Reading...

![]()

Play button

![]()

Play button

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

40 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

What are scarce resources/ factors of production ?

|

Land- line natural resources

Labor- all human resources Capital - all man-made aids to production 🔹Euntrepreneurship - the ability to perceive a want and to see how resources can be used to fulfill that want |

There are 4

|

|

|

What are ulimited wants?

|

1. Goods

2. Services |

There are 2

|

|

|

What do we have to determine about or unlimited wants?

|

If they are necessities or luxuries, which depends on when (era) and where (location)

|

2 things

|

|

|

What choice do we have to make?

|

(always constant)

Can't give to someone without taking from another |

Nothing in life is free...

|

|

|

What is opportunity cost?

|

- the most desired good, service, activity that is for gone by choosing one alternative instead of another

*The forgone opportunity of the next best alternative |

It is based on choices

|

|

|

What is the production possibilities curve?

|

It shows the alternative combinations of goods and services that could be produced with all available resources and technology.

-show that given our resources that different combinations that are possible |

Given our resources, what is possible?

|

|

|

What is the law of increasing opportunity cost?

|

When more time, effort, resources are devoted to one activity,

The cost in terms of the other activity or activities sacrifice becomes greater and greater |

Greater and greater

|

|

|

Why does the sacrifice become greater and greater (Law of increasing opportunity cost)?

|

The reason is because the specialization of inputs

↪Specialization of one good or service comes at the cost of producing another |

|

|

|

How does the production possibilities curve effect/ show opportunity cost?

|

The reallocation of resources to one good come at the cost of sacrificing resources to another service.

|

One for the other

|

|

|

How does the production possibility curve show specialization of resources?

|

High production of one good comes at the cost of low production of another

|

|

|

|

How does the production possibilities curve show the increasing opportunity cost?

|

As you produce more and more of one good the sacrifices of producing another becomes greater and greater

|

|

|

|

How can the production possibility curve increase?

|

- by growth; increasing standards of living

- so we must be able to increase our resources and technology |

2 must increase

|

|

|

What does it mean to produce on the curve, inside, and outside the curve?

|

➖ inside: under utilizing resources.

✅ on the curve: fully utilizing resources. ➕ ouside: over utilizing resources. |

|

|

|

What did Adam Smith write in his book?

|

That people who are guided by their own self interest tend to promote the greater good as well

|

|

|

|

What are the 3 alternatives for how people act?

|

1. Rely on self-interest

2. Enforce or coerced by the government 3. Rely on their benevolence |

|

|

|

What is harmony of interests?

|

Capitalists/ entreprenuers have to voluntarily "hook us up" based on their self interest.

- Responding to what customers want. |

Everybody's happy

|

|

|

What is the definition of efficient (re)allocation of resources?

|

- Prices reflect what you need

- relying on people to be frugal, mindful, get what they need. Which is guaranteed if you rely on their self interest. |

|

|

|

What is the invisible hand?

|

-Guides market assistance in the market economy.

👉⭐ prices are the reason we don't rely on a central authority, it needs to reflect reality and it tells the story of scarcity and demand. 👈 -giant billboard sign that is a market signal to businesses. |

|

|

|

What is Laissez-faire?

|

The government needs to leave (the market) alone, don't distort (the market).

|

|

|

|

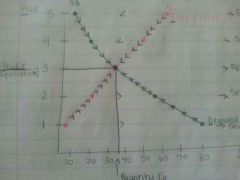

What is price determination?

|

Equal price and quantity demand/supply are determined by the interaction between the supply curve and demand curve.

|

2 curves

|

|

|

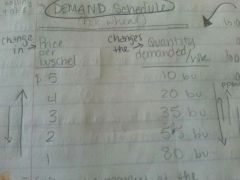

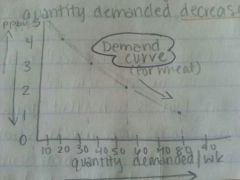

Demand schedule?

|

- explained by the law of demand.

-A Change in the price changes the quantity demand of the product per week. ⭐ it reflects the market at the time; the determinants of the demand. |

|

|

|

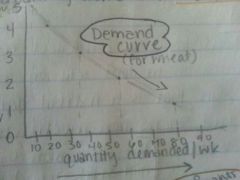

What is the law of demand?

|

- As the prices of a good decrease⬇, the quantity demanded increases ⬆.

- As the price of a good increases⬆, the quantity demanded decreases⬇. |

⬇, ⬆.

⬆, ⬇. |

|

|

What are the determinants of demands?

|

1. Income of consumers

2. Tastes of consumers (what they want) 3. Prices of related goods >substitute ($tea 🔼, Dcoffee 🔼) >compliment ($hotdog🔽,Dbuns🔼) 4. Price expectations of consumers (expect $⬆= D⬇, and the opposite) 5. Number of consumers |

They're 5.

Must keep them ceteris paribus. |

|

|

What happens with changes in demand?

|

Caused by - a change in one of the determinants of demand.

Result in - a whole new demand schedule and curve. |

A cause and effect

|

|

|

What happens with a change in quantity demanded?

|

Caused by- a change in the price of a good itself.

Results in - movement from one point to another point on the same demand curve. |

A cause and effect

|

|

|

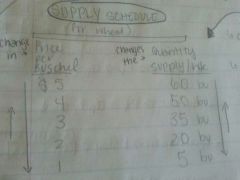

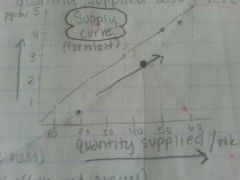

Supply schedule?

|

- a change in the price changes the quantity supplied per week.

- based on the law of supply - Reflects the market at the time and the determinants of supply. |

|

|

|

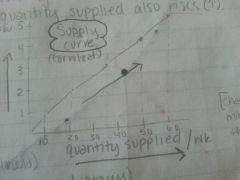

What is the law of supply?

|

As the price of a good decreases⬇, the quantity supplied also decreases⬇.

As the price of a good increases⬆, the quantity supplied also increases⬆. |

⬇, ⬇. ⬆, ⬆.

|

|

|

What are the determinants of supply?

|

1. Cost of inputs (use it for their business).

2. Prevailing technology (anything that affects production process). 3. Number of sellers 4. Price expectations of suppliers. (in the future $🔼, S🔽) 5. Subsidies and taxes 6. Price of other goods ($corn🔽, Swheat 🔽) |

There are 6.

Must keep them ceteris paribus. |

|

|

What happens with a change in supply?

|

Caused by - change in one of the determinants of supply.

Results in - a whole new supply schedule and curve. |

Cause and effect

|

|

|

What happens with the change in quantity supplied?

|

Caused by - a change in the price of the good itself.

Results in - movement from one point to another point on the same supply curve. |

A cause and effect

|

|

|

Draw a demand curve?

|

|

|

|

|

Draw a supply curve.

|

|

|

|

|

Show equilibrium price and quantity demanded/supplied.

|

|

|

|

|

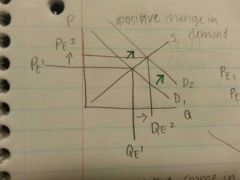

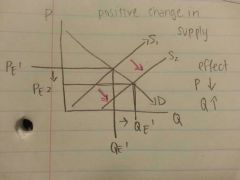

Positive change in demand? The effect?

|

The effect: P ⬆And Q⬆

|

|

|

|

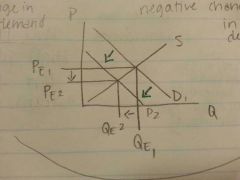

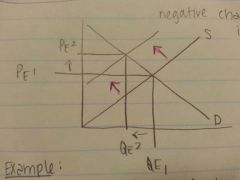

Negative change in demand? The effect?

|

Effect: P ⬇and Q ⬇

|

|

|

|

Positive change in supply? The effect?

|

The effect : P⬇ and Q⬆

|

|

|

|

Negative change in supply? The effect?

|

The effect: P⬆ and Q⬇

|

|

|

|

Price of a demanded compliment & substitute good changes?

|

Compliment: $corn⬆, Dwheat⬆

Substitute: $ hotdogs⬇, Dbuns ⬆ |

|

|

|

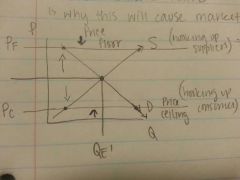

What is a price floor? Draw.

|

When the government raises the price to a certain point where it cannot fall, so it hits a floor.

-benefits the suppliers -⬆supply ⬇demand -creates a surplus -creates market failure |

|

|

|

What's a price ceiling? Draw.

|

When the government lowers the price so much that. It cannot rise anymore, hits a ceiling.

-hooking up the consumer -⬇supply.⬆demand. -creates a shortage - causes market failure |

|