![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

54 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

Accounting |

The process of identifying, measuring,and communicating the economic information that permits informed judgements and decisions |

|

|

|

What are the assumptions that an accountants make? |

- economic entity - time period - monetary unit - going concern |

There are four units |

|

|

Economic entity |

An assumption that business financial activities are separated from the companies owners |

Seperation |

|

|

Time period |

The assumption that economic info can be meaningfully captured and communicated over a short period of time |

|

|

|

Monetary unit |

Assumption that the dollar is most effective means to communicate economic activity |

|

|

|

Going concern |

The assumption that the company will continue to operate in the foreseeable future |

|

|

|

Revenue |

An increase in resources resulting from sale of goods and provisions |

INC |

|

|

Revenue Recognition Principle |

a revenue should be recorded when a resource has been earned |

|

|

|

Expense |

a decrease in resources resulting from the sale of goals services |

decrease |

|

|

Matching Principal |

Expenses should be recorded in the period resources used to generate revenue |

|

|

|

How do you find Net Income/Loss |

Revenue - Expense= Net income/loss |

|

|

|

Asset |

An economic resource that is objectively measurable, that results from a transaction. |

will provide future economic benefit |

|

|

Liability |

An obligation of a business that results from a past transaction |

|

|

|

Equity |

The difference between a company's assets, and liability and are shares claimed by the company owners |

|

|

|

Contributed Capital |

The resources that the owner contributes. |

|

|

|

Retained Earnings |

Profits that a company generates |

|

|

|

what should you remember about profits? |

Profits will be the Revenue - Expenses and all that from the income statements will they close out from your return earnings |

|

|

|

Accounting Equations |

Assets = Liabilities + Equity |

Reported at a given time or date |

|

|

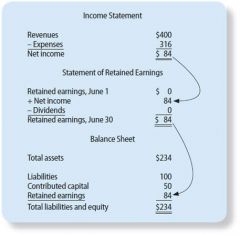

Basic Structure of the statement of retained earnings |

Retained earnings, Beginning Balance +/- Net income/loss - dividends = Retaining earnings, Ending Balance |

|

|

|

Example of the relationship of financial statements |

|

|

|

|

what are the cash flows three different sections? |

-operative activities -investing activities -Financing activities |

The details of cash inflows and outflows for a business that are reported

|

|

|

The basic structure of cashflows statement |

Cash Flows Provided (Used) by Operating Activities (Day to Day op) +/− Cash Flows Provided (Used) by Investing Activities (acquired assets) +/− Cash Flows Provided (Used) by Financing Activities (borrowed money) = Net Increase (Decrease) in Cash |

|

|

|

Understandability |

The ability of accounting info to "be comprehensible to those who have a reasonable understanding of business ... and are willing to study info with reasonable diligence |

|

|

|

Relevance |

The capacity of accounting info to make a difference in decisions |

|

|

|

Reliability |

The extent to which accounting info can be depended upon to represent what it purports to represent, both in description and number. |

|

|

|

Comparability |

The ability to use accounting info to compare or contrast the financial activities of different companies. |

|

|

|

Consistency |

The ability to use accounting info to compare or contrast the financial activities of the same entity over time. |

|

|

|

Materiality |

The threshold at which a financial item begins to affect decision making. |

|

|

|

Conservation |

The manner in which accountants deal with uncertainty regarding economic situations. |

|

|

|

Conceptual Framework of Accounting |

The collection of concepts that guide the manner in which accounting is practiced |

|

|

|

What are the Three Business forms? |

-Sole proprietorship - Partnership - Corporation |

|

|

|

Sole Proprietorship |

A business owned by one person |

an application of economic entity |

|

|

Partnership |

A business that is formed when two or more proprietors join together to own a business |

Spreading the financial risk among many people |

|

|

Corporation |

A separate legal entity that is established by filling articles of incorporation |

|

|

|

Generally accepted accounting principles (GAAP) |

The accounting standards, rules and principles, and procedures that comprise authoritative practice for financial accounting. |

|

|

|

What are the five GAAP most significant regulatory bodies? |

- Securities and Exchange Committee (SEC) - Financial Accounting Standards Board (FASB) -American Institute of Certified Public Accountants (AICPA) - International Accounting Standard Boards (IASB) -International Financial Reporting Standards (IFRS) |

|

|

|

SEC |

The federal agency charged to protect investors and maintain the integrity securities markets |

|

|

|

FASB |

The standard setting body whose mission is " to establish and improve standards of financial accounting and reporting for the guidance and education of the public, including issues, auditors, and users of financial information" |

|

|

|

AICPA |

The professional organization of certified public accountants whose board establishes rules that are often more technical and more specific to certain industries |

|

|

|

IASB |

A board, similar to the FASB, whose mission is to develop a single set of high-quality standards requiring transparent and comparable information. |

|

|

|

IFRS |

Standars issued by the IASB |

|

|

|

Classified balance sheet |

A type of balance sheet that groups together accounts of similar nature and reports them in a few major classifications |

|

|

|

What five main categories are assets classified as? |

Current Assets

Long-term investments Fixed assets Intangible assets Other assets |

|

|

|

Current Assets |

Any asset that is reasonably expected to be converted to cash or consumed within one year of the balance sheet date. |

|

|

|

Long-term Investments |

The investments in the common stock or debt of another entity that will not be sold within a year |

|

|

|

Fixed assets

|

The tangible resources that are used in a company's operation for more than one year and are not intended for resale |

|

|

|

intangible assets |

A resource that is used in operation for more than one a year, is not intended for resale and has no physical substance |

|

|

|

Other Assets |

Resources that do not fit well into one of the other asset classification or are a small enough that they do not warrant separate reporting |

|

|

|

Current Liability |

an obligation that is reasonably expected to be satisfied within one year |

|

|

|

Long-term Liability |

An obligation that is not expected to be satisfied for one year |

|

|

|

Single-step income statement |

Calculates total revenues and total expenses and then determines net income in one step by subtracting total expenses from total revenues |

|

|

|

Multi-step income statement |

Calculates income by grouping certain revenues and expenses together and calculating several subtotals of income |

|

|

|

Gross Profit |

The profit that a company generates when considering only the sales price and the cost of the product sold |

|

|

|

Operating profit |

The profit that a company generates when considering both the cost of then inventory and the normal expenses incurred to operate the business |

|