![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

51 Cards in this Set

- Front

- Back

|

What are the four the purpose of Capital? |

1- Absorb losses2- Promote Public Confidence3- Restrict Excessive Asset Growth4- Provide Protection to Depositors and the FDIC insurance Fund |

|

|

What does Common Equity Tier 1 Capital consist of? |

1. Qualifying common stock and related surplus net of Treasury stock2. Retained Earnings 3. Certain Accumulated Other Comprehensive Income (if bank did not opt out)4. Regulatory deductions or adjustments5. Qualifying common equity tier 1 minority interests |

|

|

Part 324 requires what items to be deducted from Common Equity Tier 1 Capital? |

1. DTAs from net operating loss2. Goodwill3. Tax-credit carryforwards4. Other intangible assets (excluding MSAs)5. Gains on sales of securities exposures6. Certain investments in another financial institution’s capital interests |

|

|

What are the threshold deductions for MSAs, DTAs, and significant investments in another unconsolidated institution’s common stock? |

• Must deduct exposure that exceeds 10% of CET1• Aggregate limit of 15% total for all 3• Amount of items not deducted are assigned a 250% risk-weight (once Part 324 is fully phased in) |

|

|

What is included in Additional Tier 1 Capital? |

• Qualifying noncumulative preferred perpetual stock• Bank-insured SBLF and TARP that previously qualified for Tier 1• Qualifying Tier 1 minority interest less certain investments in other consolidated financial institution’s instruments that would qualify ass additional Tier 1 capital. |

|

|

How do you calculate Tier 2 Capital? |

• ALLL - up to 1.25% of gross RWA• qualifying preferred stock• Subordinated debt• Qualifying Tier 2 minority interests• MINUS any deductions in the Tier 2 instruments of an unconsolidated financial institution. |

|

|

What is Tier 2 Capital limited to? |

Part 324 eliminates limits on term subordinated debt, limited life preferred stock, and the amount of Tier 2 allowable in total capital. |

|

|

Investments in the capital instruments of other financial institutions are deducted from where? |

Deductions are made from the corresponding tier of capital (i.e. Tier 1 capital instruments from Tier 1) |

|

|

0% risk weight |

1. Cash; 2. Gold bullion 3. Direct and unconditional claims on the U.S. government, its central bank, or a U.S. government agency; 4. Portions of exposures that are unconditionally guaranteed by the U.S. government, its central bank, or a U.S. government agency, including exposures insured or otherwise unconditionally guaranteed by the FDIC or National Credit Union Administration (NCUA); 5. Claims on certain supranational entities (such as the International Monetary Fund) and certain multilateral development banks; and 6. Claims on and exposures unconditionally guaranteed by sovereign entities that meet certain criteria |

|

|

20% risk weight |

1. Cash items in the process of collection; 2. Portions of exposures that are conditionally guaranteed by the U.S. government, its central bank, or a U.S. government agency, including exposures that are conditionally guaranteed by the FDIC or NCUA; 3. Claims on government-sponsored enterprises (GSEs); 4. Claims on U.S. depository institutions and NCUA-insured credit unions; 5. General obligation claims on, and claims guaranteed by the full faith and credit of state and local in the United States; and 6. Claims on and exposures guaranteed by foreign banks and public sector entities if the sovereign of incorporation of the foreign bank or public sector entity meets certain criteria |

|

|

50% risk weight |

1. Statutory multifamily mortgage loans meeting certain criteria;2. Prudently underwritten first-lien residential mortgage exposures meeting certain criteria;113. Presold residential construction loans meeting certain criteria;4. Revenue bonds issued by state and local governments in the United States; and5. Claims on and exposures guaranteed by sovereign entities, foreign banks, and foreign public sector entities that meet certain criteria |

|

|

100% risk weight |

1. All claims on foreign and domestic private-sector obligors (including loans to nondepository banks and BHC)2. Claims on commercial firms owned by the public sector3. Customer liabilities to the bank on acceptances outstanding involving standard risk claims4. FA, premises, and ORE5. Common and preferred stock of corporations6. Commercial, credit cards, and consumer loans (except those assigned to lower risk categories)7. Recourse obligations, direct credit substitutes, etc. rated in the lowest investment grade (BBB) 8. Industrial development bonds 9. All obligations of states or political S/D of countries that do not belong to the OECD10. Stripped MBS and others (IO strips that are not credit-enhancing and principal-only strips)11. Claims representing capital of a qualifying securities firm12. Investments in unconsolidated companies, joint ventures; instruments that qualify as capital issued by other banks; deferred tax assets; MSAs, NMSAs, and PCCRs.13. Residential mortgage exposures that do not meet the criteria to qualify for the 50 percent risk weight and junior-lien residential mortgage exposures receive a 100 percent risk weight.14. All Corporate exposures |

|

|

150% risk weight |

1. A sovereign exposure must be assigned a 150 percent risk weight immediately upon an event of sovereign default 2. Loans and other exposures that are 90 days or more past due. (Unless 1-4 Family in 100%) 3. HVCRE exposure is a credit facility that finances or has financed the acquisition, development, or construction (ADC) of real property, unless the facility finances: • One- to four-family residential properties; • Certain community development projects; • The purchase or development of agricultural land; or • Commercial real estate projects in which: o The LTV ratio is less than or equal to the applicable maximum supervisory LTV ratio; o The borrower has contributed capital to the project in the form of cash or unencumbered readily marketable assets (or has paid development expenses out-of-pocket) of at least 15 percent of the real estate’s appraised “as completed” value; and o The borrower contributed the amount of capital required by this definition before the bank advances funds under the credit facility, and the capital contributed by the borrower, or internally generated by the project, is contractually required to remain in the project throughout the life of the project. |

|

|

100% Conversion Factor |

• Financial SBLOC - Financial Standby Letters of Credit• Forward agreements • Participations sold with recourse• Sale and repurchase agreements (Repo)• Securities, indemnifies the customer against loss• Guarantees;• Repurchase agreements (the off-balance sheet component of which equals the sum of the current market values of all positions the bank has sold subject to repurchase);• Credit-enhancing representations and warranties (see the definition for the inclusion for the 120-day safe harbor);• Off-balance sheet securities lending transactions (the off-balance sheet component of which equals the sum of the current market values of all positions the bank has lent under the transaction);• Off-balance sheet securities borrowing transactions (the off-balance sheet component of which equals the sum of the current market values of all non-cash positions the bank has posted as collateral under the transaction); |

|

|

50% Conversion Factor |

• Pf – SBLOC - Performance standby letters of credit • Unused portions of commitments with an original maturity exceeding one year (Ex. Commercial LINE of Credit with a maturity exceeding 1 year)• RUFs - Revolving Underwriting Facilities (RUFs, Contingent 1 Liab.)• NIFs - Note Issuance Facilities (NIFs, Contingent 1 Liab.) |

|

|

20% Conversion Factor |

• Commercial letters of credit (contingencies that arise from the movement of goods, ST, self-liquidating, trade-related contingencies) (Ex. Commercial LETTER of Credit)• Commitments with an original maturity of one year or less that are not unconditionally cancellable by the bank; and• Self-liquidating, trade-related contingent items that arise from the movement of goods, with an original maturity of one year or less. |

|

|

0% Conversion Factor |

Unused Commitments with the following:• Retail credit card lines and related plans if unconditional option to cancel at any time |

|

|

What is deducted from the denominator when calculating the RBC ratio? AKA. TRWA |

All assets that are deducted from capital in the numerator. (Only items that are risk-weighted and deducted from Total Capital) • Intangibles other than allowed portion of MSRs, NMSAs, and PCCRs• Investments in unconsolidated majority owned banking and finance subsidiaries• Investments in securities subsidiaries (12 CFR 337.4) • Reciprocal holdings of capital instruments banks• Deferred tax assets disallowed for Tier 1• The disallowed portion of the allowance. |

|

|

What is each category of contingent liabilities? |

• Category I contingent liabilities will result in a simultaneous increase in bank assets if it converts to an actual liability• Category II contingent liabilities are those were a claim on assets arises without an equivalent increase in assets. |

|

|

Are off-balance sheet risks included in the RBC calculations for risk-weighted assets? |

Yes |

|

|

What is the difference between loss contingency, potential loss, or estimated loss? |

Loss Contingency: Existing condition involving uncertainty as to possible loss if/when future events occur or fail to occur(Only refers to Category II) Potential Loss: Contingent liabilities where there is substantial and material risk of loss (Category 2 Liability, on Capital Calculations Page – Memo Section (not actually deducted from Capital). Estimated Loss: From a loss contingency, recognized if probable that an asset has been impaired or a liability incurred as of the exam date and the amount of the loss can be reasonably estimated (Category 2 Liability, On Capital Calculations Page – Other Adjustment to Tier 1 Capital (deduct from T1) |

|

|

What are the primary risks associated with standby letters of credit? |

Credit risk and funding risk (Liquidity) |

|

|

1. Traveler’s Letter of Credit |

Addressed by bank to correspondents authorizing draft by person named meeting specified terms. |

|

|

2. Sold for Cash Letter of Credit - |

- Sold, and bank receives funds from account party at issuance (not a continent liability, but DDA) |

|

|

3. Commercial Letter of Credit |

Drafts drawn upon when underlying transaction consummated. Facilitates trade and commerce. |

|

|

4. Standby Letter of Credit |

an irrevocable commitment by bank to make payment to a designated beneficiary and obligates the bank to guarantee or stand as surety for the benefit of a third party. SBLCs can be- Financial - where account party is to make payment to the beneficiary (100% conversion factor) - Performance - where a service is to be performed by account party (50 percent conversion factor) |

|

|

What is a material adverse change clause in a line of credit? |

Allows the bank to terminate the commitment or line of credit arrangement if the customer’s financial condition deteriorates. |

|

|

Category 1 contingent liabilities |

will give rise to an increase in assets if the contingent liability becomes an actual liability1. Letters of Credit2. Unfunded commitments3. Revolving Underwriting Facilities4. Banker’s Acceptances (for participating banks; accepting banks have a direct liability)5. Loan Sold without Recourse – but only in limited situations6. Asset Backed Commercial Paper Programs. |

|

|

Category 2 contingent liabilities |

will not give rise to an increase in assets if the contingent liability becomes an actual liability1. Litigation2. Interest rate futures, forwards and standby contracts3. Trust activities4. Reserve Premium Accounts 5. Cosigned Items and Other Non-ledger Accountsa. Customer Safekeeping i.e. safe deposit boxesb. Collection Itemsc. Consigned Items (travelers checks, US Savings Bonds) |

|

|

What are some UFIRS considerations for Capital? |

Overall Condition Ability to address emerging needs ALLL adequacy Balance sheet composition Off-balance sheet items strength of earnings/ reasonableness of dividends Asset growth Access to capital |

|

|

When a bank is inadequately capitalized do you cite a violation or a contravention of policy? |

A violation is cited only if Tier 1 is under 3 or 4%. A contravention is cited if a bank is undercapitalized due to either of the risk based capital ratios. |

|

|

What is the Minimum Leverage Capital Requirement? |

• 3% - fundamentally sound, well managed, no significant growth, “1” • 4% – for all other institutions |

|

|

If a bank is below minimum leverage capital requirements It will prohibit any application from being approved and bank is required to file a written capital restoration plan to the FDIC RD within _?_ days of date the bank receives notice or it represents an unsafe or unsound practice. |

45 |

|

|

What constitutes an unsafe and unsound practice? (Per Capital Guidelines) |

Being Undercapitalized and not submitting or being in compliance with a plan approved by the FDIC to increase Tier 1 Leverage |

|

|

What constitutes an unsafe and unsound condition? (Per Capital Guidelines) |

Tier 1 Leverage Capital Ratio falls to 2 percent of below |

|

|

under Part 325, a capital restoration plan must be submitted to RD entailing? |

SLOTH 1. Steps the insured depository institution will take to become adequately capitalized 2. Levels of capital to be attained during each year the plan will be in effect 3. Other information as required under the particular Federal agency 4. Types and levels of activities in which the institution will engage; and 5. How the institution will comply with the restrictions in effect under PCA |

|

|

What is Well Capitalized? |

• Total Risk Based Capital – 10.0% or greater • Tier 1 Risk Based Capital – 8.0% or greater • Common Equity Tier 1 – 6.5% or greater • Leverage Ratio – 5.0% or greater • Not subject to an written agreement |

|

|

What is Adequately Capitalized? |

• Total Risk Based Capital – 8.0% or greater • Tier 1 Risk Based Capital – 6.0% or greater • Common Equity Tier 1 – 4.5% or greater • Leverage Ratio – 4.0% or greater |

|

|

What is Undercapitalized? |

• Total Risk Based Capital – Less than 8.0% • Tier 1 Risk Based Capital – Less than 6.0% • Common Equity Tier 1- Less than 4.5% • Leverage Ratio – Less than 4.0% |

|

|

What is Significantly Undercapitalized? |

• Total Risk Based Capital – less than 6.0% • Tier 1 Risk Based Capital – less than 4.0% • Common Equity Tier 1- Less than 3% • Leverage Ratio – less than 3.0% |

|

|

What is Critically Undercapitalized? |

Tangible equity to total assets equal to or less than 2.0% |

|

|

What is Tangible equity capital? |

1. CET1+ Tier 1 + 2. cumulative perpetual preferred stock (including surplus) 3. Less all intangible assets except eligible MSR. |

|

|

When may FDIC reclassify a bank from Well Capitalized to Adequately Capitalized? |

1. Unsafe & Unsound Practice or Condition 2. Consent Order with capital provision |

|

|

May the FDIC reclassify an institution from Significantly Undercapitalized to Critically Undercapitalized? |

No |

|

|

Under Section 38(d) what capital restrictions are there on all banks? |

Pay capital distributions or management fees causing it to become undercapitalized. |

|

|

5 things Undercapitalized, significantly undercapitalized, and critically undercapitalized banks are subject to |

Expansion approval Capital restoration plan monitoring restricted growth capital distributions management fees |

|

|

When will an Undercapitalized bank be subject to the provisions for a Significantly Undercapitalized bank? (3 times) |

• Capital restoration plan was submitted, but disapproved • Failure to submit a capital restoration plan within the period provided (45 days) • Failure to materially comply with an approved capital restoration plan |

|

|

What 8 actions require prior written FDIC approval for CU banks? |

|

|

|

What is the Leverage Capital ratio? |

Tier 1/ adjusted average assets** (average assets for the quarter) ** Need to remember to subtract assets which are deducted from Tier 1 Capital (e.g. disallowed intangibles and Loss) |

|

|

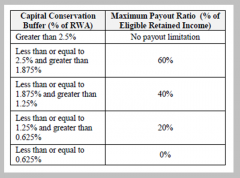

What payments are restricted for institutions with inadequate Capital Conservation Buffers? |

1. Dividends2. Share Buybacks3. Discretionary payments on Tier 1 instruments4. Discretionary bonus payments |

|

|

What are the buffers and associated Payout Ratios? |

|