Reading...

![]()

Play button

![]()

Play button

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

16 Cards in this Set

- Front

- Back

|

What is Production Function?

|

A technological relationship expressing the maximum quantity of a good attainable from different combinations of factor inputs.

|

|

|

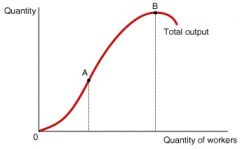

In short-run which resources are fixed, which are not?

|

Labor is variable and all other resources are fixed.

|

|

|

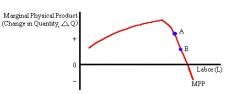

What is the formula for MPP?

|

The change in total output associated with one additional unit of input

|

|

|

What is the law of diminishing returns?

|

The marginal physical product of a variable input declines as more of it is employed with a given quantity of other (fixed) inputs

|

|

|

Graph MPP

|

|

|

|

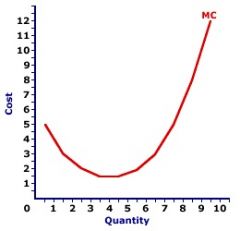

What is the formula for Marginal Cost?

|

The increase in total cost associated with a one unit increase in production.

|

|

|

Graph Marginal Cost.

|

|

|

|

What is the relationship of MPP and MC?

|

When MPP is increasing then MC must be failing and vice versa.

|

|

|

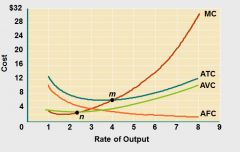

What is Total Cost?

|

The market value of all resources used to produce a good or service.

|

|

|

What is fixed cost?

|

Costs of production that do not change when the rate of output is altered (e.g. the cost of basic plant and equipment)

|

|

|

What is Variable cost?

|

Costs of production that change when the rate of output is altered (e.g. labor and material costs)

|

|

|

Graph MC, TC FC and VC

|

|

|

|

What is the relationship between average total cost and marginal cost?

|

Marginal cost is the change in total cost for a change in quantity. Average total cost is the per unit burden, therefore when MC < ATC then AC lowers.

|

|

|

Explain the difference between accounting costs and economic costs.

|

Accounting costs are explicit cost such as direct payments to resources. Economic costs are explicit and implicit cost which are value of resources used even w/o direct payment.

|

|

|

Explain the difference between short run and long run cost of production.

|

With short run labor is variable where all other resources are fixed. With long run all resources are variable.

|

|

|

Explain economies of scale.

|

Economies of scale / increse returnes to scale

Inputs double then outputs more than doube Therefore ATC is lower Dis-economies of scale / decrease returns to scale Inputs double then outputs less than double Therefore ATC increases Constant returns to scale Inputs double then outputs double No change in ATC |