![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

40 Cards in this Set

- Front

- Back

|

Scarcity Principle |

Although we have boundless needs and wants, the resources available to us are limited. Often, having one good means less of another. |

|

|

Total Cost |

= Implicit + Explicit Costs Implicit: Intangible costs like time |

|

|

Opportunity Cost |

Cost including value of highest valued alternative that must be given up |

|

|

Cost - Benefit Principle |

A person/group should take an action if, and only if, the extra benefits from taking the action are at least as great as the extra cost |

|

|

Diminishing Marginal Benefit |

Every successive unit gives you less value/pleasure. The benefit of eating a 2nd slice of pizza is not a good as eating the 1st. |

|

|

Marginal Benefit |

(MB) The amount of benefit you receive by creating one more unit. Additional units are only worth so little to you after you already have what is needed. The slope of a total benefit curve (or the derivative). The greater the slope , the greater the marginal benefit of the product. |

|

|

Value at which you cease consumption |

MB equal to MC

Consume no further, as long as MB is greater than or equal to MC consumption benefits you |

|

|

Production Possibilities Frontier (PPF) |

Closely associated with comparative advantage. Deals with who should produce a certain object and trade with someone else because it is mutually beneficial for both parties to produce what is least costly to them and trade. |

|

|

Income's Effect on Supply/Demand |

As price goes down/the income of the consumer goes up, the greater the purchase power of the consumer leading to rise in quantity demanded |

|

|

Substitution's Effect on Supply/Demand |

As price goes up/competitive replacements for a product are offered, the consumer purchases more substitutes for that product and quantity demanded decreases |

|

|

Equilibrium |

The supplier has no more product that he is looking to sell and the consumer is not looking to buy any more |

|

|

Substitute |

A good that can replace another |

|

|

Compliment |

A good that goes well with another (ex. cream cheese and bagels) |

|

|

Rising Income's Effect on Normal Goods |

Income increases = Demand for normal goods increases |

|

|

Rising Income's Effect on Inferior Goods |

Income increases = Demand for inferior goods decreases

As purchase power increases you will buy the superior product. |

|

|

Demand Shifters (Consumer) |

1. Substitutes / Compliments 2. Income 3. Performance of the product (consumer's happiness with it) 4. Number of buyers 5. Expectation of future price (as it decreases, demand increases) |

|

|

Demand Shifters (Producer) |

1. The price or availability of ingredients or inputs 2. Taxes (taxes increase, production cost increases = higher reservation price of the product for the producer 3. Technology (as tech. increases/improves, production of the goods is more effective) 4. Number of suppliers |

|

|

Inputs |

Ingredients or resources like payroll of employees, actual ingredients, or bills that go into creating a product |

|

|

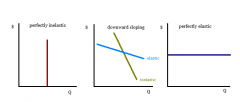

Elasticity |

Observes how consumers react to changes in prices and availability of substitutes. The more consumers react to price change the more elastic the good is. |

|

|

Determinants of Elasticity |

1. Availability of substitutes (if you need surgery, your demands are highly inelastic, there are no more effective substitutes to it) 2. Budget Share (smaller goods like salt are inelastic because you couldn't care less but a new car is elastic because its a big share of your budget) 3. Time (the more time a consumer has to work with, the more elastic the good will be because they can wait for a substitute or change in price) |

|

|

Elasticity Equation |

Ed = (price/quantity) x (1/slope) - Slope = change in Price/change in Quantity Ed = %change of demand / %change of price

X is less than 1, Inelastic x is equal to 1, Unit Elasticity (equilibrium) x is greater than 1, Elastic |

|

|

Income Elasticity Equation |

= %change in demand / %change in income

X is greater than 0 for normal goods X is less than 0 for inferior goods |

|

|

Determinants for Elasticity of Supply |

1. Flexibility/Mobility of Inputs (how specialized inputs like equipment and labor force are for the product) 2. Time (the longer a person has to work with the more elastic the product because they can wait for substitutes or a drop in input prices) |

|

|

Competitive Markets |

Markets where the product is exactly the same across all producers (ex. crops like corn), there are a large number of suppliers, there is easy entry and exit in/out of the market (ex. hot dog vendors), and there are well informed supplies and consumers.

Market determines price for suppliers. |

|

|

Accounting Profit |

= Total Revenue - Explicit Costs |

|

|

Economic Profit |

= Total Revenue - Total Cost (implicit/explicit) |

|

|

Short Run |

One or more inputs is fixed |

|

|

Long Run |

All inputs are variables and firms can exit/enter the market |

|

|

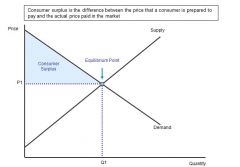

Consumer Surplus |

= Reservation Price - Actual Price

.5(base x height) |

|

|

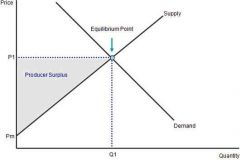

Producer Surplus |

= Actual Price - Reservation Price

.5(base x height) |

|

|

Reservation Price |

Max price that a consumer will pay for a good the lowest a producer is willing to sell the product for |

|

|

External Cost |

A cost of an activity that falls on ppl other than those who pursue the activity (ex. pollution) |

|

|

External Benefit |

A benefit received by ppl other than those who originally pursued the action that caused it |

|

|

Social Benefit or Cost |

= Private benefit or cost + External benefit or cost |

|

|

Coase Theroem |

When the parties affected by externalities can negotiate "costlessly" w/ one another, an efficient outcome results no matter how the law assigns responsibility for the charges |

|

|

Socially Beneficial |

When MB = MC, Equilibrium |

|

|

Oligopoly |

Small number of firms running a single market like a monopoly |

|

|

Dominant Strategy |

Regardless of whatever other firms do to effect price, what is your firm's best response to their production? |

|

|

Nash Equilibrium |

A combination of strategies such that no players have an incentive to change their strategy given the strategies of their opponents |

|

|

Search Models |

Consumers must decide how much time/$/effort to exert in acquiring info about product characteristics like quality, price, etc. |