![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

165 Cards in this Set

- Front

- Back

|

Economics |

the study of how individuals, institutions, and society make optimal choices under conditions of scarcity

|

|

|

Scarcity |

wants/needs exceed available resources |

|

|

Wants |

goods/services that people would like to have |

|

|

Needs |

things needed to live- food, shelter, clothing |

|

|

Factors of Production |

productive resources |

|

|

Land |

the earth and all resources from it. land, forests, water resources, oil |

|

|

Labor |

efforts and abilities of humans used to produce goods. schools, teachers, janitors |

|

|

Capital |

tools, equipment, and facilities to produce good. hammers, nails, saws |

|

|

Entrepreneurship |

when an individual who organizes resources for production and distribution |

|

|

WIRP |

Wages for labor. Interest for capital. Rent for land. Profit for entrepreneurship |

|

|

Trade-Off |

Giving up one item or category for another |

|

|

Opportunity Cost |

the item or value lost when making an economic decision |

|

|

Marginal Benefit |

satisfaction of adding one unit in production or consumption |

|

|

Marginal Cost |

the desired good's cost |

|

|

Diminishing Marginal Utility |

decreasing satisfaction or usefulness as additional units of a product are acquired |

|

|

Production Possibility Curve |

Point X- inefficient Point A,B,C- efficient Point Y- unattainable |

|

|

Specialization |

doing a specific task in the production of goods/services |

|

|

Division of Labor |

breaking productive tasks into smaller and more specialized act (assembly line) |

|

|

Voluntary Exchange |

when individuals and businesses freely choose to exchange goods, services, and resource for something else of value |

|

|

3 Basic Economic Questions |

1. What will be produced? 2. How will it be produced? 3. For whom will it be produced? |

|

|

Market Economy |

producers and consumers make economic decisions and the factors of production are privately owned (Capitalism) |

|

|

Consumer Sovereignty |

the idea that individuals are the best judge of their needs and what is in their best interest and that they indicate their choices by their spending decision |

|

|

Command Economy |

the central authority or government, makes most of the economic decisions |

|

|

Mixed Economy |

An economy which has the characteristics of a market economy with some government intervention and regulation |

|

|

Laissez Faire |

a policy or attitude of letting things take their own course, without interfering |

|

|

Traditional Economy |

Economic activity stems from the rituals, habits or customs |

|

|

Public Goods |

items such as schools, defense, police and fire protection, parks roads and street lighting provided by government |

|

|

Goods |

items that companies/individuals produce to sell (cars, toys) |

|

|

Services |

activities/assistance provided by people (builders, chiropractors) |

|

|

Private Goods |

a product that must be purchased to be consumed, and its consumption by one individual prevents another individual from consuming it |

|

|

Redistribution of Income |

healthcare, social security |

|

|

Private Property Rights |

people have the right to control their possessions as they see fit |

|

|

Tariffs |

a tax or duty to be paid on a particular class of imports or exports |

|

|

Subsidies |

a sum of money granted by the government or a public body to assist an industry or business so that the price of a commodity or service may remain low or competitive |

|

|

Deregulations |

taking away rules or laws on an industry such as deregulation of transportation |

|

|

Inputs |

what is used in the production process to produce output |

|

|

Outputs |

finished goods and services |

|

|

Fixed Costs |

business costs, such as rent, that are constant whatever the quantity of goods or services produced |

|

|

Variable Costs |

a cost that varies with the level of output |

|

|

Total Costs |

total economic cost of production |

|

|

Capital Investment |

funds invested in a firm or enterprise for the purpose of furthering its business objectives |

|

|

Capital Goods

|

goods that are used in producing other goods, rather than being bought by consumers |

|

|

Human Capital

|

the skills, knowledge, and experience possessed by an individual or population, viewed in terms of their value or cost to an organization or country |

|

|

Standard of Living |

is the rough estimate of the quality of life that people in a country are able to afford |

|

|

Incentive |

positive and negative rewards that encourage economic behavior such as making purchases or working to increase productivity |

|

|

Commercial Banks |

a bank that offers services to the general public and to companies |

|

|

Interest Charged |

interest the bank charges people or business to borrow money (personal and business loans) |

|

|

Interest Earned |

interest the bank pays people or business for the use of their money (Money in savings accounts) |

|

|

Credit Union |

A credit union provides services similar to a bank; the difference is that a credit union only provides these services to its members, and these members own and control the institution |

|

|

Return vs Risk |

invested money can render higher profits only if the investor is willing to accept the possibility of losses |

|

|

Stocks |

Types of securities representing ownership in a corporation

|

|

|

Bonds |

loaning the government a sum of money in return for interest earned and the original loan |

|

|

Mutual Funds |

A professionally managed, DIVERSIFIED investment that enable investors to pool money with other investors

|

|

|

Reasons People Save and Invest |

to have money for emergencies or for retirement |

|

|

Progressive Tax |

a tax that imposes a higher percentage of taxation of persons with high incomes than on those with lower incomes, hurts the rich |

|

|

Regressive Tax |

a tax that imposes a higher percentage rate of taxation on low incomes than on higher incomes, hurts the poor |

|

|

Proportional Tax |

the tax rate does not change with respect to changes in income |

|

|

Credit |

borrowed money |

|

|

Interest |

the amount of money that a lender charges a borrower in exchange for the use of their money |

|

|

Simple Interest |

applied only to the value of the principal. interest grows slowly |

|

|

Compound Interest |

is interest applied to both the principal and the interest. (you pay interest on interest, grows fast) |

|

|

Principal |

amount borrowed or the amount still owed on a loan |

|

|

Debt |

the state of owing money |

|

|

Credit Worthiness |

valuation performed by lenders that determines the possibility a borrower may default on his debt obligations |

|

|

Insurance |

government agency provides a guarantee of compensation for specified loss, damage, illness, or death in return for payment of a premium |

|

|

Comprehensive Liability |

protects the organization from liability claims |

|

|

Deductibles |

specified amount of money that the insured must pay before an insurance company will pay a claim |

|

|

Premiums |

amount to be paid for an insurance policy |

|

|

Shared Liability |

allows more than one person or party to share the risk |

|

|

Medium of Exchange |

Anything that is generally acceptable in exchange for goods and services |

|

|

Measure of Value |

Common measurement in which values are expressed |

|

|

Store of Value |

an item that maintains value over time |

|

|

Sole Proprietorships Advantages |

All decision making power belongs to owner and they are easy to start |

|

|

Sole Proprietorships Disadvantages |

Owner faces unlimited liability(owner is responsible for loses or debt), hard to raise money and limited life(business dies with owner) |

|

|

Partnership Advantages |

Specialization of owners |

|

|

Partnership Disadvantages |

Partners face unlimited liability, decision making can be complex, owners share profits and costs |

|

|

Corporation Advantages |

Owners have limited liability (not responsible for loses and debt), have long life spans, and easy to raise money for business |

|

|

Corporation Disadvantages |

Double taxation (profits that the company make are taxed twice) and corporations are hard to start |

|

|

Microeconomics |

The study of how economic actors (individuals and businesses) make decisions and are impacted by the allocation(distribution) resources |

|

|

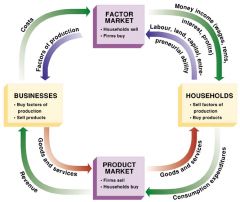

Factor Market |

where inputs such as land, labor, capital, and other resources are exchanged |

|

|

Product Market |

where households buy finished goods and where businesses sell finished goods |

|

|

Economic Independence |

the reliance on business/households to provide the goods and services that people consume |

|

|

The Circular Flow Chart |

|

|

|

Law of Demand |

the quantity demanded varies inversely with price. Price Increases(P↑) then Quantity Decreases(Q↓) or Price Decrease(P↓) then Quantity Increases(Q↑) |

|

|

Change in Quantity Demanded |

movement along the demand curve due to a change in price |

|

|

CD or Change in Demand |

when the whole curve shifts |

|

|

CD Consumer Income |

if consumer income increases he or she can buy more of a product |

|

|

CD Consumer Tastes |

consumers buy more products when they are advertised |

|

|

CD Substitutes |

goods that can be purchased to replace a similar good |

|

|

CD Compliments |

goods that are normally purchased with other goods |

|

|

CD Change in Expectations |

The way consumers think about the future will affect the demand for a good |

|

|

CD Number of Consumers |

As population increases, more consumers are buying more products |

|

|

Law of Supply |

the quantity supplied varies proportionately with price.Price Increases(P↑) then Quantity Increases(Q↑) or Price Decrease(P↓) then Quantity Decreases(Q↓) |

|

|

Change in Quantity Supplied |

movement along a supply curve; caused only by a change in a good’s own price |

|

|

CS or Change in Supply |

a shift in the entire supply curve caused by a change in non-price determinants of supply |

|

|

CS Input Prices |

If the cost of producing a product goes up, then the supply of the product will go down |

|

|

CS Technology |

changes in producer’s technology can change the current supply of a product |

|

|

CS Expectations |

what people expect |

|

|

CS Taxes |

how much tax is on every product |

|

|

CS Number of Sellers |

changes in the number of sellers in a market can change the current supply of product |

|

|

Equilibrium |

the place where the quantity supplied equals the quantity demanded |

|

|

Shortage |

Wants/Needs exceed supply |

|

|

Surplus |

an excess of production or supply over demand |

|

|

Elasticity |

measures the sensitivity between two economic variables |

|

|

Price Elasticity of Demand |

a change in price has a relatively large effect on quantity demanded |

|

|

Price Inelasticity of Demand |

a change in price has relatively little effect on quantity demanded |

|

|

Price Ceiling |

when government creates a maximum price at which a good can be sold |

|

|

Price Floor |

when governments set a minimum price for which a product can be sold |

|

|

Perfect Competition |

buyers and sellers are so numerous and well informed that all elements of monopoly are absent and the market price of a commodity is beyond the control of individual buyers and sellers |

|

|

Monopolostic |

Number of Firms:a large number Barriers to Enter the Market:low, easy to enter Products:products are similar, but not exactly alike. Competition: firms must remain aware of their competitor’s action, but they do have some control over their own prices Advertisement:much Example: Airline companies, blue jean companies |

|

|

Oligopoly |

market is shared by a small number of sellers and producers |

|

|

Monopoly |

market is controlled by one |

|

|

Macroeconomics |

the study of the economics of a nation as a whole |

|

|

Gross Domestic Product |

the market value of all goods and services produced by a country over a specific period of time, usually a year |

|

|

Net Exports |

total amount of exports |

|

|

GDP per Capita |

dollar amount of GDP produced on a per- person basis |

|

|

Consumer Price Index |

takes a hypothetical basket of goods and services purchased by a typical household. It then tracks changes in the amount of money required to purchase this same basket of goods and services year after yea |

|

|

Inflation |

rise in overall prices in an economy |

|

|

Deflation |

fall in overall prices in an economy |

|

|

Stagflation |

rise in overall prices and unemployment rate in an economy |

|

|

Who benefits form inflation |

borrowers and people who barter |

|

|

Who loses with inflation |

savers, lenders, people who live on fixed incomes, people with long-term contracts |

|

|

Labor force |

all the members of a particular organization or population who are able to work, viewed collectively |

|

|

Frictional Unemployment |

unemployment due to people leaving a job and looking for one that better fits their interests and abilities. |

|

|

Structural Unemployment |

unemployment occurs when you have job skill that no one wants, or when a company wants to hire somebody but can’t find anyone who has the necessary requirements |

|

|

Cyclical Unemployment |

people who are laid off as a result of a contracting economy |

|

|

Seasonal Unemployment |

regular seasonal changes in unemployment |

|

|

Natural Rate of Unemployment |

5% in the U.S. |

|

|

National Debt |

if a government continues to operate a deficit more than 1 year |

|

|

National Deficit |

when a country spends more money than it takes in with taxes, in a year |

|

|

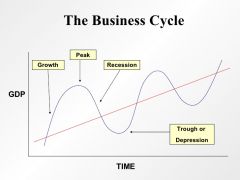

Business Cycle |

|

|

|

Recession |

a decline that lasts at least 6 months |

|

|

Depression |

he lowest point at the end of a recession and before a recovery |

|

|

Aggregate Supply |

the supply of all goods and services within a country |

|

|

Aggregate Demand |

the demand for all goods and services within a country |

|

|

Monetary Policy |

:refers to changes in the money supply of a nation in order to influence its economy |

|

|

Federal Reserve |

is the bank of banks or the bank of last resorts. |

|

|

Reserve Requirement Ratio |

portion of depositors' balances that banks must have on hand as cash |

|

|

Discount Rate |

the minimum interest rate set by the Federal Reserve for lending to other banks |

|

|

Open Market Operations |

If the Fed wanted to stimulate the economy to reduce unemployment it could buy securities on the open market |

|

|

Fiscal Policy |

the use of government expenditures (spending)and revenue collection (taxes)toinfluence the national economy, specifically GDP |

|

|

Imports |

are those goods that a nation buys from other countries |

|

|

Exports |

are goods that a nation sells to other countries. |

|

|

Absolute Advantage |

when a country can produce more of a good than another country. |

|

|

Comparative Advantage |

when a country can produce a product at a lower opportunity cost than another country. |

|

|

Quotas |

a limited quantity of a particular product that under official controls can be produced, exported, or imported |

|

|

Embargoes |

when government prohibits the import of a good |

|

|

Standards |

governments employ standards to ensure the safety of imported goods and to make sure these goods comply with local laws |

|

|

Protectionism |

when governments protects its’ country’s industries from foreign competition |

|

|

Free-Trades |

international trade without government restrictions |

|

|

North American Trade Agreement |

eliminates trade barriers between Canada, Mexico and the United States |

|

|

World Trade Organization |

makes the rules for trade between nations |

|

|

European Union |

eliminates trade barriers between European countries such as France, Germany, Spain and Italy |

|

|

United Nations |

international organization formed in 1945 to increase political and economic cooperation among member countries. The organization works on economic and social development programs, improving human rights and reducing global conflicts |

|

|

Association of Southeast Asian Nations |

eliminates trade barriers between Southeast Asian Countries such as Vietnam, Thailand, Singapore, Indonesia and the Philippines |

|

|

Favorable Balance of Trade |

when country A EXPORTS more than it IMPORTS. The money flows from country B to country A, which increases country A’s GDP and decrease its unemployment rate |

|

|

Unfavorable Balance of Trade |

When country A IMPORTS more than it EXPORTS. The money flows from country A to country B, which decreases country A’s GDP and increase its unemployment rate. |

|

|

Balance of Payments |

covers all the economic transactions of a country; this includes the trade balance, but it also includes other things such as the transfer of capital goods and changes in country’s official reserves |

|

|

Fixed Exchange Rate |

maintain a country's currency value within a very narrow band |

|

|

Floating Exchange Rate |

currency's value is allowed to fluctuate in response to foreign-exchange market mechanisms |

|

|

Currency Appreciation |

when a nations currency is stronger than another nations currency |

|

|

Currency Depreciation |

when a nations currency is weaker than another nations currency |

|

|

Factors that affect Exchange Rates |

Inflation rates Interest Rates Government Debt Recession |

|

|

Purchasing Power |

the financial ability to buy products and services |

|

|

Purchasing Power Parity |

theory which states that exchange rates between currencies are in equilibrium when their purchasing power is the same in each of the two countries |