![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

15 Cards in this Set

- Front

- Back

|

What is a portfolio weight? |

The fraction of the total investment in the portfolio held by each individual investment in the portfolio |

|

|

How do we calculate the return on a portfolio? |

Sum the returns of the individual stocks x their portfolio weights |

|

|

What does correlation measure? |

Measures the strength of the relationship between two stocks. It is a barometer of the degree to which the returns share common risks and tend to move together. |

|

|

What is covariance? |

Covariance is the expected product of the deviations of two returns from their means. +ve and -ve covariance determines how the returns move together. |

|

|

What is short selling? |

The selling of a stock that the seller doesn't own (but promises to deliver): broker lends seller the stock; stock's proceeds are credited in seller's account; at some point, seller must "close" the short by buying back the same number of shares and returning them to broker. |

|

|

How can short selling increase a portfolio’s expected return? |

If you sell a low return stock short and spend the money on a high return stock then you increase your expected returns. Of course, you also increase the level of risk which you assume. |

|

|

How does the volatility of an equally weighted portfolio change as more stocks are added to it? |

The volatility declines as the number of stocks in the portfolio increases. This is a result of diversification. |

|

|

How does the volatility of a portfolio compare with the weighted average volatility of the stocks within it? |

The volatility of a portfolio is less than the weighted average volatility of the individual stocks within the portfolio. This is a result of diversification. Note: The expected return of a portfolio is equal to the weighted average expected return. |

|

|

How does the correlation between two stocks affect the risk and return of portfolios that combine them? |

Correlation: - has no effect on the expected return of a portfolio - however it does effect the volatility of the portfolio |

|

|

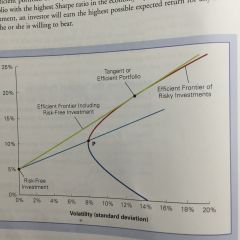

Tangent portfolio |

The portfolio that provides the biggest reward per unit of volatility of any portfolio available. It is the efficient portfolio. |

|

|

If investors are holding optimal portfolios, how will the portfolios of a conservative and an aggressive investor differ? |

The two investors differ how much each invests in the tangent portfolio versus the risk-free portfolio. |

|

|

What is the capital market line (CML)? |

When the tangent line goes through the market portfolio (= efficient portfolio), that is the capital market line. According to CAPM, all investors should choose a portfolio on the capital market line by holding some combination of the risk-free security and the market portfolio. |

|

|

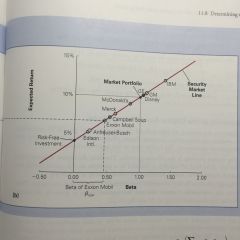

What is the security market line (SML)? |

The line along which all individual securities should lie when plotted according to their expected return and beta. Risk-free investment (beta = 0); market (beta = 1) |

|

|

According to CAPM, how can we determine a stock's expected return? |

Recall Expected Return of a portfolio is the expected return of the securities in the portfolio. The Beta of a portfolio is the weighted average of the individual investment betas in the portfolio |

|

|

What is Capital Asset Pricing Model (CAPM)? |

Method for estimating the cost of capital CoC = Risk-free rate + Beta * Market premium |