![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

44 Cards in this Set

- Front

- Back

|

CIA MfAD

|

CIA MfAD

|

|

|

MfAD

|

Reflects the degree of uncertainty of the best estimate assumption

|

|

|

Reasons for deviation of actual from expected experience (3)

|

a. Favorable or adverse error of estimation.

b. Unexpected deterioration or improvement of expected experience as a result from unanticipated events. c. Favorable or adverse statistical fluctuation |

|

|

Desirable characteristics of a risk margin (4)

|

1) The less that is known about the current estimate and its trend, the higher the risk margin should be

2) Higher for low-frequency and high-severity lines 3) Higher for long-term contracts 4) Higher for wider probability distributions |

|

|

Risk Margin - Method should (4)

|

a. Applied consistently over the lifetime of a contract

b. Be easy to calculate c. Be consistently determined for different time periods for the same entity d. Be consistently determined between entities at each reporting date |

|

|

Claims development

|

2.5% to 20%

|

|

|

Recovery from Reinsurance

|

0% - 15%

|

|

|

Investment Return Rate

|

25 bp to 200 bp

|

|

|

Situations where appropriate to use high margins

|

- Reinsurer financial distress resulting in risk of not recovering ceded claim

- Hyperinflation causing steep increases in the cost of claims - New line of business / Lack of data to use for reserving - Change in tort system / regulatory regime affecting future claims - Economic recession / volatile financial market causing high investment return risk - A significant degree of uncertainty in the assumptions used |

|

|

Risk in margin for IRR (3)

|

Types of risks addressed

a. Mismatch between claim payments and availability of liquidity of assets b. Error in estimating claim payment patterns of future claims c. Asset risk 1) Credit/default risk 2) Liquidity risk |

|

|

Weighted Formula (MfAD)

|

|

|

|

Explicit quantification of 3 margins

|

Asset/Liability Mismatch Risk Margin + Time Risk Margin + Credit Risk Margin |

|

|

Asset/Liability mismatch

|

|

|

|

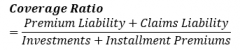

Coverage Ratio

|

|

|

|

Interest Rate Movement |

|

|

|

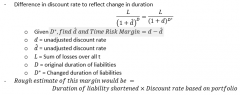

Timing Risk

|

|

|

|

Credit Risk

|

Yield on corporate bond - yield on risk-free bond |

|

|

Quantile approaches (3)

|

- Multiple of standard deviation

- Percentile level / Confidence level / Value at risk (VaR) - Conditional Tail Expectation (CTE) / Tail Value at risk (TVaR) |

|

|

Practical issues quantile approaches (3)

|

1. Selection of confidence level or CTE level -no theory or practice yet developed

2. Different confidence levels for different products or during claims runoff 3. Sources of risk distributions and treatment of extreme events |

|

|

High margin for claims development (6)

|

1. Considerations related to claims management

o Significant changes in systems affecting claims handling o Lack of consistent claims management leadership and personnel o Significant change in the relative adequacy of case outstanding 2. Considerations related to underwriting o Significant changes in systems affecting underwriting o Inconsistent underwriting leadership and personnel o Inadequate staff 3. Considerations related to other operations o Significant changes in consistent technology and processing systems o Absence of or significant changes in internal controls o Significant changes in accounting systems 4. Considerations related to data o Significant changes in loss and premium volumes by period o Lack of credible historical experience for new exposures o Significant changes in the mix of business 5. Considerations related to lines of business o Unstable legislative, judicial, and government environment o Long tail o High liability exposure 6. Change in high margin allowed from 15% to 20% in situations where: - Automobile insurance undergoing tort reforms - Introduction of a new line or operations where data is limited - Significant retention changes where data is limited for estimating the effects - Economic upheaval with effect on long-tail lines - Not expected that such will shift all current margins upward |

|

|

High margin for reinsurance ceded (4)

|

- Characteristics of high-margin situations

o significant unregistered reinsurance o high ceded loss ratio o high ceded commission rate o significant reinsurers with weak financial condition |

|

|

High margin for investment return rates (4)

|

o Significant mismatch of flows between assets and liabilities

o Significant variability in claim payment pattern o High asset default risk o Long claim settlement period |

|

|

IFRS 4

|

IFRS 4

|

|

|

Reasons for issuing IFRS 4 (2)

|

a. to make limited improvements to accounting for insurance contracts until the Board completes phase II of its project on insurance contracts.

b. to require any entity issuing insurance contracts (an insurer) to disclose information about those contracts. |

|

|

Primary requirements IFRS 4 (2)

|

a. limited improvements to accounting by insurers for insurance contracts.

b. disclosure of the amounts in an insurer's financial statements arising from insurance contracts and helps users of those financial statements understand the amount, timing and uncertainty of future cash flows from insurance contracts. |

|

|

Liabilities adequacy test

|

An insurer shall assess at the end of each reporting period whether its recognized insurance liabilities are adequate, using estimates of future cash flows. If those insurance liabilities are inadequate, the entire deficiency shall be recognized in profit or loss.

|

|

|

Changes in accounting policies

|

An insurer may change its accounting policies for insurance contracts if, and only if, the change makes the financial statements more relevant to the economic decision-making needs of users and no less reliable, or more reliable and no less relevant to those needs. An insurer shall judge relevance and reliability by the criteria in IAS 8.

|

|

|

Insurance contract

|

A contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder.

|

|

|

Reinsurance contract

|

An insurance contract issued by one insurer (the reinsurer) to compensate another insurer (the cedant) for losses on one or more contracts issued by the cedant.

|

|

|

Discretionary participation feature

|

A contractual right to receive, as a supplement to guaranteed benefits, additional benefits.

|

|

|

At least one of following must be uncertain for it to be insurance contract (3)

|

a. whether an insured event will occur;

b. when it will occur; or c. how much the insurer will need to pay if it occurs. |

|

|

KPMG Solvency II

|

KPMG Solvency II

|

|

|

Goals of Solvency II (4)

|

a. Alignment of economic and regulatory capital including giving appropriate recognition to diversification benefits within companies and between subsidiaries.

b. Freedom for companies to choose their own risk profile and match it with an appropriate level of capital c. An early warning system for deterioration in solvency by active capital management d. By better aligning risk and capital management, encouraging an improvement in the identification of risks and their mitigation |

|

|

Three pillars of Solvency II (3) |

Pillar 1: quantitative requirements a. It aims to ensure firms are adequately capitalized with risk-based capital. B. Standard Formula approach or an internal model approach.

Pillar 2: Quantitative requirements: a. Imposes higher standards of risk management and governance on an insurer.

Pillar 3: Disclosure requirements a. aims for greater levels of transparency for supervisors and the public. b. Increases the level of disclosure through internal reports and reports to regulators. |

|

|

Benefit of Solvency II (3)

|

1) It will level the playing field by ensuring consistent regulation in all territories.

2) It should also improve the solvency of the industry and that means better protection for consumers. 3) It promises benefits of better capital management by aligning solvency with the risk profile of each firm. |

|

|

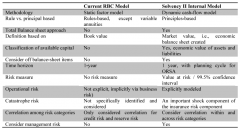

Compare US and EU (4)

|

|

|

|

Blanchard & Klann

|

Blanchard & Klann

|

|

|

Principal functions of reinsurance (4) |

1. Increase large-line capacity - company wants to limit its exposure per policy but portions of market demand greater coverage E.g. Prorata reinsurance treaty above 500k 2. Provide catastrophe protection -company desires to reduce its potential loss from a catastrophic event E.g. Reinsurance for loses in excess of 10% of gross premium 3. Stabilize loss experience a. Loss experience experiences annual fluctuations greater than management desires b. Motivated by demands of capital providers or its own desire to simplify capital management E.g. Excess of loss treaty (90% of losses above loss ratio of 100%) 4. Provide surplus relief -reduce net leverage ratios to a desirable level E.g. Quota share 5. Facilitate withdrawal from a market segment E.g. Prospective reinsurance to cede unearned premium and future losses 6. Provide underwriting guidance |

|

|

Increase large-line capacity - impact on surplus/loss reserves/unearned premium/leverage ratio/income statement

|

a. Surplus

i. No impact other than on earnings from additional business opportunities ii. Ceding company may decide or be required to hold more surplus b. Loss reserves -both gross and net reserves increase c. Unearned premiums -increase but in proportion to premium increase d. Leverage ratios- Net ratios increase slightly

e. Income statement i. Little changed on a net basis ii. Riskier book and cost of reinsurance may introduce greater volatility |

|

|

Provide catastrophe protection - impact on surplus/loss reserves/unearned premium/leverage ratio/income statement

|

a. Surplus

i. If no catastrophe occurs, surplus decreased because of its cost ii. But if catastrophe occurs, surplus decreases stongly b. Loss reserves i. No impact on net reserves unless covered event occurs ii. If catastrophe occurs, gross reserves can increase significantly for the payout period of the catastrophe c. Unearned premiums i. Little or no change as reinsurance is a small portion of total premium d. Leverage ratios i. If no catastrophe, increases ii. If catastrophe occurs without reinsurance, strong increase in gross and net ratios iii. If catastrophe occurs with reinsurance, strong increase in gross ratios e. Income statement - Reduced |

|

|

Stabilize loss experience - impact on surplus/loss reserves/unearned premium/leverage ratio/income statement

|

a. Surplus - lowered by net cost of reinsurance

b. Loss reserves i. Gross reserves reflect full volatility of the annual results ii. Net reserves should be smaller, more stable, and could be easier to estimate c. Unearned premiums -reduced, unless reinsurance is purchased with a single effective date and the accounting date coincides with the reinsurance expiration date d. Leverage ratios - more stable but slightly higher because of reduced surplus e. Income statement i. Lower results over time because of net cost of reinsurance and lower investment income ii. Year-to-year results should be more stable |

|

|

Provide surplus relief - impact on surplus/loss reserves/unearned premium/leverage ratio/income statement

|

a. Surplus

i. Reduction of assets equals reduction of liabilities plus net underwriting cost of reinsurance ii. Quota share can only increase surplus if business is written at a loss b. Loss reserves -net reserves are a fixed percentage of gross reserves c. Unearned premiums -net reserves are a fixed percentage of gross reserves d. Leverage ratios i. Net leverage ratios are significantly improved ii. Ceded reinsurance leverage ratios are significantly increased e. Income statement -underwriting income is cut by the quota share amount and investment income is reduced |

|

|

Facilitate withdrawal from a market segment - impact on surplus/loss reserves/unearned premium/leverage ratio/income statement

|

a. Surplus

i. Slight reduction for assumed profitable business b. Loss reserves i. Gross reserves are unchanged ii. Net reserves and their volatility eliminated c. Unearned premiums i. Gross reserves run-off over the year ii. Net reserves eliminated d. Leverage ratios -net leverage ratios are zero e. Income statement i. Underwriting profit since ceding commission offsets expenses that were paid the previous year |

|

|

Provide underwriting guidance - impact on surplus/loss reserves/unearned premium/leverage ratio/income statement

|

a. Conceptually equivalent to the situation involving increased large line capacity

b. Impact on surplus and income depends on profitability and volume (after cessions) of the new business |