Reading...

![]()

Play button

![]()

Play button

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

24 Cards in this Set

- Front

- Back

|

This type of accounting is concerned with reporting financial information to external parties, such as stockholders, creditors, and regulators.

|

Financial accounting

|

|

|

This type of accounting is concerned with providing information to managers for use within the organization.

|

Managerial accounting

|

|

|

A difference in costs between any two alternatives

|

Differential cost

|

|

|

A difference in revenues between any two alternatives

|

Differential revenue

|

|

|

A cost that is incurred to support a number of cost objects but that cannot be traced to them individually

|

Common cost

|

|

|

Conversion Cost

|

Direct labor + Manufacturing overhead

|

|

|

Contribution Margin

|

The amount remaining from sales revenues after all variable expenses have been deduced.

|

|

|

Manufacturing Overhead

|

All manufacturing costs except direct materials and direct labor.

|

|

|

Prime Cost

|

Direct materials + Direct labor

|

|

|

Unadjusted COGS

|

Beginning finished goods inventory + COGM - Ending finished goods inventory

|

|

|

A credit balance in the Manufacturing Overhead account that occurs when the amount of overhead cost applied to WIP exceeds the amount of overhead cost actually incurred during the period.

|

Overapplied overhead.

|

|

|

A debit balance in the Manufacturing Overhead account that occurs when the amount of overhead cost actually incurred exceeds the amount of overhead cost applied to WIP during a period.

|

Underapplied overhead

|

|

|

COGM

|

The manufacturing costs associated with the goods that were finished during the period.

|

|

|

Conversion Cost

|

Direct labor + Manufacturing Overhead

|

|

|

Equivalent Units (Weighted Average)

|

Units transferred out + EU in the ending WIP

|

|

|

A process costing method in which equivalent units and unit costs relate only to work done during the current period.

|

FIFO

|

|

|

COGM Schedule

|

Direct Materials

BB_Raw Mat Add New Purchases Deduct EB_Raw Mat Deduct Ind. Mat in MO Direct Labor MO applied Add BB_WIP Deduct EB_WIP |

|

|

COGS Schedule

|

BB_FG

Add COGM Deduct EB_FG Add Underapplied MO or Subtract Overapplied |

|

|

Applied Overhead =

|

POHR * Amount of Allocation Incurrred

|

|

|

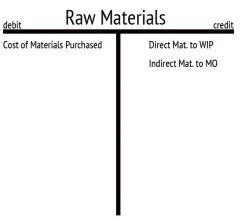

Raw Materials T-Chart

|

|

|

|

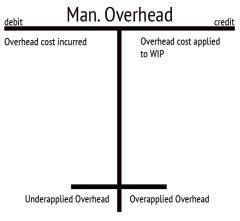

Manufacturing Overhead T-Chart

|

|

|

|

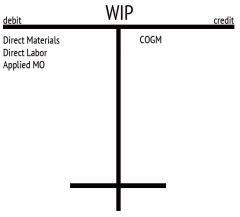

WIP T-Chart

|

|

|

|

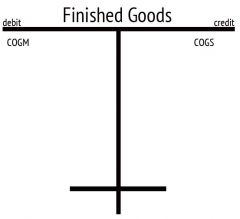

Finished Goods T-Chart

|

|

|

|

COGS T-Chart

|

|