentation -Earnings management decreases quality of earnings |

|

|

|

Comprehensive Income |

includes any non-shareholder transactionsthat causes a change in equity ex. unrealized gains/losses on revaluation of property, plant, andequipment under the revaluation model Comprehensive income = net income +/- OCI Only under IFRS |

|

|

|

Discontinued operations |

-Components that have been disposed of or held for sale -component generates its own cash flows and has its own distinct operations |

|

|

|

Held for sale |

Component is held for sale if the following criteria are met: -plan to sell exists -asset available for immediate sale -active search for a buyer -sale probable within a year -asset reasonably priced and marketed -changes to plan are unlikely |

|

|

|

Discontinued operations measurement and presentation |

-depreciation not recognized for held for sale assets -remeasured at lower of carrying amount and net realizable value -once asset is written down, subsequent gains can be recognized only up to the amount of original loss -presented separately on balance sheet -under aspe, held for sale assets maintain original classification (current/non-current) -under ifrs, held for sale assets generally current assets |

|

|

|

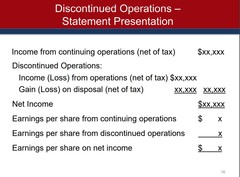

Discontinued operations statement presentation |

|

|

|

|

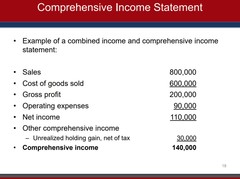

Presentation of Combined Comprehensive and Income Statement |

|

|

|

|

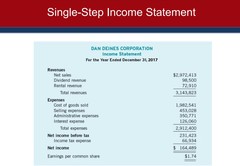

Presentation of Single-Step Income Statement |

|

|

|

|

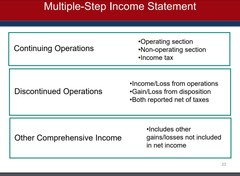

Presentation of Multiple-Step Income Statement |

|

|

|

|

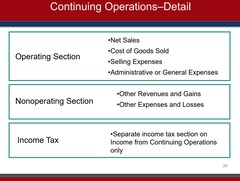

Continuing Operations Section of Income Statement |

|

|

|

|

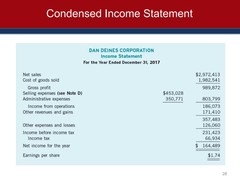

Condensed Income Statement |

|

|

|

|

Nature vs. Function (IFRS only) |

Nature of expenses: purchase of materials, transportation costs, employee benefits, depreciation etc. Function of expenses: cost of sales, administrative costs |

|

|

|

Intraperiod Tax Allocation |

-Refers to allocation of income tax within a fiscal period -certain irregular items on income statement reported net of tax -income tax expense (or benefit) is calculated and presented separately for the following: 1. income from continuing operations 2. discontinued operations 3. other comprehensive income |

|

|

|

Earnings per share (EPS) |

-indicates dollars earned per common share -eps based on earnings before discontinued operations and eps based on net income must be presented on face of income statement -eps based on discontinued operations may be disclosed in notes to financial statements |

|

|

|

EPS formula |

Net income - preferred dividends / weighted average of common shares outstanding |

|

|

|

Statement of Changes in Equity |

Under IFRS, presented in lieu of a retained earnings statement and presents the following -total comprehensive income -for each component of equity, the effects of retrospective application/restatement -reconciliation between the carrying amount of the component of equity at the beginning and end of the period |

|

|

|

Use of Statement of Financial Position and Statement of Cash Flows |

To assess: -financial flexibility and risk of business failure -earnings quality -creditworthiness |

|

|

|

Uses of Statement of Financial Position |

-evaluating capital structure -computing rates of return on invested assets assessing an enterprise's -liquidity (time until asset is realized or liability has to be paid) -solvency (ability to pay debts and related interest) -financial flexibility (able to respond to unexpected needs and opportunity) |

|

|

|

Limitations of Statement of Financial Position |

-many assets and liabilities stated at historical cost -judgement and estimates are used in determining many of the items -does not report items that cannot be recorded objectively (eg. internally generated goodwill) |

|

|

|

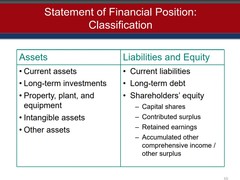

Statement of Financial Position Classification |

|

|

|

|

Working Capital |

Current assets - current liabilities |

|

|

|

Five types of additional information required on SFP |

-contingencies and provisions -contractual situations -accounting policies -additional detail -subsequent events |

|

|

|

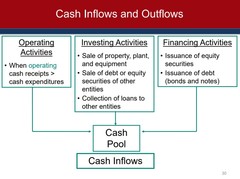

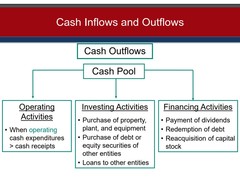

Use of Statement of Cash Flows |

To assess the firm's ability to generate cash and cash equivalents and to allow comparison of cash flows between different entities Divided into three main categories: -Operating activities -Investing activities -Financing activities |

|

|

|

Cash Inflows |

|

|

|

|

Cash Outflows |

|

|

|

|

Statement of Cash Flows presentation |

Direct method: includes specific cash inflows/outflows Indirect method: Begins with net income and reconciles to cash (adds back non-cash charges deducted from net income such as depreciation) |

|

|

|

Current cash debt coverage ratio (financial liquidity) |

net cash provided by operating activities/average current liabilities |

|

|

|

Cash debt coverage ratio (financial flexibility) |

Net cash provided by operating activities/average total liabilities |

|

|

|

Free cash flow |

Net cash from operations less capital expenditures and dividends -indicates discretionary cash flow (cash left to invest or expand) to make additional investments, to retire its debt, or to add to its liquidity |

|

|

|

Major Types of Ratios |

Liquidity Ratios: Measure the enterprise's short-term ability to pay its maturing obligations Activity Ratios: Measure how effectively the enterprise is using its assets. Also measure how liquid certain assets are such as inventory and receivables. Profitability ratios: Measure financial performance and shareholder value creation for a specific time period Solvency ratios: Measure the degree of protection for long-term creditors and investors or a company's ability to meet its long-term obligations |

|

|

|

Sales transactions |

Often involve transfer of goods, services, or both. Accounting is different under each situation Sale of goods: tangible assets with a finite point when control transfers to buyer (generally with transfer of legal title and possession) Sale of services: legal title and possession irrelevant Sale of goods and/or services combinations: complexity of measuring each component of bundled sales or multiple deliverables |

|

|

|

Description of revenue/sales and approaches to recognizing |

Revenue/sales is described as: -inflow of economic benefits (eg cash, receivables) -arising from ordinary activities two approaches to recognizing revenue/sales: -asset/liability approach (contract based approach) -earnings approach |

|

|

|

Five steps in the revenue recognition process |

1. identify the contract with customers 2. identify the separate performance obligations in the contract 3. determine the transaction price 4. allocate the transaction price to the separate performance obligations, and 5. recognize revenue when each performance obligation is satisfied |

|

|

|

Revenue recognition principle |

Recognize revenue in the accounting period when the performance obligation is satisfied |

|

|

|

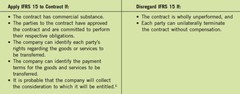

Step 1: Identifying the contract with customers |

Contract is an agreement between two parties with enforceable rights or obligations. Can be written, oral or implied. A company applies the revenue guidance according to the criteria: |

|

|

|

Step 2: Identifying Separate Performance Obligations |

Performance obligation is a promise in a contract to provide a product or service to a customer -may be explicit, implicit, or possibly based on customary business practice. Below are examples when revenue is recognized as a result of providing a distinct product or service, therefore satisfying a performance obligation: |

|

|

|

Step 3: Determining the Transaction Price |

-Transaction price is the amount of consideration a company expects to receive in exchange for transferring goods or services -Usually stated in the contract -Must consider: variable consideration, time value of money, noncash consideration, consideration paid or payable to the customer |

|

|

|

Step 4: Allocating the Transaction Price to Separate Performance Obligations |

-transaction prices are allocated to performance obligations based on their fair values -fair value is standalone selling price -if fv info not available, best estimates are used |

|

|

|

Ways to estimate the stand-alone selling price |

adjusted market assessment approach - estimate price cx will pay and look at competitor prices expected cost plus a margin - forecast expected costs and add a profit margin residual approach - use when selling price is highly variable or uncertain. estimate standalone selling price by starting with the total price for contract and deduct the observable selling prices of other items being sold |

|

|

|

Step 5: Recognizing Revenue When Each Performance Obligation is Satisfied |

-Company satisfies its performance obligation when the customer takes control of the good or service |

|

|

|

Earnings Approach |

Used by ASPE, revenues for sale of goods are recognized when following criteria are met: 1. risks and rewards of ownership have transferred to customer 2. vendor has no continuing involvement in, nor effective control over, the goods sold 3. costs and revenues can be measured reliably 4. collectibility is probable |

|

|

|

Right of return |

if there is an expectation items may be returned, an estimate must be made and accounted for the initial transaction (credit refund liability and debit estimated inventory returns, then reverse upon return) |

|

|

|

Repurchase agreements |

Will allow company to transfer an asset to a customer but have an obligation or right to repurchase the asset at a later date -generally reported as a financing transaction (borrowing) |

|

|

|

Bill and Hold Arrangements |

-A contract under which one entity bills a customer for a product but the entity retains physical possession of the product until it is transferred to the customer at a point in the future -may occur when purchasing company has limited space for the product , delays in production schedule, or more than sufficient inventory in its distribution channel |

|

|

|

Principal-agent relationships |

-Principals obligation is to provide goods or services to the customer -Agents obligation is to arrange for the principal to provide goods or services to the customer -amounts collected on behalf of the principal are not revenue of the agent as agent would record commission as their revenue most likely eg. real estate |

|

|

|

Consignment sales |

-Consignor ships inventory to consignee -Consignee sells inventory on behalf of consignor -Risks and rewards have not transferred -Goods held by seller as "Inventory on Consignment" -Not held as inventory on consignee's books -When goods are sold, consignee remits cash to consignor, after deducting commission and other chargeable expenses |

|

|

|

Warranties |

-two types of warranties: -Assurance type warranty: warranty where the product meets agreed-upon specifications at the time the product is sold. included in the sales price of the product -Service type warranty: warranty that provides additional service beyond the assurance type warranty - not included in the sales price of a product |

|

|

|

Non-refundable upfront fees |

companies sometimes receive payments upfront from customers before they deliver a product or perform a service. -generally relate to the initiation, activation or set up of a good or service to be provided or performed in the future -in most cases non-refundable |

|

|

|

Contract assets (2 types) |

1. Unconditional rights to receive consideration eg. where the company has satisfied its performance obligation with a customer or the amounts due to the company are non-refundable 2. conditional rights to receive consideration from the customer: eg. the company has not satisfied the performance obligation or has satisfied one performance obligation but must satisfy another in the contract before entitle to consideration. |

|

|

|

Contract liability |

A company's obligation to transfer goods or services to a customer for which the company has received consideration from the customer |

|

|

|

Percentage of Completion Method (long-term contracts) |

-The amount of revenues, costs and gross profit recognized on long term contracts depends upon the percentage of work done -application of this method requires a basis for measuring the progress toward completion at interim dates, and is based on significant judgement -can use input measures (eg. costs incurred, labour hours worked) -can use output measures (eg. tonnes produced) |

|

|

|

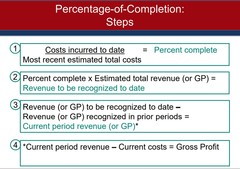

Percentage of Completion Steps (cost-to-cost method) |

|

|

|

|

Percentage of Completion Financial Statement Presentation |

-The difference between "Construction In Process" and "billings on Construction in Process" is recorded on the balance sheet as either: -current asset* (with inventories) if difference is a debit balance -current liability* if difference is a credit balance *may be non-current depending on length of contract |

|

|

|

Construction in Process vs. Billlings on Construction in Process |

Construction in Process - Balance in account represents the costs incurred and gross profit recognized to date Billings on Construction in Process - represents the billings made to customers to date |

|

|

|

Criteria for satisfying a performance obligation and recognizes revenue over time and the company is able to estimate progress toward completion (at least one must be met) |

1. The customer receives and consumes the benefit as the seller performs 2. The customer controls the asset 3. The company does not have an alternate use for the asset and has a right to payment for its performance If one of these is not met, revenue is recognized at a point in time. ASPE criteria is that revenue should reflect the work accomplished |

|

|

|

Zero-profit method |

Under IFRS, if one of the criteria is met but an estimate cannot be made, then the company records recoverable revenues equal to costs until the uncertainty is resolved |

|

|

|

Completed-contract method |

Under ASPE, revenue and gross profit are recognized when the contract is completed -all journal entries are the same as percentage of completion method except no entry is recorded at the end of the period to recognize revenue and gross profit |

|

|

|

Long-term contract losses |

-can be interim losses on a profitable contract or overall losses on an unprofitable contract Percentage of completion method: All losses are immediately recognized Completed-contract method: losses are recognized only when overall losses result |

|

|

|

Key concerns relating to management and control of cash and accounts receivable |

Cash: Implementing appropriate internal controls incl. regular bank reconciliations, minimizing idle cash Accounts receivable: Implementing appropriate internal controls including appropriate credit policies, speeding up the collection cycle |

|

|

|

Restricted cash |

-separately disclosed and reported in the current assets section or classified separately in the long-term assets section, depending on the date of availability or expected disbursement -compensating balances: minimum cash balances maintained by a corporation in support of existing borrowings -funds not available for use by corporation but bank can use restricted cash -petty cash, special payroll, and dividend accounts are examples -note disclosure of restricted cash is required |

|

|

|

Foreign currencies |

-reported in Canadian dollars -exchange rate on the date of the statement of financial position is used -if restrictions exist on foreign funds, they are reported as restricted |

|

|

|

Bank overdrafts |

-represent cheques written in excess of the cash account balance -reported as current liabilities (often as ap) -should not be offset against the Cash account -may be offset against cash in another account if both accounts are at the same bank |

|

|

|

Cash equivalents |

-short-term, highly liquid investments readily convertible to known amounts of cash and are subject to an insignificant risk in changes in value -original maturity 3 mos or less -ex. treasury bills, money market funds, commercial paper -ASPE excludes equity securities -under IFRS, some equity instruments can be classified as cash equivalents (eg. preferred shares acquired within short time of maturity date) -reported at fair value |

|

|

|

Receivables |

-loans and receivables are specific claims against customers and other parties for cash (or other assets) -classified as either current or non current (current when expected to collect within one year) -can be classified as trade or non trade receivables |

|

|

|

Trade receivables |

-accounts receivable -notes receivable |

|

|

|

Non-trade receivables |

-advances to employees or other officers -delayed payment terms from a purchaser -receivables from the government -dividends and interest receivables -amounts owing by insurance companies |

|

|

|

Measurement of accounts receivable |

Initially measured at fair value and then after initial recognition, measure at amortized cost |

|

|

|

Trade discounts |

discounts given to customers for different quantities purchased (often quoted as %) -generally not recorded, price charged net of discount recorded by seller as a receivable and a revenue |

|

|

|

Cash discounts (sales discounts) |

-encourages customers to pay faster, they are recorded -ex. 2/10, n/30, will receive a 2% discount if paid within 10 days and gross amt due in 30 days |

|

|

|

Gross method |

-records discounts when customers pay within sale period -"sales discounts" are deducted from sales on the income statement -most common method |

|

|

|

Net method |

-records accounts receivable net of the discount, discounts are forfeited by customers when they are not taken -preferred method but rarely used -"sales discounts forfeited" are recorded as other revenue if customer does not take discount |

|

|

|

Impairment of accounts receivable |

-short-term receivables reported at NRV (net amount of cash expected to be collected) -calculated as gross accts receivable less estimated uncollectable accounts and any returns, allowances or cash discounts -loans and receivables are impaired if there is "significant adverse change" in expected configuration of cash flows (timing or amount) |

|

|

|

Allowance method |

-records estimated impairment to properly value accounts receivable and record the bad debts as expense in the same accounting period as the sale -receivables are reported at their estimated NRV ie. net of allowance for doubtful accounts -uses past collection experience to estimate uncollectible accounts -focus to report ar at nrv (does not focus on matching bad debt expense to sales) -any existing balance in Allowance for Doubtful Accounts is used to calculate the current year's bad debt expense |

|

|

|

Estimate of uncollectable accounts |

may be based on: -Allowance procedure only: mgmt frequently analyzes accounts receivable, estimates uncollectable amounts and adjusts allowance for doubtful accounts -mix of procedures: initally may use percentage of sales (or net sales) but must still adjust at year end to ensure that Allowance for Doubtful Accounts is appropriate |

|

|

|

Percentage-of-receivables approach (aging method) |

The process whereby receivables are recorded on the statement of financial position at their net realizable value |

|

|

|

Writing off accounts receivable |

Allowance method: debit Allowance for Doubtful Accounts, credit Accounts Receivable -if payment received after writeoff, debit accounts receivable and credit allowance for doubtful accounts, then another entry to debit cash and credit accounts receivable direct write off method: -used if uncollectible amounts are highly immaterial -debit bad debt expense and credit accounts receivable |

|

|

|

Recognition of short-term notes receivable |

-supported by promissory note and contain some interest are either: -interest bearing: have a stated rate of interest or -non-interest bearing: interest rate not always stated, interest rate is the difference between the amount borrowed and the face amount -accounted for at amortized cost |

|

|

|

Long-term loans receivable |

-recognized at fair value (present value of future cash flows) -when stated interest rate is market interest rate, note or loan is issued at fair value -when there is a difference between interest rates, the note or loan is issued at a premium or a discount (ie. present value is greater or less than face value) |

|

|

|

Stated interest rate (face rate/coupon rate) |

The rate of interest that is part of the loan contract |

|

|

|

Effective interest rate (market rate/yield rate) |

Rate that is used in the market to determine the note's value; that is, the discount rate that is used to determine its present value |

|

|

|

Effective interest method of amortization |

Required under IFRS Requires that the effective interest or yield rate be calculated at the time whne the investment is made. This rate is then later used to calculate interest income by applying it to the carrying amount (book value) of the investment for each interest period. The note's carrying amount changes as it is increased by the amount of discount amortized. |

|

|

|

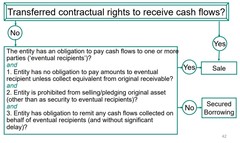

Derecognition of receivable |

-holder of accounts or notes receivable can transfer them to another company for cash transfer may be a secured borrowing or a sale of receivables -when determining whether an asset should be derecognized, ASPE considers who has control of the asset whereas IFRS considers whether the risks and rewards have been transferred. |

|

|

|

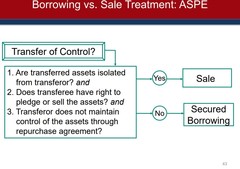

Borrowing vs. Sale (IFRS) |

|

|

|

|

Borrowing vs. Sale (ASPE) |

|

|

|

|

Accounting for transfers of receivables (ASPE) |

|

|

|

|

Secured Borrowing |

-Account for receivable (now collateralized) same way as before secured borrowing: -collect accounts receivable, record sales returns and discounts, absorb bad debts expense -Account for new liability (eg. note payable) -record a finance charge (if applicable), record interest expense on note payable, pay the note periodically from collections |

|

|

|

Sale of receivables (eg factoring) |

-ownership of receivables transferred to the purchaser (the factor); receivables recorded as an asset in the purchaser's books -if sold without recourse, purchaser is fully responsible for the collection of the receivables -seller records any retained proceeds as "due from factor" (a receivable) which covers possible sales discounts and sales returns and allowances -seller records a gain or loss on the sale of receivables (normally a loss, representing the finance charge) -seller records any recourse liability (if receivables are sold with recourse i.e. sellers guarantee to pay the purchaser if customer fails to pay) |

|

|

|

Presentation of trade accounts and notes receivable |

• Segregate types of receivables (i.e. ordinary tradeaccounts, due from related parties and otherreceivables segregated) • Separate current from non-current receivables • If > 1 year, report amount and maturity date • Use allowance account to record impairments (IFRSalso requires reconciliation of changes in theallowance account during accounting period) • Income statement disclosure of interest income,impairment losses, and any reversals of such losses |

|

|

|

Accounts receivable turnover ratio |

Net sales or revenue/average trade receivables (net) |

|

|

|

Days sales uncollected ratio |

365 days/accounts receivable turnover |

|

|

|

How petty cash system works |

-Someone is designated as petty cash custodian and given small amount of cash -custodian gets a receipt for each authorized disbursement -when fund runs low, custodian presents to controller a request for disbursement supported by receipts and other evidence -cheque is prepared and transactions recorded by someone other than custodian |

|

|

|

Cash over and short |

Account used when the cash in the petty cash fund plus the dollar amount of the receipts does not add up to the imprest petty cash amount |

|

|

|

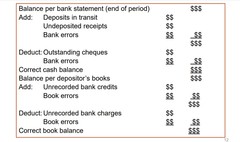

Bank reconciliation form |

|

|

|

|

Inventory |

Current asset Merchandising company: 1 inventory acct, Merchandise Inventory. Cost of inventory sold transferred to COGS Manufacturing company: 3 inventory accts: Raw materials inventory, work in process inventory, finished goods inventory. COGManufactured similarly used like COGS |

|

|

|

Items to be included in inventory |

Legal title generally determines items to be included 1. Goods in transit if seller has title during transit (fob destination) 2. goods out on consignment 3. goods sold under buyback agreements 4. goods sold with high rates of return that can't be estimated |

|

|

|

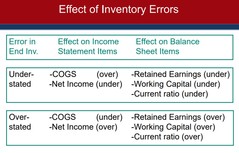

Effect of inventory errors |

|

|

|

|

Costs included in inventory |

Includes all costs of purchase, costs of conversion, and other costs incurred in bringing the inventories to their present location and condition Product cost: invoice, freight, etc Conversion cost: direct labour, fixed and variable overhead Not included: Period costs (selling, admin) |

|

|

|

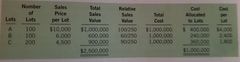

Basket purchase |

When a group of units with different characteristics is purchased at a single lump-sum price |

|

|

|

Relative sales value method |

Method to allocate total cost of basket purchase among the various units based on their relative sales value |

|

|

|

Interest and borrowing costs included in inventory |

Under IFRS: Interest costs are included as product costs if manufacturing of inventory takes a long time (otherwise company can choose whether to capitalize or not) Under ASPE: interest costs may be either expensed or capitalized, but policy must be disclosed |

|

|

|

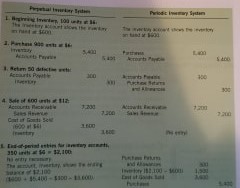

Perpetual inventory vs periodic inventory entries |

|

|

|

|

Specific identification |

Each item sold and purchase is individually identified |

|

|

|

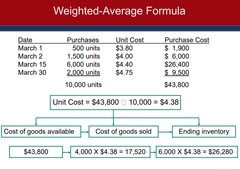

Weighted average cost formula (periodic) |

|

|

|

|

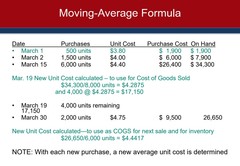

Moving average cost formula (weighted average used with perpetual system) |

|

|

|

|

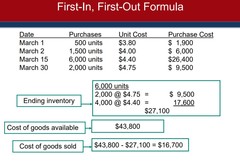

FIFO |

|

|

|

|

Choice of cost formula |

-choose an approach that corresponds as closely as possible to the physical flow of goods -report an inventory cost on the statement of financial position that is representative of the inventory's recent cost -use the same method for all inventory assets that have similar economic characteristics for the entity |

|

|

|

Lower of cost and net-realizable value to value inventory |

Cost is not appropriate if the asset's value (ability to generate net cash flows) is now less than its carrying amount. This is because readers of financial statements presume that current assets can be converted into at least as much cash as the amount reported on the sfp. Second, a loss of utility should be deducted from (matched with) revenues in the period in which the loss occurs, not the period where the inventory is sold. |

|

|

|

Direct method |

Records the NRV of the inventory directly in the inventory account at the reporting date if the amount is lower than cost. No loss is reported separately in the income statement because the loss is buried in cost of goods sold |

|

|

|

Indirect method (allowance method) |

Keeps the inventory account at cost and establishes a separate contra asset account to inventory on the SFP. (Allowance to reduce inventory to NRV), a loss account is reported on income statement -recovery of market value decline is recorded up to but not exceeding original cost |

|

|

|

Exceptions to LC&NRV model |

-Inventories measured at NRV if: sale is assured, or there is an active market and minimal risk of completing the sale, and costs of disposal can be estimated Inventories measured at fair value less costs to sell include: inventories of commodity broker-traders -biological assets and agricultural produce at point of harvest (no specific ASPE guidance on measurement of these assets) |

|

|

|

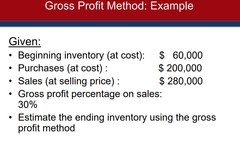

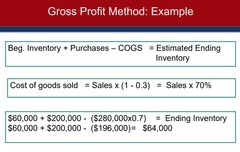

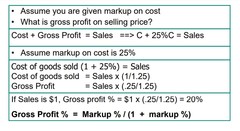

Gross profit method of estimating inventory |

-may be required in situations such as interim reporting, fire loss, testing reasonableness of cost from actual inventory count based on 3 assumptions: 1. beginning inventory + purchases = cost of goods available for sale 2. goods not incl. in cogs must be on hand in ending inventory 3. when an estimate of cogs is deducted from the cogsafs, the result is an estimate of ending inventory |

|

|

|

Example of gross profit method of estimating inventory pt. 1 |

|

|

|

|

Example of gross profit method of estimating inventory pt. 2 |

|

|

|

|

Example of gross profit method of estimating inventory pt. 3 |

|

|

|

|

Disclosure and presentation of inventory |

examples of required disclosures: 1. measurement policy 2. total inventory, as well as inventory by classification 3. amount of inventory recognized as expense on the income statement (usually reported as COGS) 4. any amount of inventory pledged as security for liabilities |

|

|

|

Inventory ratios |

Inventory turnover: cogs/average inventory average days to sell inventory 365/inventory turnover |

|

|

|

Types of investments |

Debt investments: include investments in government debt, corporate bonds, convertible debt, commercial paper equity investments: ownership interests in companies (preferred stock, common stock) motivations for investments include: to obtain short or long term returns on investments and for corporate strategy |

|

|

|

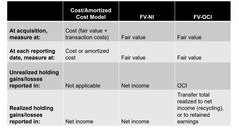

Three main models of accounting for investments |

|

|

|

|

Cost/amortized cost model |

Investments in shares: 1. recognize investment at fair value plus direct transaction costs 2. report at cost (unless impaired) 3. recognize dividend income when have claim to dividend 4. when dispose of investment, recognize gain or loss on disposal in net income Investments in debt securities: 1. recognize at fair value plus direct transaction costs 2. report at amortized cost as well as interest receivable (unless impaired) 3. recognize interest income as earned, and also amortize any discount/premium by adjusting carrying amount of investment 4. when disposing of investment, first bring accrued interest and discount/premium amortization up to date. derecognize investment and report a gain or loss on disposal in net income. |

|

|

|

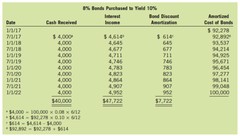

Bond discount amortization example |

|

|

|

|

Sale of investments |

-discount or premium is amortized from last date of amortization to date of sale -new carrying amount calculated, amortized cost balance + discount (- premium) amortized from last date of amortization -gain or loss calculated as difference between selling price and carrying amount -any accrued interest income is calculated and received over and above the investment selling price |

|

|

|

FV-NI (also known as FVTPL) model |

-investment recorded at fair value at acquisition -transaction costs are expensed -adjusted to fair value at each reporting date and any holding gain or loss is reported in net income -any interest/dividend income and any holding gain or loss on the investment may be reported together as "Investment Income" (interest must be reported separately under ASPE) |

|

|

|

FV-OCI |

-at acquisition, investments recorded at fair value -transaction costs tend to be added to asset's carrying amount -at each reporting date, fv-oci investments are adjusted to fair value and any holding gain or loss is reported in OCI -accumulated holding gains/losses are reported in AOCI, which is a separate item under shareholders' equity -when investments are disposed, previously unrealized holding gains or losses need to be transferred out of OCI/AOCI -under FV-OCI with recycling, unrealized holding gains or losses are "recycled" (transferred) into net income (and as part of net income, closed to retained earnings) -under FV-OCI without recycling, unrealized holding gains or losses are transferred directly into retained earnings (bypassing net income) |

|

|

|

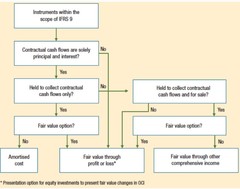

Classfication of investments under IFRS 9 |

|

|

|

|

Impairment models for investments |

-must be reviewed for impairment to ensure that future benefit justifies the valuation on the balance sheet three different impairment models: -incurred loss model -expected loss model -full fair value model |

|

|

|

Incurred Loss Model |

-impairment test carried out only if there is evidence of possible impairment indicators of impairment may include: -significant financial difficulties -defaulting on principal/interest payments -major financial reorganization or bankruptcy -impairment loss recognized in net income as difference between carrying amount and revised present value of expected cash flows -Revised present value is calculated using discounted cash flow(DCF) model (using either historic or current market rate asdiscount rate) |

|

|

|

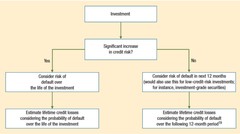

Expected Loss Model |

-Impairment tests are made on a continuous basis and do not require a triggering event to occur -impairment loss recognized in net income as difference between carrying amount and revised present value of expected cash flows -revised present value is calculated using discounted cash flow model (using effective interest rate from time of acquisition) |

|

|

|

Decision tree of the Expected Loss Model for impairment |

|

|

|

|

Fair value loss model |

-impairment loss is recognized in net income as difference between carrying amount and fair value -where fair value is determined using the discounted cash flow model, use the current interest rate at time of impairment |

|

|

|

Accounting standards for impairment (IFRS) |

-for all financial asset investments accounted for at cost/amortized cost: expected loss model (with original discount rate) -for FV-NI instruments and equity investments accounted for using FV-OCI: full fair value model (no need to do separate impairment test) |

|

|

|

Accounting standards for impairment (ASPE) |

-for financial asset investments accounted for at cost/amortized cost: incurred loss model (using current market rate) -for equity instruments (with market values) and derivative instruments, use fair value model |

|

|

|

Strategic investments |

-as common shares carry voting rights, extent of influence becomes a factor in determining the appropriate accounting treatment -3 levels of influence, each with its own accounting treatment: 1. little or no influence (< 20%) 2. significant influence (20-50%) 3. control (> 50%) |

|

|

|

Investment in Associates: Significant influence |

-appllies to equity investments of significant influence (not control) -significant influence deemed using the following criteria: 1. quantitative test: 20%-50% ownership 2. qualitative test: -representation on board of directors -participation in policy making -material intercompany transactions -exchange of management personnel -provision of technical information -under IFRS, accounted for using the equity method -under ASPE, investors can choose either equity method or cost method (unless associate shares are quoted in active market, in which case FV-NI model used) |

|

|

|

Equity method |

-investment recorded at cost of acquisition -investor takes into income its respective share of the investee net income for the year by debiting the Investment account and crediting Investment Income -any dividends received are credited to the Investment account -the accrual basis of accounting is applied -amounts paid in excess of (or less than) investee's book value becomes part of the cost of the investment -these amounts must be accounted for appropriately after the acquisition -for example, if the difference is due to long-lived assets with fair values greater than book value, the difference must be amortized -share of discontinued operations and other comprehensive income of investee are reported in the same way by the investor (major classifications of income are retained) |

|

|

|

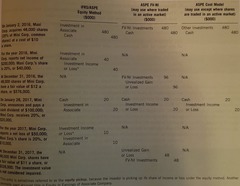

Equity method example |

|

|

|

|

Equity method impairment |

-investments with significant influence are assessed at the end of each reporting period to determine if there are indicators of impairment -if there are indicators of impairment, the impairment test is carried out -impairment loss is recognized in income and is measured as carrying amount in excess of investment's recoverable amount -investment's recoverable amount is measured as the higher of value in use and fair value less costs to sell -impairment losses may be reversed |

|

|

|

Equity method disposal |

-on disposal of the investment, both investment account and investment income accounts are brought up to date (adjusted for investor's share of associate's income and changes in book value up to date of sale) -investment's carrying value is removed and any gains/losses are recognized in net income |

|

|

|

Investments in Subsidiaries |

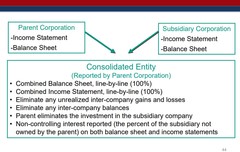

-when one corporation (the parent) acquires control of another entity (subsidiary) -control is assumed when investor owns 50% or more of voting shares of other company -control defined as continuing power to determine the strategic operating, financing, and investing policies of another entity without the co-operation of others (ASPE) -investor controls another if it has the power to direct the activities of the other entity to generate returns, either positive or negative, for the investor (IFRS) -under IFRS, investor with subsidiaries is required to present consolidated financial statements for the group of companies under its control (eliminates the investment account and instead reports all assets and liabilities of the subsidiary on a line by line basis) -under ASPE, parent company has the option to: -consolidate all its subsidiaries, or -present all of its subsidiaries under either the equity method or cost model (same choice must be applied to all subsidiaries) |

|

|

|

Consolidated Financial Statements |

|

|

|

|

PP&E Asset Components |

components of a single asset should be recognized separately if they make up a relatively significant portion of the asset's total cost |

|

|

|

Borrowing costs PP&E |

Under IFRS, borrowing costs that are incurred during acquisition, construction, or production of qualifying assets must be capitalized as part of the asset's cost ASPE allows a choice of capitalizing or expensing |

|

|

|

Cash discounts PP&E |

-net of discount method is preferred method, where asset cost is reduced by the discount even if the discount is not taken and is considered the asset's cost -other approach is that discount should not always be deducted |

|

|

|

Deferred payment contracts |

• Assets, purchased through long-term credit,are recorded at the present value of theconsideration exchanged • When no interest rate is stated, the cash priceof the purchased asset is used to determineimputed interest rate • Interest expense is recognized over the termof the deferred payment contract |

|

|

|

Share based payments |

When property is acquired by issuing shares, the fairvalue of the asset received or the fair value of theshares given up is used for the cost of the asset • If the fair value of the asset received cannot be readilydetermined, and the shares given up are activelytraded, the market value of publicly traded shares isused |

|

|

|

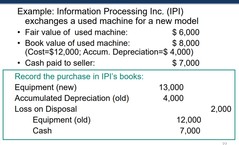

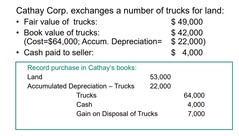

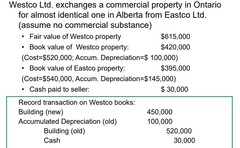

Asset exchange |

• Monetary exchange of assets occurs when:– Non-monetary assets (e.g., PP&E) are acquired for cashor other monetary assets (e.g., accounts and notesreceivable), or– Non-monetary assets are disposed of in exchange formonetary assets • Non-monetary transaction or exchange of assetsoccurs when:– Non-monetary asset is exchanged for another nonmonetary asset |

|

|

|

Nonmonetary transactions |

• The basic ASPE standard is that the nonmonetary exchange is valued at:– the fair value of the asset given up, or– the fair value of the asset received whichever ismore reliably measurable, and– gain or loss on the exchange is recognized inincome • Monetary transactions are accounted for onthe same basis Exception to standard: • If one or more of the following conditionsexist:1. transaction lacks commercial substance, 2. fair values are not determinable, •Then:– new asset cost equals book value of assetsgiven up, and– no gain is recognized (but losses arerecognized) |

|

|

|

Asset exchange example 1 |

|

|

|

|

Asset exchange example 2 |

|

|

|

|

Asset exchange example 3 |

|

|

|

|

Contributed assets and government grants (non-reciprocal transfers) |

Referred to as non-reciprocal transfers: transfer of assets wherenothing is given up in exchange (e.g., donations, gift, governmentgrants) • Asset’s fair market value used as cost of asset • Two approaches:1. Capital Approach: credit Donated Capital; used forshareholder contributions only; otherwise not GAAP 2. Income Approach: credit represents income; used for nonowner contributions;• Cost Reduction Method: credit the respective assetaccount (benefit recognized through reduced depreciationexpense)• Deferral Method: credit Deferred Revenue (benefitamortized into revenue) |

|

|

|

Land costs |

• Land costs include:1.Purchase price 2.Closing costs (title, legal, and recording fees) 3.Costs of getting land ready for use (such as removalof old building, clearing, grading, filling and draining)4.Assumption of liens or encumbrances 5.Additional improvements with an indefinite life • Sale of salvaged materials reduces cost of land • Special assessments for local improvements (e.g.,pavement) are part of land cost Permanent improvements to the land such aslandscaping are added to the Land account• Improvements with limited lives (such asdriveways, walkways, fences, and parkinglots) are recorded in a separate LandImprovements account • These costs are separated from Land as theyare depreciated over their estimated usefullives |

|

|

|

Building costs |

• Building costs include all costs directlyrelated to buying or constructing the building • The removal of an old building previouslyowned and used increases loss on thedisposal of the old building • If land is purchased with an old building on it,any demolition costs less salvage value ischarged to Land |

|

|

|

Leasehold Improvements |

• In long-term lease contracts, the lessee maypay for improvements on the leased property • Examples: construction of building on leasedland, improvements to leased building • These costs are recorded in a separateaccount called Leasehold Improvements • Leasehold improvements are depreciatedover the lesser of the remaining lease life andthe useful life |

|

|

|

Equipment costs |

• Includes delivery equipment, office equipment, factoryequipment, machinery, and furniture • Cost of equipment includes all necessary and reasonablecosts incurred to get asset ready for its intended use • Includes:– Purchase price– Freight and handling charges– Insurance while in transit– Costs of special foundation, assembly and installation– Cost of trial runs |

|

|

|

Investment property |

• Property that is held to generate rentalrevenue and/or appreciate in value, ratherthan– sell as part of ordinary business or– use in production, administration, or supplying ofgoods and services • IFRS allows for special accounting under IAS40 subsequent to acquisition |

|

|

|

Natural Resource Properties |

Also known as wasting assets• Examples: oil and gas resources, and mineral deposits • Main characteristics:1. Asset is completely removed or consumed2. Asset does not retain original characteristics • Costs to be capitalized relate to four activities:1. Acquisition of properties2. Exploration3. Development4. Restoration • Capitalized costs make up the depletion base, and aredepreciated through depletion charge into inventory |

|

|

|

Biological assets |

Examples: fruit trees, grapevines, livestock • Special standard under IFRS– Measure at fair value less costs to sell, withchanges in values going through incomestatement |

|

|

|

Measurement after Acquisition |

There are three main measurement methods toaccount for property, plant, and equipmentsubsequent to acquisition: 1. Cost Model (CM) 2. Revaluation Model (RM) 3. Fair Value Model (FVM) • Under ASPE, CM must be used • Under IFRS, companies have the followingchoices: – For investment property assets: CM or FVM – For other PP&E assets: CM or RM |

|

|

|

Cost Model |

Measures property, plant and equipment assets after acquisition at their cost less accumulated depreciation and any accumulated impairment losses |

|

|

|

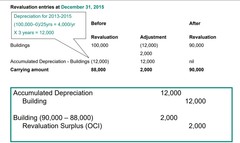

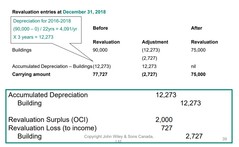

Revaluation Model |

PP&E assets carried at – fair value at the date of revaluation, less – any subsequent accumulated depreciation andimpairment losses • Available only for PP&E assets whose fairvalue can be measured reliably • Revaluation must be frequent enough sothat carrying value is not materially differentfrom assets’ fair value (not necessarilyevery year) When carrying value of asset increases (debit) – Credit Revaluation Surplus (equity, OCI), unless increasereverses previous declines recognized in income (in this case,recognize increase in income to extent of prior declines) • When carrying value of asset decreases (credit) – Debit Revaluation Surplus (equity, OCI) to the extent theaccount has credit balance for the asset. Otherwise, debit isrecognized as decrease in income. • There can be no net increase in net income from revaluing theasset over its life • Revaluation Surplus is transferred directly to Retained Earnings(either each period, or only at time of disposal) |

|

|

|

Revaluation Model Example pt 1 |

|

|

|

|

Revaluation Model Example pt 2 |

|

|

|

|

Fair Value Model |

Available as measurement option for investmentproperties (under IFRS only) • Investment property measured at fair valuesubsequent to acquisition • Changes in value reported in net income duringperiod of change • No depreciation is recognized over asset’s life • Note that fair value must be disclosed in financialstatements, even if cost model is chosen instead offair value model |

|

|

|

Costs incurred after acquisition |

If costs incurred achieve greater future benefits, capitalize costs(Capital expenditure) • If costs maintain a specific level of service, expense costs(Revenue expenditure) • Major types of expenditures are: – Additions: Increase or extension of existing assets – Replacements, major overhauls, and inspections:Substitution of a new part/component for an existing asset,and overhauls/inspections whether or not physical parts arereplaced – Rearrangement and reinstallation: Moving an asset from onelocation to another – Repairs: Costs that maintain assets in good operatingcondition |

|

|

|

Replacements, major overhauls, and inspections |

Generally meet definition for capitalization, and costsadded to carrying amount • However, replaced assets or previous overhaulsand/or inspections already have a depreciatedcarrying value on books • Therefore, original asset’s carrying value should beremoved • If original cost and accumulated depreciation are notknown, they must be estimated • ASPE is less strict than IFRS and allows for new costto be debited to Accumulated Depreciation or simplyadded to asset’s carrying value |

|

|

|

Rearrangement and Installation |

Accounting treatment for rearrangementand reinstallation costs: 1. If the original installation cost is known,record as a replacement 2. If the original installation cost is not known,cost is expensed3. If the original installation cost is not knownand amount is material, capitalize cost(ASPE) |

|

|

|

Repairs |

• Ordinary repairs are costs that keep assetin good operating condition • Ordinary repairs are treated as anexpense • Examples: replacement of minor parts,repainting, lubricating equipment |

|

|

|

Depreciable amount |

• Depreciable amount is initially calculated as:Original cost of the assetless estimated residual value (or salvage value)• IFRS does not permit the use of salvage value • Residual value is the net amount expected to be receivedfor the asset today if it were of the age and in the conditionexpected at the end of its useful life • Salvage value is the asset’s estimated net realizable valueat the end of the asset’s life • Residual value should be reviewed regularly (at leastannually under IFRS) • Depreciation continues as long as residual value is lowerthan asset’s carrying amount |

|

|

|

Depletion of mineral resources |

Natural resources are depleted (amortized) overtime as they are removed • Depletion is calculated using an activity method(such as units-of-production) • The depletion charge is initially debited toInventory • When the resource is sold, Inventory is creditedand Cost of Goods Sold is debited • Where an equipment’s useful life is clearly linkedto the life of the resource, it is also amortizedusing the units-of-production method |

|

|

|

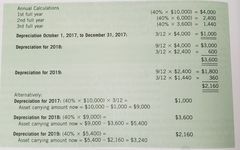

Double declining balance partial year depreciation |

|

|

|

|

Impairment of depreciable assets |

• Impairment occurs when the carrying amount of the long-livedasset (such as PP&E) is greater than its future economicbenefit to the company • There are many external and internal indicators that provideevidence of possible impairment • Management needs to regularly evaluate assets for theseindicators of impairment– IFRS requires this at the end of each reporting period • If there is an indicator of possible impairment, then the assetmust be tested for impairment • Two main approaches to measuring impairment losses are: – Cost recovery impairment model – Rational entity impairment model |

|

|

|

Cost recovery impairment model |

• Under this model, an asset is impaired only if carrying amountcannot be recovered from using and eventually disposing ofthe asset (recoverability test) – i.e. impaired if carrying amount > undiscounted future net cashflows • Impairment loss is then measured as asset’s – carrying amount– less fair value • Fair value of the asset is best measured by quoted marketprices in active markets– It is by its nature a present value or discounted measure • Impairment losses cannot be reversed • Applied by ASPE |

|

|

|

Rational entity impairment model |

• This approach assumes that an entity makes rationaldecisions in managing its long-term assets – If management can earn a higher return from using an asset (value in use) thenthe company will continue to use it– If management can earn a higher return from selling the asset, then the rationaldecision is to sell it (fair value less cost of disposal) • An impairment loss is determined by comparing the asset’scarrying amount and recoverable amount (greater of the valuein use and the fair value less cost of disposal) • If carrying amount < recoverable amount, then there is noimpairment loss • If carrying amount > recoverable amount, then impairmentloss is difference between two values -used by IFRS |

|

|

|

Value in use vs. fair value less costs of disposal |

Value in use– Is the present value of the future cash flows expected to bederived from the asset’s use and subsequent disposal • Fair Value Less Cost of Disposal– Is the amount currently expected to be received from the sale ofthe asset in an orderly transaction between market participantsafter subtracting incremental costs directly related to the sale ordisposal |

|

|

|

Asset Groups and cash generating units (CGU) |

Many assets do not generate cash flows independently, so impairmentanalysis cannot be done at the level of the individual asset • These assets are identified with an asset group or cash-generating unit(CGU) – i.e. “smallest identifiable group of assets that generates cash inflowsthat are largely independent of the cash flows from other assets orgroups of assets” (IAS 36.6) • Both cost recovery and the rational entity impairment models are thenapplied to the groups of assets, instead of the individual asset • Any impairment losses are then allocated to individual assets on a prorata basis • No individual asset should be reduced below its fair value (under costrecovery model) or recoverable amount (under rational entity model) – ifthese amounts are known |

|

|

|

Held for Sale |

• Long-lived asset is classified as held for sale if the companyintends on disposing the asset by sale and meets strict criteria(described in Ch. 4) • Held for sale assets are– Reported separately on the statement of financial position– Not depreciated– Measured at the lower of • Carrying amount, and • Fair value less costs to sell • Subsequent increases in net realizable value may berecognized as gains, but only to the extent they offsetpreviously recognized losses |

|

|

|

Derecognition |

• Plant assets may be:– retired voluntarily, or disposed of by sale,exchange, involuntary conversion, donation • Depreciation is recorded up to the date of disposalbefore determining gain or loss • Gains or losses from disposal are normally shownwith “Other” revenues and expenses in the incomestatement |

|

|

|

Disclosure |

There are many significant disclosures required for property,plant, and equipment• Types of disclosures include the following: – cost and the accumulated depreciation – depreciation method and rate or period – assumptions surrounding fair-value-relatedmeasurements – carry amounts of assets held for sale – outstanding contingencies • Specific standards under IFRS generally have moreextensive disclosure requirements compared to ASPE |

|

|

|

PP&E Ratios |

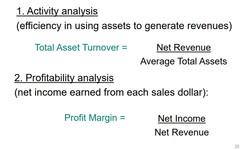

asset turnover x profit margin = rate of return (net income/average total assets) |

|

|

|

Purchased Intangibles |

Cost includes all expenditures that are necessary to get theintangible asset ready for its intended use (e.g., purchaseprice, legal fees)• If there are delayed payment terms, recognize financingexpense (interest) • If acquired for shares, cost is generally measured at asset’sfair value (or value of shares if value of asset cannot bedetermined) • If intangible assets are exchanged for non-monetary assets,the fair value of the item given up or the fair value of theintangible received is used to determine cost • For a “basket purchase” of intangibles, the cost is allocatedbased on fair values

Business combination: when one businessacquires control over one or more otherbusinesses • Identifiable intangible assets acquired arerecognized at fair value |

|

|

|

Internally developed intangibles |

• Costs that a company incurs internally to create intangibles(such as patents and brand names) • Internally developed intangibles present significantchallenges: – Recognition: When to recognize? Is there probability offuture cash flows? – Measurement: What costs to capitalize vs. expense? Howto reliably measure the costs? • IFRS requires that costs be capitalized when certain criteriaare met, and expense all other costs • ASPE also allows for an accounting policy option to expenseall costs relating to internally generated intangibles |

|

|

|

Research and development costs |

All research costs are charged to expense whenincurred • Development costs are charged to expenseexcept in certain defined circumstances |

|

|

|

Development cost capitalization criteria |

Development cost capitalization criteria: 1. Technical feasibility 2. Intent to complete for use or sale 3. Ability to use or sell 4. Availability of resources (technical, financial, andother) needed to complete, and to use or sell 5. If the intent is to sell, a market exists and is clearlydefined; if the intent is to use, there is a definableuse/need 6. Product/process clearly defined, and costs can beidentified |

|

|

|

Examples of development costs |

Examples of development costs include the following: 1. Materials and services consumed 2. Direct personnel costs (e.g., salaries) 3. Fees needed to register a legal right 4. Amortization of other intangibles needed togenerate the asset 5. Interest and borrowing costs |

|

|

|

Measurement after acquisition |

There are two models for measuring intangibleassets subsequent to initial recognition: – Cost model (CM) – Revaluation model (RM) • Under ASPE, cost model is the only methodallowed • Revaluation model requires that intangible assetshave fair value determined in an active market • Both models are applied in same way as forproperty, plant, and equipment |

|

|

|

Limited-life vs. indefinite life intangibles |

Limited-life: An intangible asset with limited (or finite)useful life is amortized over its useful life. Intangibles assumed to have no residualvalue, unless:1. There is a commitment to purchase, or2. There is an observable market Indefinite life: An intangible asset with an unlimited (orinfinite) useful life is not amortized • Because of the potential effect on the financialstatements, it is important for management toreview whether the intangible asset still has anindefinite life |

|

|

|

Impairment of limited-life intangibles |

• Impairment of limited-life intangibles is covered by same impairmentmodels and standards as for long-lived tangible assets • Potential impairment is assessed – under ASPE, when events or circumstances indicate thatcarrying value may not be recoverable – Under IFRS, at the end of each reporting period • Two impairment models are:– Cost recovery impairment model (ASPE) – Rational entity impairment model (IFRS) |

|

|

|

Impairment of indefinite-life intangibles |

ASPE • Use fair value test only • Fair value of intangible compared to the carrying amount • When fair value is less than carrying amount, impairment hasoccurred and loss is recorded • The recoverability test is not used for indefinite-life intangibleassets IFRS • Compare carrying value and recoverable amount on anannual basis, whether or not there is indication of impairment. |

|

|

|

Goodwill |

Goodwill is the excess of the considerationtransferred to acquire the business over the fairvalue of the identifiable tangible and intangible netassets acquired in a business combination • Goodwill can be acquired and sold only when abusiness combination occurs • Goodwill cannot be separated from the business • Internally-generated goodwill is not capitalized |

|

|

|

Bargain purchase |

A “bargain purchase” or negative goodwillarises when fair value of acquiredidentifiable net assets is greater than theconsideration transferred for those assets • The current standard requires any negativegoodwill be recognized immediately as again in net income after a thoroughreassessment of the variables used indetermining its amount. |

|

|

|

Goodwill impairment ASPE |

Impairment test done whenever events or changesin circumstances indicate possible impairment • Impairment test for other assets in group is donebefore the impairment test for goodwill • Impairment loss exists if carrying amount ofreporting unit including goodwill > fair value ofreporting unit – Loss is calculated as amount of excess • Goodwill impairment losses cannot be reversed |

|

|

|

Goodwill impairment IFRS |

Impairment test done annually and also wheneverthere is indication that CGU may be impaired • Impairment loss exists if carrying amount of unitincluding goodwill > recoverable amount of unit – Loss is calculated as amount of excess • Impairment loss is allocated first to goodwill andthen to other assets on a relative carrying amount(proportionate) basis • Goodwill impairment losses cannot be reversed |

|