![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

10 Cards in this Set

- Front

- Back

|

What is raw material |

Goods purchased for incorporation into product for sale |

|

|

When direct material can be treated as indirect material cost |

Sometimes small quantities of direct material used in the product like gums and threads are used in binding book may be categorized as indirect material cost |

|

|

What is inventory

|

Inventory as tangible property held.finished good WIP RAW MATERIAL |

|

|

Need for inventory control |

So that man and machine don't have wait. help in controlling the production cost. To reduce purchasing and storing cost without affecting production or sale. to keep the size of inventory optimum. To reduce excessive consumption and wastage |

|

|

Dormant/non moving stock |

Items which are not moving temporarily but their movement expect shortly |

|

|

Slow moving stock |

Items which are moving at slow rate |

|

|

Feature of material cost control |

1. Optomise the cost and quality of raw material 2.timely procurement and avoid urgent purchase 3.over stockings should be avoided 4.wastage and looses should be avoided at every stage of operation 5.material should be classified and accounted |

|

|

Purchase and store routine |

1.material inspection note 2. Material transfer note 3. Bill of material 4.purchase requisition 5. Bin card 6.store ledger |

|

|

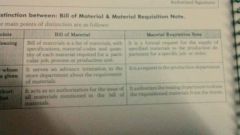

Bill of material vs material requisition note |

|

|

|

Bin card vs ledger |

|