Reading...

![]()

Play button

![]()

Play button

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

105 Cards in this Set

- Front

- Back

|

Cost that includes both variable costs and fixed costs.

|

Mixed Cost

|

|

|

Minor products of small value that resulted from the manufacture of the main product

|

By–products

|

|

|

Outputs with significant value that cannot be distinguished for each product in the manufacturing process, so common costs must be allocated by some arbitrary means.

|

Joint products

|

|

|

FIFO Equivalent Units

|

Beginning WIP X % to be completed (1–%complete)

+units completed –units in beginning +WIP ending X % completed *Only use ending % complete |

|

|

Weighted Avg Equivalent Units

|

Beginning inventory X % completed

+FIFO equivalent units *Use beginning and ending inventory cost or Completed units +ending inventory X % completed |

|

|

Joint Cost using quantity

|

[Joint Cost

Less NRV of byproduct (end selling price X total qty)] X (quantity of product @ split off/ total of quantity at split off) |

|

|

Prime Cost for DM

|

Beginning DM+purchase+transportation–returns/allowance=materials available

Less end DM =materials used |

|

|

Cost of goods transferred to finished goods (manufactured) COGM

|

WIP beginning+DM (used)+DL+OH applied

=manufacturing incurred less WIP end |

|

|

Calculate COGS

|

Finished goods beginning

+COGM =COG available for sale Less finished goods end |

|

|

Product costing for a sequentially moving manufacturing process. Used when few units are produced and each unit is unique.

|

Job Order Costing

|

|

|

Product costing that averages costs for large homogeneous items.

|

Process Costing

|

|

|

Manufacturing Cost Calculation

|

DM (used) + DL + OH applied

|

|

|

Calculate overhead under/over applied

|

1.Total standard costs / total standard hours = application rate per hour

2. Total actual hours * application rate = budgeted amount 3. Actual – budgeted amount = over/under applied OH |

|

|

Increase in the level of risk results in an increase in management's required rate of return. Higher expected returns to compensation for greater risk.

|

Risk–Averse Behavior

|

|

|

Increase in the level of risk does not result in an increase in management's required rate of return. Seek highest return

|

Risk–Indifferent Behavior

|

|

|

Increase in the level of risk results in a decrease in Management's required rate of return. Willing to settle for lower expected returns as the level of risk increases.

|

Risk–Seeking Behavior

|

|

|

Represents the portion of a single asset's risk that is associated with random causes and can be eliminated through diversification.

|

Diversifiable Risk (nonmarket, unsystematic, or firm specific risk)

|

|

|

Risk that affect all firms and cannot be eliminated through diversification. Ex: war, inflation, High IR, international incidents, and political evens, recessions.

|

Nondiversifiable Risk (market or systematic risk)

|

|

|

Foreign Currency chart of affects

|

Foreign $ Domestic $ Net inflow net outflowDepreciation Appreciation Loss GainAppreciation Depreciation Gain Loss

|

|

|

Cooperation amongst nations to address global issues

|

Functional Interdependence

|

|

|

Global issues, sharing earth. Actions of governments that adversely impact the climate or reduce safety impact all nations.

|

Systemic Interdependence

|

|

|

Requires an acknowledgement of the interdependence of nations and cooperation among nations consistent with shifts in the balance of power.

|

Multipolarity

|

|

|

Examples: U.S. sole economic & military superpower.

|

Unipolar

|

|

|

List prevention Costs

|

1. Training

2. Inspection 3. Preventive maintenance 4. Redesign process/product 5. Search for vendors |

|

|

List Appraisal Costs

|

1. Testing

2. Inspection 3. Maintenance 4. Statistical quality checks |

|

|

List Internal Failure Costs

|

1. Rework

|

|

|

List External Failure Costs

|

1. Warranty costs

2. Cost of returning the good 3. Liability claims – complaints 4. Lost customers –complaints 5. Re–engineering an external failure |

|

|

Define Vertical Linkage Analysis (Value Chain Analysis)

|

Understanding the activities of the suppliers and buyers of the product

|

|

|

Define Internal differentiation Analysis (Value Chain Analysis)

|

Create value through differentiation, benefits are greater than cost.

|

|

|

Perfect (pure) competition attributes

1. control over price and quantity 2. Elasticity 3. Profitability 4. Strategy |

1. Only controls quantity, price set by market

2. Perfectly elastic 3. no profit 4. maintain market share, responsive to market price |

|

|

Monopolistic Competition attributes

1. control over price and quantity 2. Elasticity 3. Profitability 4. Strategy |

1. Controls quantity, primarily relies on market price

2. Highly elastic, adjust quantity w/o effecting price 3. no profit 4. Maintain market share, product diff, allocation of resources |

|

|

Oligopoly attributes

1. control over price and quantity 2. Elasticity 3. Profitability 4. Strategy |

1. Control over price and quantity

2. inelastic, kinked demand curve 3. Positive 4. Maintain or enhance market share, proper spending, adapt to price changes and product volume |

|

|

Monopoly

1. control over price and quantity 2. Elasticity 3. Profitability 4. Strategy |

1. Control over price and quantity

2. Inelastic 3. Positive 4. Ignore market share and focus on profitability from production levels that max profits |

|

|

Supply Chain Operations Reference model process

|

Plan, Source, make, deliver

|

|

|

Workers routinely change jobs or from worker's being temporarily laid off.

|

Frictional Unemployment

|

|

|

Jobs available do not correspond to skills in the workforce or do not live in area where jobs are located. Possible changes in technology is a cause

|

Structural Unemployment

|

|

|

Seasonal changes n the supply and demand of labor.

|

Seasonal Unemployment

|

|

|

Amount of unemployment resulting from declines in real GDP during periods of a recession (contraction).

|

Cyclical Unemployment

|

|

|

Government Purchases of goods and services

Gross private domestic investment (fixed investments & change in inventories Personal consumption expenditures Net exports(exports minus imports) |

Expenditure Approach

|

|

|

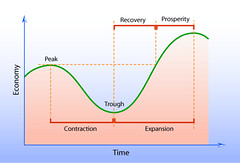

Describe Business cycles

1. Expansionary Phase 2. Peak 3. Contractionary Phase 4. Trough 5. Recovery |

|

|

|

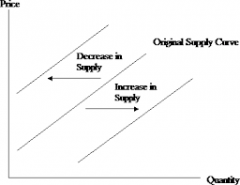

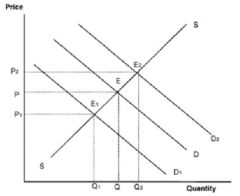

What happens with an increase in demand?

increase in supply? |

|

|

|

What happens with an decrease in demand?

decrease in supply? |

|

|

|

Calculate the Multiplier effect

|

1 1

------------ or ----------- (1–MPC) 1 / MPS |

|

|

Sequence of Events in an AIS (Accounting information System)

|

1. Input sourch documents

2. file source documents 3. Record in journal and posted to GL and sub ledger 4. Trial balances are prepared w/ adj and accruals 5. Financials are generated. |

|

|

Calculate WACC (weighted avg cost of capital)

|

Cost of equity X % of equity

Add: weighted avg cost of debt X % of debt (% of debt = cost of debt x (1–Tax %)) *Lower WACC is better |

|

|

Calculate a payment discount

|

360 discount

------------------------------------- X ------------------------- pay period–discount per 100%–discount % |

|

|

Calculate CAPM (Capital Asset Pricing Model)

|

Risk free rate (krf) + risk premium (PMR)

or krf + (bi x (km–krf)) |

|

|

Calculate degree of financial leverage

|

% Change in EPS

--------------------------- % Change in EBIT |

|

|

Calculate Return on investment

|

Income --------------------------- or avg PP&E + avg Wcinvestment Capital

or Profit margin * Investment turnover Profit margin = income / sales Investment turnover = sales / avg investment |

|

|

Calculate Residual Income

|

Net income – required return

Required return = net book value * hurdle rate |

|

|

Calculate Times Interest earned

|

EBIT/ Total interest Expense

EBIT = Pretax income/ (1–T%) + interest |

|

|

Calculate Net Present Value (NPV)

|

1. After–tax Cash flows: Annual net $ inflow x (1–T%)

2. Add Depreciation benefit 3. X present value of annuity 4. – initial cash outflow |

|

|

Payback Period

|

Net initial investment / increase in annual net after–tax cash flow

*time value of money is ignored |

|

|

Net initial outflow

|

Invoice + shipping+installation

+ increase in working capital –proceeds on sale of old equipment |

|

|

Explain how tax is used in the following NPV calculations: 1. annual depreciation shield

2. Annual savings 3. Salvage Value inflow 4. working capital |

1. Depreciation X Tax %

2. Savings per year X (1–tax%) 3. (salvage value – basis (includes depreciation if not fully depreciated)) x (1–tax%) 4. don't use. |

|

|

Calculate Profitability Index

|

PV of net future cash inflows / present value of net initial investment

or PV FCF – cost today *Greater than 1 means +NPV |

|

|

Balanced Scorecard critical factors(FICA)

|

1. financial

2. internal business processes 3. customer satisfaction 4. advancement of innovation and HR development |

|

|

Strategic Business Unit's 4 financial measures (performance objectives) for managers from lowest to highest (CRPI)

|

1. cost

2. revenue 3. profit 4. investment (return on assets) – independent |

|

|

Flexible budget allow you to adjust which factors?

|

1. production

2. sales |

|

|

The order budgets must be prepared

|

1. Sales

2. Production & SG&A 3. DM , DL, OH 4. COGS 5. Cash (all budgets needed for this) |

|

|

Calculated Efficiency Variance (DL)

|

Step 1: Actual hours X standard rate only

Step 2: Actual units X standard hours x standard rate Step 3: Step 1 – Step 2 = variance (+ unfavorable, –favorable) |

|

|

Costs that are unavoidable because they have already occurred and cannot be recovered. Not a relevant cost.

|

Sunk Costs

|

|

|

The additional costs incurred to produce an additional amount of the unit over the present output.

|

Incremental Costs

|

|

|

Costs that can be authorized at a specific level of management.

|

Controllable Costs

|

|

|

Costs that were authorized at a different level. Not a relevant cost because they cannot be changed.

|

Uncontrollable Costs

|

|

|

Cost for a one–unit increase in activity. These include all variable costs and any avoidable fixed costs associated with decision.

|

Marginal Costs

|

|

|

Cushion, the excess of sales over break even sales. Expressed in $$$ or as a %.

|

Margin of Safety

|

|

|

Calculate Breakeven Sales

|

Fixed costs / (CM / Sales)

|

|

|

Calculate Margin of Safety

& Margin of Safey % |

1. Total sales – Breakeven sales

2. Margin of Safety in $ / Total sales |

|

|

Contribution Margin

Contribution Margin % (ratio) |

1. Break even sales X CM ratio

2. CM/ Total Sales |

|

|

Calculate Stockholder's Equity

|

Total Assets – Liabilities

|

|

|

Calculate Current Ratio

|

Current Assets / Current Liabilities

|

|

|

Calculate Return on Stockholder's Equity

|

Net Income / Stockholder's Equity

|

|

|

Calculate Breakeven point in $$$

|

Total fixed costs / CM ratio

|

|

|

Regression Analysis

|

A method for studying the relationship between 2 or more variables. Predicts the value of dependent variable corresponding to given values of the independent variables (ie fixed cost, variable cost/unit). More accurate than high–low method

|

|

|

Technique used to estimate the fixed and variable portions of cost, usually production costs. Used for flexible/performance budgets

|

High–Low Method

|

|

|

Step–by–step method of projecting costs when learning is a variable, often for repititve task. The rate is a percentage of the decrease in avg time (or total) as production doubles.

|

Learning Curve

|

|

|

Product costing for a sequentially moving manufacturing process. Used when few units are produced and each unit is unique.

|

Job Order Costing

|

|

|

Product costing that averages costs for large homogeneous items.

|

Process Costing

|

|

|

5 Components of COSO (CRIME)

|

1. Control environment

2. Risk Asessment 3. Info. & Comm systems 4. Monitoring 5. Existing Control activities |

|

|

Risk Response (is eaR aim)

|

1. Avoidance

2. Reduction 3. Sharing 4. Acceptance |

|

|

Inherent Risk

|

Risk if management takes NO action

|

|

|

Residual Risk

|

Risk AFTER management takes action to mitigate adverse impacts of an event

|

|

|

Fraud Risk

|

1. Incentive/pressure

2. Rationalization 3. Opportunity |

|

|

Internal Environment

|

1. Risk Appetite

2. Organizational structure 3. Ethics 4. BoD 5. Authority and Responsibility |

|

|

Avoidance (risk response)

|

Avoids or terminates risk (disc ops)

|

|

|

Reduction (risk response)

|

Elect to reduce or mitigate risk (invest in inventory technology or closely monitor inventory)

|

|

|

Sharing (risk response)

|

Reduce risk by transferring (insurance)

|

|

|

Acceptance (risk response)

|

No action in risk response

|

|

|

Monitoring (criMe)

|

1. Ongoing monitoring – controls

2. Separate evaluations – fresh look at controls 3. Reporting deficiencies |

|

|

Code of ethics (internal environment)

|

1. Honest & ethical conduct

2. Full, fair, accurate, and timely disclosures in f/s 3. Compliance with laws, rules & regulations |

|

|

Event Identification Techniques

|

1. Event Inventories – List of potential events common to industry

2. Internal analysis – Analysis performed by staff 3. Escalation or threshold triggers – comparison of predefined criteria may identify events (var from std) |

|

|

Objectives (ERM)

|

1. Strategic – goals, mission, increase s/h value

2. Operations – effectiveness, efficiency & profitability 3. Reporting – reliable 4. Compliance – laws, rules, and regulations |

|

|

The Business Judgement Rule (Fiduciary Duty)

|

Directors must always act in the best interest of the Corporation

|

|

|

Marketing for a single sale – lowest price (used car)

|

Transaction Marketing

|

|

|

Marketing for an ongoing relationship – loyalty

|

Interaction – Based Relationship marketing

|

|

|

Marketing for target markets

|

Database marketing

|

|

|

Marketing with the use of internet

|

E–marketing

|

|

|

Multilevel marketing with focus on relationships and referrals

|

Network marketing

|

|

|

Total Factor Productivity Ratios

|

Output / Total Cost

Material & Labor costs (all inputs) |

|

|

Partial Productivity Ratios

|

Output / Specific Quantity

Material & Labor for specific quantity |

|

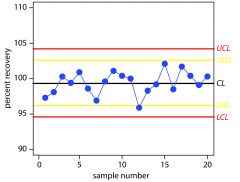

Control Charts

|

Plot comparison of actual results by batch to an acceptable (std) range.

Show trends toward improved quality conformance or deteriorating quality conformance (zero defects). |

|

Pareto Diagrams (Histogram)

|

Shows the frequency of quality issues (defects).

Determines the quality–control issues that are most frequent and often demand the greatest attention. |

|

Cause–and–Effect Diagram (fishbone)

|

Used to identify the sources of problems in process and take corrective action.

|

|

|

Elements on a Cause and Effect Diagram (fishbone)

|

1. Materials

2. Manpower 3. Machinery 4. Method |