![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

36 Cards in this Set

- Front

- Back

|

What is a Financial Instrument? |

A financial instrument is any contract that gives rise to a financial asset in one entity and a financial liability or equity instrument of another entity.

|

|

|

Which accounting standards deal with Financial Assets and Financial Liabilities? |

1. IAS 32 Financial instruments: presentation

2 IFRS 7 Financial instruments: disclosures 3. IFRS 9 Financial instruments IAS 32 deals with the classification of financial instruments and their presentation in financial statements. IFRS 9 deals with how financial instruments are measured and when they should be recognised in financial statements. IFRS 7 deals with the disclosure of financial instruments in financial statements. |

|

|

What is a Financial Asset? |

A financial asset is any asset that is:

• cash • a contractual right to receive cash or another financial asset from another entity • a contractual right to exchange financial assets/liabilities with another entity under conditions that are potentially favourable. • an equity instrument of another entity Potentially favourable means that we will be receiving most of the benefits of owning the asset. |

|

|

Give examples of Financial Assets |

1. Trade receivables

2. Options 3. Investment in equity shares Just think...owning shares or debt in another company. |

|

|

What is a Financial Liability? |

A financial liability is any liability that is a contractual obligation:

1. To deliver cash or another financial asset to another entity, 2. To exchange financial instruments with another entity under conditions that are potentially unfavourable. 3. That will or may be settled in the entity’s own equity instruments. |

|

|

Give examples of Financial Liabilities? |

Examples of financial liabilities include:

1. Trade payables 2. Debenture loans 3. Redeemable preference shares |

|

|

What is an Equity Instrument? |

An instrument that is not traded for cash or any other instrument but is instead settled in shares. |

|

|

Classification: When do we recognise Financial Assets? |

An entity should recognise a financial asset on its statement of financial position when, and only when, the entity becomes party to the contractual provisions of the instrument |

|

|

Classification: How are Financial Assets measured on initial recognition? |

At initial recognition, all financial assets are measured at fair value. This is likely to be the purchase consideration paid to acquire the financial asset.

Transaction costs may be added to the cost of the asset. |

|

|

What are the two tests that must be considered when classifying FA that are debt instruments? |

1. The Business Model Test 2. The Contractual Cash flows test NB. These tests are only conducted on debt instruments that are Financial Assets. i.e We bought the debt of another company. |

|

|

What is the Business Model Test? |

The business model test sets out the objective of the entity's business model which can either be: 1. To hold the financial asset to collect the contractual cash flows or 2. to sell the financial asset prior to maturity to realise changes in fair value. |

|

|

What is the Contractual Cash Flows Test? |

The contractual cash flow characteristics test determines whether the contractual terms of the financial asset give rise to cash flows on specified dates that are solely of principal and interest based upon the principal amount outstanding.

|

|

|

How do we then classify debt instruments? |

1. Upon conducting the tests, if the entity intends to: 1. Hold the asset to collect cash flows 2. Cash flows are only principal interest The the debt instrument should be held at AMORTISED COST Any other FA that is a debt instrument is held at FVTP/L. |

|

|

Can we designate to avoid an accounting mismatch? If yes explain. |

Even if a financial instrument passes both tests, it is still possible to designate a debt instrument as FVTPL if doing so eliminates or significantly reduces a measurement or recognition inconsistency (i.e.accounting mismatch)that would otherwise arise from measuring assets or liabilities or from recognising the gains or losses on them on different bases. |

|

|

How do we classify equity instruments? |

1. All shares are held at FVTP/L. That means, there will be changes in the FV each year, and those changes will go straight to the I/S. 2. If the shares are NOT held for trading purposes i.e. we don't intend to sell the shares, then we hold them at FVTOCI. That means that changes in FV each year are recorded in OCI rather than I/S. |

|

|

Can the classification be changed or re-classified? |

1. There should be no reclassification between FVTP/L and FVTOCI. 2. Reclassification between Amortised Cost and FVTP/L is permitted but ONLY where there is a change in the business model or to avoid an accounting mismatch. |

|

|

Can gains or losses be recycled upon derecognition? |

NO! We do not recycle gains and losses on derecognition, they are instead transferred from other reserves to retained earnings. |

|

|

How do we classify Financial Liabilities? |

Most Financial Liabilities are held at FVTP/L. They are usually held for trading purposes in the short term, e.g. Derivatives They are revalued to FV each year with gains and losses to be recognised in the I/S. For others NOT held for trading purposes, for e.g. Bank Loans; hold these at AMORTISED COST. |

|

|

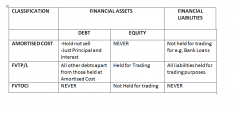

CLASSIFICATION SUMMARY |

|

|

|

How do we measure Financial Assets @ Amortised Cost? |

1. Recognise Financial Asset @ Cost + Transaction Costs 2. Calculate Effective Interest: DR. Asset (SFP) CR. Income (I/S) 3. To receipts of cash over the years: DR. Cash CR. Asset |

|

|

How do we measure Financial Liabilities @ Amortised Cost? |

1. Recognise Financial Liabilities @ Cost less discounts and issue costs. 2. Calculate Effective Interest: DR. Income (I/S) CR. Liability (SFP) 3. Any payments of cash over the years: DR. Liability CR. Cash |

|

|

How do we measure at FVTP/L? |

1. Measure the value of the financial instrument on initial recognition. 2. Measure FV of Financial Instrument at each year end. 3. Revalue to new amount 4. Post the gain/loss to the income statement. |

|

|

How do we measure at FVTOCI? |

Same as FVTP/L except the gains and losses are instead recognised in OCI. |

|

|

How do we treat with Preference Shares? |

If preference shares are irredeemable they are classified as equity.

If preference shares are redeemable they are classified as a financial liability. |

|

|

Distinguish between redeemable and irredeemable preference shares. |

Redeemable preference shares

These are preference shares that the company will buy back at an agreed date in the future. They are classified as non-current liabilities in the statement of financial position. Irredeemable preference shares These are preference shares that will not be bought back by the company. Shareholders will continue to earn dividends as long as profit is earned. They are listed under heading equity in the statement of financial position of a company. |

|

|

Distinguish between liability and equity |

The key distinguishing feature for liabilities and equity is identifying whether or not a contractual obligation will arise. If a contractual obligation exists to repay principal or interest then it is a liability. If there is no contractual obligation to deliver cash or any other financial asset then it is regarded as equity. |

|

|

Why is the distinction between liability and equity so important? |

1. It can have a significant impact on the entity's gearing ratio, reported earnings and debt covenants. 2. If an entity issues an instrument and classifies it as a liability, then gearing will rise and the entity will appear more risky to potential investors. The servicing of the finance will be charged to profit or loss reducing profits. 3. If an entity issues an investment and classifies it as equity then gearing will fall. The servicing of the finance will be charged directly to retained earnings and so will not impact profit. |

|

|

What is a Compound Instrument? |

A compound instrument is a financial instrument that has characteristics of both equity and liabilities, such as a convertible loan.

Be careful here as these are treated differently according to whether they are receivable loans (assets) or payable loans (liabilities) |

|

|

How do we account for compound instruments? |

These are to be accounted for using split accounting, recognising both the equity and liability components of the instrument.

STEP 1: Calculate liability component first– Based on present value of future cash flows assuming non conversion.– Apply discount rate equivalent to interest on similar non convertible debt instrument. STEP 2: Equity = remainder (i.e. deduct the present value of the debt from the proceeds of the issue |

|

|

Is offsetting of Financial Assets and Liabilities permitted? |

Only in Limited circumstances. The net amount may only be presented in the statement of financial positionwhen the entity: 1. has a legally enforceable right to set off the amounts, and 2. intends either to settle on a net basis or to realise the asset and settle the liability simultaneously. |

|

|

When should Financial Instruments be de-recognised? |

1. Financial asset – when, and only when, the contractual rights to the cash flows of the financial asset have expired.

2. Financial Liabilities- when, and only when, the obligation specified in the contract is discharged, cancelled or expires. |

|

|

What are the two types of Convertible Loans? |

1) Payable Convertible Loan 2) Receivable Convertible Loan |

|

|

What is the difference between a receivable convertible loan and a payable convertible loan? |

For a receivable convertible loan - it fails the cashflow test - as one receipt may be shares and not just capital and interest.

Therefore a receivable convertible loan cannot be amortised cost and so is a FVTPL item. However, there are no such tests for liabilities, and so a payable convertible loan is not held for trading and so falls into the amortised cost category. |

|

|

What are transaction costs? |

There will usually be brokers’ fees etc to pay and how you deal with these depends on the category of the financial instrument.

|

|

|

How do we treat with Transaction Costs? |

For FVTPL - these go to the income statement.

For everything else they get added/deducted to the opening balance. So if it is an asset - it will increase the opening balance. If it is a liability - it will decrease the opening balance. Nb. If a company issues its own shares, the transaction costs are debited to share premium |

|

|

When does De-recognition of Financial Asset occur? |

De-recognition of a financial asset occurs where:

1) The contractual rights to the cash flows of the financial asset have expired (debtor pays), or 2) The financial asset has been transferred (e.g., sold) including the risks and rewards. |