![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

31 Cards in this Set

- Front

- Back

|

Types of accounts for these chapters |

Allowance for doubtful accounts (contra asset) Uncollectible accounts expense (not on balance sheet) |

|

|

Formulas |

A/R Accounts Receivable) Beg Balance + Sales on Acct - Cash collected from Customers - Write-offs ------------------------------------------------ End balance A/R ADA (Allowance for doubtful accounts) Beg Balance + UAE (Uncollectible accounts expense) - Write offs _______________ End balance ADA NRV Net realized value A/R (ADA) --------- NRV Basket Purchase Asset |Appraisal Value / Total Value = Rate * Acquisition cost = Adjusted cost Straight-Line (Cost – Salvage Value) ÷ Useful Life = Annual Depreciation Double-Declining Balance (Cost – Accum. Depreciation at Beginning of Period) × (2 × SL Rate) = Annual Depreciation Units of production ((Cost - SV) / Estimated Units of Production)x Units of production in currents yr = Annual depreciation expense |

|

|

Face value |

Full amount |

|

|

The amount of receivables a company estimates it will actually collect |

Net realized value (NRV) Face value- allowance for doubtful accounts |

|

|

a company's estimate of the amount of uncollectible receivables |

allowance for doubtful accounts |

|

|

3 methods used to determine NRV of |

to avoid overstating assets, companies usually report receivable on their balance sheet as the NRV

known as: Allowance method of accounting for uncollectible accounts Also: Percent of revenue method Also: Percentage of receivables method |

|

|

Have a physical presence: they can be seen and touched |

Tangible Assets |

|

|

Have no physical for: Rights, privileges, patents etc. |

Intangible assets |

|

|

The term used to recognize expense for property, plants and equipment |

Depreciation |

|

|

Mineral Deposits, oil and gas reserves, timber stands, coal mines and stone quarries are examples of |

Natural resources |

|

|

The term used to recognize expense for natural resources |

Depletion |

|

|

The term used when recognizing expense for intangible assets with identifiable useful lives is called |

amortization |

|

|

What is the Historical Cost Concept |

Requires that assets be recorded at the amount paid for it. |

|

|

Relative Fair Market Value Method |

Used with Basket purchases. Asset |Appraisal Value / Total Value = Rate * Acquisition cost = Actual cost |

|

|

The amount of an asset's cost that is allocated to expense during an accounting period |

Depreciation Expense |

|

|

The expected Market Value of a fully depreciated asset is called |

Salvage value

|

|

|

The total amount of depreciation a company recognizes for an asset |

Depreciable cost |

|

|

3 type of methods used for Depreciating Expense's with assets |

Straight-line (Cost - SV) / Estimated Useful Life Double-declining Yr | Beg BV | Rate (SL rate *2) | Dep Exp | End BV | End A/D Units of production ((Cost - SV) / Estimated Units of Production) x Units of production in currents yr = Annual depreciation expense |

|

|

Because they reduce net income when incurred, accountants often call repair and maintenance cost...(companies subtract them form REV by way of recording and EXP) |

revenue expenditures |

|

|

Substantial amounts spent to improve the quality or extend the life of an asset are described as |

capital expenditures Improves Quality: Increase Machinery Extends Life: increase BV and Acc. Dep. |

|

|

The value attributable to favorable factors such as reputation, location, and superior products |

Goodwill |

|

|

Assets like inventory, office supplies are called |

Current assets |

|

|

Assets like equipment or buildings that are used for an extended period of time |

long-term operational assets

|

|

|

What is "remitting the tax" mean |

Paying cash to the tax authority |

|

|

Liabilities that mature within on year of a company's operating cycle, whichever is longer |

current liabilities |

|

|

a potential obligation arising from a past event |

contingent liabilities Ex: Pending Lawsuit |

|

|

The classifications of Contingent Liabilities |

Probable and estimable - Recognize in financial Statements Reasonably possible (or probably but not estimable) - Disclose in the footnotes of the financial statements Remote - Need not recognize or disclose |

|

|

All other liabilities in respect to being over a year and have varying requirements for paying interest charges and repaying principle |

Long-term liabilities |

|

|

Repaying a portion of the principle with regular payments that also include interest is often called |

loan amortization |

|

|

Loans that require payments of principal and interest at regular intervals (amortizing loans) are typically represented by |

installment notes |

|

|

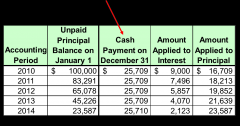

Amortization Schedule for Installment notes |

|