![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

70 Cards in this Set

- Front

- Back

|

Production |

The process by which resources are transformed into products or services that are used in other production processes or consumed. |

|

|

What are three important questions to ask for production? |

What to produce? (product-product tradeoffs) How much to produce? (input-product) How to produce? (input-input substitution) |

|

|

What are important decisions to make for production? |

Resources are scarce and frequently costly

Competition forces efficiency and good planning

Profit is necessary for firm survival |

|

|

What are the production-physical relationships? |

Input-input Product-product Input-product |

|

|

How are outputs and inputs measured in Production-physical relationships? |

pounds, tons, bushels, kg., and acres |

|

|

What are the production-input classes? |

Land Labor Management (Entrepreneurship) - Decision making Capital - every manufactured item that can be used in production |

|

|

Fixed Proportions |

We increase all by the same percentage |

|

|

All ________ are increased in the same proportions. |

inputs |

|

|

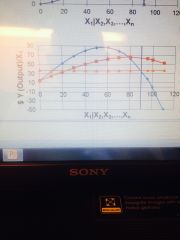

Total Physical Product (TPP) |

|

|

Y = _______ = f (X1 l X2, X3...., Xn) |

TPP |

|

|

TPP or Y ___________ at a(n) ______________ rate, then ______________ at a ______________ rate before it reaches its peak/maximum. |

increases increasing increases decreasing |

|

|

Beyond the peak, TPP may begin to ________ even as X1 continues to _____________. |

decline increase |

|

|

Define Marginal Physical Product (MPP) |

The amount added to TPP when another unit of input is used; the slope of the TPP curve |

|

|

Define the Average Physical Product |

TPP divided by the quantity of input |

|

What is the blue line? What is the red line? |

Blue line = MPP

Red line = APP |

|

|

Where is stage 1 located on an MPP and APP graph? |

Before MPP and APP cross |

|

|

Where is stage 2 located on an MPP and APP graph? |

From when the line of MPP and APP cross until the line of MPP hits zero |

|

|

Where is stage 3 located on an MPP and APP graph? |

Starting when the line of MPP hits zero |

|

|

Define Stage 1 |

APP is increasing throughout, MPP is greater than APP, MPP increases then decreases; irrational

As long as the marginal contribution is greater than the average, add more input |

|

|

Define Stage 2 |

APP is decreasing throughout, MPP is less than APP, MPP goes to zero; rational |

|

|

Define Stage 3 |

MPP is negative; irrational |

|

|

When do you use more of the input? |

If the marginal benefit>marginal cost (in this case the input)

As you use more, the marginal benefit will decrease because MPP will decrease as you use more. |

|

|

When do you use less input? |

If the marginal benefit<marginal cost

As you use less, the marginal benefit will increase because MPP will increase as you use less.

Best decision: marginal benefit = marginal cost |

|

|

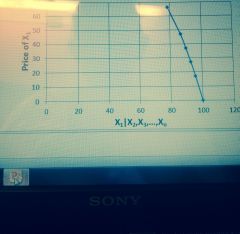

Define Total Value Product (TVP) |

TPP multiplied by the price of the product (output) |

|

|

Define Average Value Product (AVP) |

TVP divided by the number of units of the variable input |

|

|

Define Marginal Value Product (MVP) |

The change in TVP divided by the change in the variable input |

|

|

Define Total Factor Cost (TFC) |

the Variable Input multiplied by the price of the input (factor) |

|

|

Define Marginal Factor Cost (MFC) |

the change in TFC divided by change in the variable input |

|

What does the blue line represent in the top graph? |

TVP |

|

What does the blue line represent? Red line? Orange line? |

MVP AVP MFC |

|

What does this line represent? |

Input demand |

|

|

If we have improved technology and doubled the output for every input level, what will happen to the lines in the graphs? |

Shift upward |

|

|

Use marginal unit of the input until the _____________________ is equal to the Marginal Factor Cost. |

Marginal Value Product

MVP = MFC |

|

|

Aggregate supply |

Profitability Number of firms Risk and government policies |

|

|

Opportunity costs are _________ costs.

Opportunity costs are true ___________________. |

Implicit

costs of production |

|

|

Define Opportunity Cost |

the value of output that could have been obtained from an alternative use |

|

|

Define implicit cost |

opportunity cost that does not involve a money payment or market transaction

Ex: owned land, tractor that is owned |

|

|

Define explicit cost |

cost that involves a money payment and usually a market transaction. Also called out-of-pocket or accounting cost. |

|

|

Define Bookkeeping profit (accounting profit) |

occurs when all operating costs and overhead costs are exceeded by revenues so that a net balance remains |

|

|

Define economic profit |

occurs when revenues exceed the total of all explicit as well as implicit costs. Considers alternative uses of the resources or opportunity costs |

|

|

Define fixed costs |

costs that do not change as the quantity of output changes |

|

|

Define variable costs |

costs that change as the quantity of output changes |

|

|

In the immediate short run, meaning now, all _____________ are fixed. |

resources |

|

|

_________________ is a short run concept. |

Diminishing returns |

|

|

Ultimate long run: all _____________ are variable. |

Resources |

|

|

What is the total revenue equation? |

Price of output * Price of the input |

|

What is A? B? |

A = Profit

B = Loss |

|

|

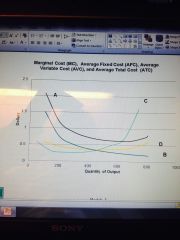

Define marginal cost |

the change in total cost divided by the change in output; the price of the input divided by the MPP |

|

What does A represent? B? C? D? |

A = ATC B = AFC C = MC D = AVC |

|

|

Define marginal revenue |

the change in total revenue divided by the change in output |

|

|

What is the profit in the graph? (What area do you shade?) |

MC vertical to ATC then shade it all the way across |

|

|

What happens if price is below ATC? |

There is no economic profit. |

|

|

When will firms supply goods in the short run? |

If the price is greater than AVC.

The firm's short-run supply curve is Marginal Cost above Average Variable Cost |

|

|

Define Elasticity of supply |

Percentage change in quantity supplied divided by percentage change in price.

Generally positive

Supply can either be elastic (>1) or inelastic (<1) |

|

|

As length of run ___________, supply becomes more ________ because of the ability to change more of the resource base. |

increases elastic |

|

|

Supply shifters (longer run) |

Technology Price of the inputs Number of firms in the industry Change in the price of the output causes movement along the curve (does not shift the whole curve) |

|

|

Define surplus |

If the prices are above equilibrium, quantity supplied will be greater than quantity demanded |

|

|

Define shortage |

If the prices are below equilibrium, quantity demanded will be greater than quantity supplied |

|

|

Bumper crops do what? |

Shift supply to the right |

|

|

Crop failures do what? |

shift supply to the left |

|

|

What does factor-factor substitution look like? |

f (X1, X2 l X3, X4....., Xn) |

|

|

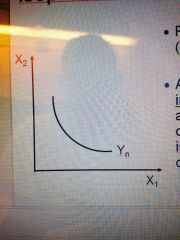

Isoproduct or Isoquant Curve |

Represent levels (amounts) of output, Yn. |

|

What curve is this? |

Isoproduct or Isoquant Curve |

|

As you move from A to D, what happens? |

You substitute factor 1 for factor 2 while producing the same amount of output |

|

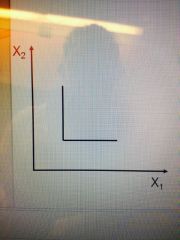

What does a right angle suggest? |

Isoquants at right angles suggest that fixed proportions or zero substitution of one input for the other

Factors 1 and 2 are one fixed combination of two inputs |

|

What does this straight line suggest? |

Isoquants in straight lines suggest perfect substitution of one factor for the other |

|

|

What is the negative of the slope of the isoquant called? |

Marginal rate of substitution (MRS) or the Marginal rate of technical substitution (MRTS)

^positive since the slope is negative |

|

|

Isocost lines |

Show the cost of various input combinations

On each line, the total cost is constant

The slope of the line shows how the market values one input versus the other |

|

|

Define Marginal Rate of Product Substitution |

amount of one product given up to produce another product

calculated as the slope of the production possibilities curve |

|

|

Define expansion path |

shows how output will change as resources change |