![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

63 Cards in this Set

- Front

- Back

|

Capital structure |

Debt - Equity ratio of the firm |

|

|

interest rates & taxes |

Once you have debt, you have interest which can be gained back through tax - deduction |

|

|

Moglliani - Miller |

it's a perfect world |

|

|

Debt: advantages & disadvantages |

Advantages: - tax-deduction - Manager's discipline (when debt, obliged to reimbursed->disciplined to pay back) Disadvantages: DIRECT COSTS: from 2 to 5 % of the value of the firm - more risk (default risk) - if default: accumulate obligations (paying more later), reputation & future debt cost, discount rate will increase because of the high risk therefore equity value decreases - Reputation: for partners (clients, suppliers) INDIRECT COSTS: from 10 to 20% of the value of the firm - because of debt a company will abandon a positive NPV (debt overhang) - investing short side - Asset substitution (because of debt, managers are tempted to invest in highly risky projects because of limited liability) |

|

|

Trade-off theory: |

Debt has advantages and disadvantages and they will only chose debt if the advantages compared to the disadvantages - you make a tradeoff |

|

|

Pecking-Order Theory: |

it's always better to use internal funds and firms will always prefer debt over equity ->internal funds->debt-> equity |

|

|

Capital budgeting |

Selecting the best projects in which to invest the firm's resources |

|

|

What are the three steps of capital budgeting? |

1. Identifying potential investments. 2. Analysing those investments to identify which will be sufficiently profitable 3. Implementing and monitoring the investments selected in Step 2 |

|

|

Share buybacks - why have they grown in popularity? |

1. Share price goes up (usually stock is undervalued) 2. The relative tax advantage of capital gains 3. The positive impact on EPS which go up |

|

|

What are the core principles of finance? |

1. The time value of money 2. Risk return trade-off 3. The power of diversification 4. Efficient Markets 5. The no arbitrage principals |

|

|

Shareholder value is? |

Equity value (They want dividends) |

|

|

Debt and tax reduction |

V(firm with debt) = V(Equity) + PV(tax earnings) |

|

|

What are the costs of debt mainly related to? |

They are associated with the possibility of DEFAULT! |

|

|

The approach of the probability of default: method to define the debt ratio |

optimal debt for a company is chosen to ensure that the company's default probability does not exceed a limit set by management |

|

|

The cost of capital approach: method to define the debt ratio |

the optimal debt ratio is chosen to minimize the cost ofcapital. |

|

|

The approach of the adjusted current value method to define the debt ratio |

the effect of adding debt to a company is evaluated by measuring both tax benefits and the costs of bankruptcy |

|

|

The efficient differential approach method to define the debt ratio |

the debt ratio is chose to maximise the difference between ROE and the cost of capital |

|

|

The comparable approach method to define the debt ratio |

The debt ratio is selected by comparing the relative ratios of similar companies |

|

|

What is Finance?

|

Finance is concerned with the allocation of funds under the

|

|

|

How is Corporate Finance different from Finance?

|

The activities involved in managing cash flows of a firm (acorporation)

|

|

|

Two ways in which firms can raise funds:

|

1. Internally: by retaining profits

2. Externally: from investors or creditors: • Equity– Venture capital (VC) or private placements |

|

|

Forms of payouts:

|

1. Regular cash dividends

2. high commitment 3. One–off special dividends • Ex.: Whole Foods Market announced a $2 special dividend in December 2012. This was in addition to its |

|

|

Bubybacks have grown in popularity over the last decade because of:

|

1. Share price goes up (usually stock is undervalued)

2. The relative tac advantage of capital gains 3. The positive impact on EPS which go up |

|

|

Working Capital =

|

Cash + other current assets – current liabilities

|

|

|

How to maximise profits?

|

– Earnings are backward–looking, dependent on accounting principles

|

|

|

How to maximise Shareholder Value (equity value)?

|

– In public firms shareholder wealth is represented by the market price

|

|

|

Name three of the largest Merger Transactions (1998-2012)? |

- Mannesmann AG & Vodafone Air Touch PLC - Shell Transport & Royal Dutch Petroleum - Time Warner & American Online |

|

|

What are the three types of industry based mergers? |

1. Horizontal Merger: Target & Acquirer are in the same industry 2. Vertical Merger: Taregt's industry buys from or sells to acquirer's industry 3. Conglomerate merger: Target and acquirer operate in unrelated industries |

|

|

What is a horizontal merger? |

Horizontal Merger: Target & Acquirer are in the same industry Example: CA and LCL or Renault & Nissan |

|

|

What is a vertical merger? |

Vertical Merger: Taregt's industry buys from or sells to acquirer's industry Example: Tele Atlas and Tom Tom |

|

|

What is a Conglomerate merger? |

Conglomerate merger: Target and acquirer operate in unrelated industries Example: Philipp Morris & General Foods Corp |

|

|

What are the two different types of mergers based on activity classification? |

1. Market Extension Merger: Two companies that deal in the same products but in separate markets. Merging the companies has at it's main aim to access a bigger market and so client base (Renault & Nissan) 2. Product Extension Mergers: Between two businesses that deal in products that are related to each other and operate in the same market. Allows merging companies to group their products and get access to a bigger set of consumers. (Facebook & WhatsApp) |

|

|

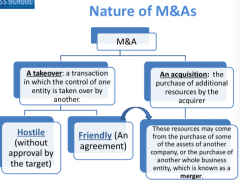

Explain the Nature of M&As.. |

|

|

|

What is the difference between an acquisition and a takeover? |

1. A takeover: A transaction in which the control of one entity is taken over by another (usually hostile or friendly) 2. An acquisition: The purchase of additional resources by the acquirer (usually friendly) |

|

|

What is the difference between a friendly vs. a hostile merger? |

1. Friendly: An agreement 2. Hostile: Without approval by the target |

|

|

What are the three different Corporate Control Transactions? |

1. Statutory Merger: Acquired firm is consolidated into acquiring firm with no further separate identity. 2. Subsidiary Merger: Acquired firm maintains its own former identity 3. Consolidation: Two or more firms combine into a new corporate identity (mainly the case for mergers) |

|

|

What are some possible other types of M&As? |

1. Going-private transactions: transform public corporations into private companies through the issuance of larger amounts of debt used to buy up the outstanding shares of the corporation: - LBO( public shares of a firm are bought and taken private through the use of debt - MBOs ( an LBO initiated by the firm's management) 2. Dual-class recapitalisation: management commonly buys all the shares of a newly issued class of stock carrying "super" voting rights |

|

|

What are the three methods of acquisitions? |

1. Negotiated Mergers: contact initiated by potential acquirer or by target firm 2. Open Market Purchases (Toeholds): Buy enough shares on the open market to obtain controlling interest without engaging in a tender offer 3. Tender offer: - the acquirer announces a public offer to buy a minimum number of the target's shares at a specific price. - Open market purchases, tender offers and proxy fights could be combined to launch a surprise attack on a target firm (hostile takeover) |

|

|

Tell me something about the history of merger waves.. |

Six merger waves in history: - Merger waves are positively related with overall economic activity - concentrated in industries undergoing changes or deregulation - usually ends with large declines in stock market values |

|

|

Tell me about the first merger wave (1897-1904).. |

It was known as the consolidation wave and ended with a stock market crash of 1904 The first two waves are characterised by advent of new technologies such as rail roads and telephones |

|

|

Tell me about the second merger wave (1916-1929).. |

Known as the vertical integration wave & ended in 1929 with a crash: The first two waves are characterised by advent of new technologies such as rail roads and telephones |

|

|

Tell me about the third merger wave (1965-1969).. |

Push for conglomeration Conglomerates discount effect |

|

|

Tell me about the fourth merger wave (1981-1989).. |

Spurred by the lax regulatory environment of the time and advent of high - yield financing: - Shift back to corporate specialisation - junk bond financing played a major role during this wave: - Antitakeover measures adopted to prevent hostile takeovers - Ended with the slowdown of the economy in the late 80s and early 90s |

|

|

Tell me about the fifth merger wave (1993-2001).. |

Characterised by friendly stock financed mergers relatively lax regulatory environment: still open to horizontal mergers consolidation in non-manufacturing service sector: healthcare, banking, telecom & high-tech - merger activity surpassed all the other reaching 3.4 $ trillion |

|

|

Tell me about the sixth merger wave (2004-2008).. |

New records: ended abruptly with the financial markets meltdown that stopped financing and eroded equity values |

|

|

What is the acquisition premium ? |

A bidder is unlikely to acquire a target company for less than it's current market value. In practice, most acquirers pay a premium to the current market value. -> this premium is defined as the percentage difference between the acquisition price and the pre-merger of a target firm |

|

|

What are the three market reactions to a takeover? |

1. Acquirers pay an average premium of 43% over the pre - merger price of the target. 2. When a bid is announced, target shareholders enjoy a gain of 15% on average in their stock price. 3. Acquirer shareholders see an average gain of 1% but more than half receive a price decrease. |

|

|

How can buying a firm at a premium to the current market price be a positive NPV investment if markets value firms fairly? |

Mergers generate value through the exploitation of synergies |

|

|

What are the three operational synergies through M&A? |

1. Economies of scale: Merger may reduce or eliminate the need for overlapping resources. -> horizontal mergers only 2. Economies of scope: are other value-creating benefits of increased size. (ex. launching large campaign, having access to some markets) > horizontal mergers only 3. Resource complementarities: Merging firms have operational expertise in different areas (ex. one company has expertise in R&D, the other in marketing; successful in both horizontal and vertical mergers) |

|

|

What are operational synergies related to exercise in particular areas (in M&A)? |

- Particularly with new technologies, hiring experienced workers directly may be difficult. - It may be more efficient to purchase the talent as an already functioning unit by acquiring an existing firm |

|

|

What are managerial synergies ( from M&A)? |

- Management teams with different strengths are combined: - expertise in revenue growth and identifying customer trends paired with expertise in cost control and logistics |

|

|

What are financial synergies ( from M&A)? |

When a merger results in less volatile cash flow, lower default risk and lower cost of capital. |

|

|

What is meant by market power as a benefit of a horizontal merger? |

- Regulatory authorities would deny a merger if it would result in a firm so dominant that it would have the power to control prices in its market - Market power can be the result of a horizontal merger through the increase in presence and representation within the market |

|

|

What are other strategic reasons for mergers? |

- Product quality increase in vertical mergers - Defensive consolidation in a mature or declining industry: consolidation in the defence industry |

|

|

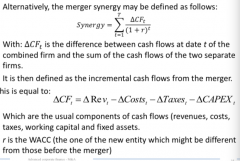

How can you quantify a synergy? |

Synergy: the value of the combined firm is bigger than the standalone sum of each of the two companies - Vab> (Va+Vb) 1+1+=3 - > the success of an M&A deal depends exactly on whether this synergy can be achieved |

|

|

Quantifying the synergy alternative definition of a merger: |

|

|

|

What are the four different possible categories in which all synergies fall? |

1. Revenue enhancement 2. Cost reduction 3. tax efficiency 4. Lowering the cost of capital |

|

|

What is another definition for synergies? |

Synergies are the incremental cash flows associated with the takeover. |

|

|

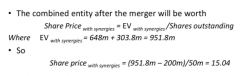

How do you calculate the offer price? |

|

|

|

What are stock market driven acquisitions (other reason for a merger)? |

- Markets are not entirely efficient and may misplace firms - Rational managers take advantage of market misplacing (time the market) and use their overrated stock to buy relatively less overvalued firms - High valuation bidders are more likely to use stock as a mean of payment |

|

|

What is meant by the Urge to Merge (other reason for M&A)? |

The influence of investment bankers: - financial advisers pitch deals to potential clients -investment bankers earn large fees from advising on deals-> potential conflict of interest - Reputation can be an important deterrent and is associated with higher bidder gains in public firm acquisitions |

|

|

What is meant by tax savings from operating losses in M&A discussions? |

A conglomerate may have a tax advantage over a single-product firm because losses in one division can offset profits in another division - to justify a takeover based on operating losses, management would have to argue that the tax savings are over and above what the firm would save using carry back and carry forward provisions |

|

|

What is meant by diversification as a motive for a merger? |

1. Risk reduction: large firms bear less unsystematic risk, so justification would be that combined firms are less risky -> BUT investors can achieve the benefits of diversification themselves by purchasing shares in two separate firms 2. Debt Capacity and Borrowing Costs: Large firms are more diversified and have lower probability of bankruptcy - > gains must be large enough to offset any disadvantages of running a larger less focused fir; a firm may be able to increase its debt and enjoy greater tax savings 3. Liquidity: shareholders of private companies often have a disproportionate share of their wealth invested in the private company |