![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

43 Cards in this Set

- Front

- Back

|

Total Revenue (TR) |

The amount a firm receives for the sum of its output. |

|

|

Total cost (TC) |

The market value of the inputs a firm uses in production

TC = FC + VC |

|

|

Profit |

Total revenue minus total cost Profit = TR - TC |

|

|

Explicit Costs (EC) |

Input costs that require an outlay of money by the firm. |

|

|

Implicit (IC) |

Input costs that do not require an outlay of money by the firm. Opportunity cost forgone. |

|

|

Economic Profit |

Total revenue minus total cost, including IC and EC. Economic Profit =TR - TC (IC + EC) |

|

|

Production function |

The relationship between quantity of inputs used to make a good and the quantity of outputs of that good |

|

|

Marginal product of labor (MPL) |

There increase in output that arises from an additional unit of input ∆Q / ∆L |

|

|

Diminishing marginal product |

The property whereby the marginal product of an input declines as the quantity of the input increases |

|

|

Fixed cost (FC) |

Cost that do not vary with the quantity of output produced |

|

|

Variable cost (VC) |

Cost that vary with the quantity of output produced |

|

|

Average total cost (ATC) |

TC / Q |

|

|

Average total cost (ATC) |

TC / Q |

|

|

Average fixed cost (AFC) |

FC / Q |

|

|

Average variable cost (AVC) |

VC / Q |

|

|

Marginal cost (MC) |

The increase in total cost that arises from an extra unit of production. MC = ∆TC / ∆Q |

|

|

Accounting profit |

Total revenue minus total explicit cost. AP = TR - EC |

|

|

Production function |

The relationship between quantity of inputs used to make a good and the quantity of outputs of that good |

|

|

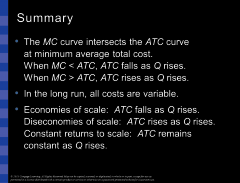

efficient scale |

the quantity of output that minimizes average total cost |

|

|

The property whereby long-run average total cost falls as the quantity of output increases |

Economies of scale |

|

|

the property whereby long-run average total cost rises as the quantity of output increases |

diseconomies of scale |

|

|

the property whereby the long-run ATC stays the same as the quantity of output changes |

constant returns to scale |

|

|

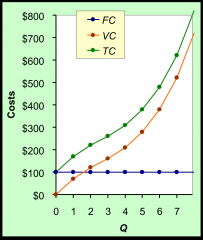

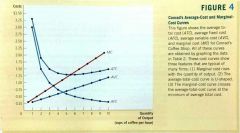

TC falls somewhere between FC and VC |

|

|

|

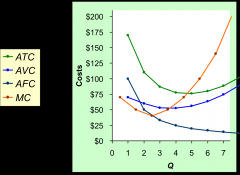

The various cost curves together |

|

|

|

Explain the difference in cost over short run vs long run |

Shortrun: Some inputs are fixed (e.g.,factories, land). The costs of these inputs are FC. Longrun: All inputs are variable (e.g.,firms can build more factories or sell existing ones). Inthe long run, ATC atany Q is cost per unit using the mostefficient mix of inputs for that Q(e.g., the factory size with the lowest ATC). |

|

|

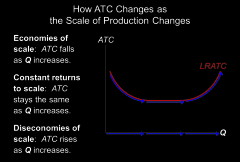

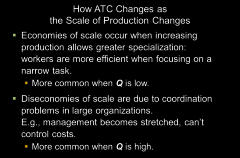

Explain the concepts behind Economies of scale, constant return on scale and disconomies of scale. Note: This is a LRATC projection |

|

|

|

How does ATC change as the scale of production changes |

|

|

|

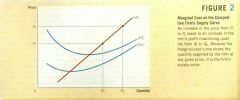

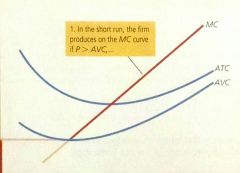

Explain the relationship between MC and ATC |

The MCcurve intersects the ATCcurve at minimum average total cost. When MC When MC >ATC, ATCrises as Qrises. |

|

Summary for Ch 13 |

|

|

|

|

|

|

a market with many buyers and sellers trading identical products so that each buyer and seller is a price taker |

competitive market |

|

|

What three characteristic are typical to have a perfectly competitive market. Two are required |

1. there are many buyers and sellers in the market place 2. the goods offered by the various sellers are largely the same. 3. Firms can freely enter or exit the market *NOTE This is not always needed* |

|

|

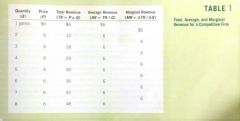

Average Revenue (AR) =

|

Total revenue (TR) divided by the quantity sold

AR = TR / Q *NOTE about AR: Because the formula it essentially (P x Q) / Q, AR equals the price of the good.* |

|

|

Total revenue (TR) = |

TR = P x Q |

|

|

Marginal Revenue (MR)= |

The change in the TR from an additional unit sold.

MR = ∆TR / ∆Q |

|

|

Profit = |

Profit = TR - TC |

|

|

Change in Profit = |

Change in profit = MR - MC |

|

|

What three features of the cost curves are thought to describe most firms |

1. The MC curve is upward sloping 2. The ATC curve is U-shaped 3. The MC curce crosses ATC curve at the minimum of ATC |

|

|

In a competitive market place, what can be said about the price in relation to the AR and MR |

P = AR = MR |

|

|

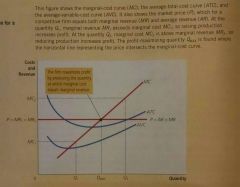

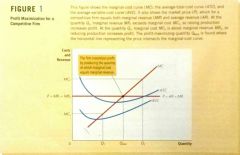

Profit maximization for competitive firms |

|

|

|

|

|

|

|

|

|

|